Mark Zuckerberg just created a photorealistic AI version of himself that can interact with Meta’s 79,000 employees in real time. The project, announced April 13 and still in early development, represents something far more significant than a Silicon Valley vanity exercise. It signals that Meta Platforms (NASDAQ: META) is now deploying its own AI infrastructure internally at the executive level, turning a $115-135 billion capital expenditure commitment for 2026 into a live product that the entire company can test, critique, and refine before it ever reaches an external customer.

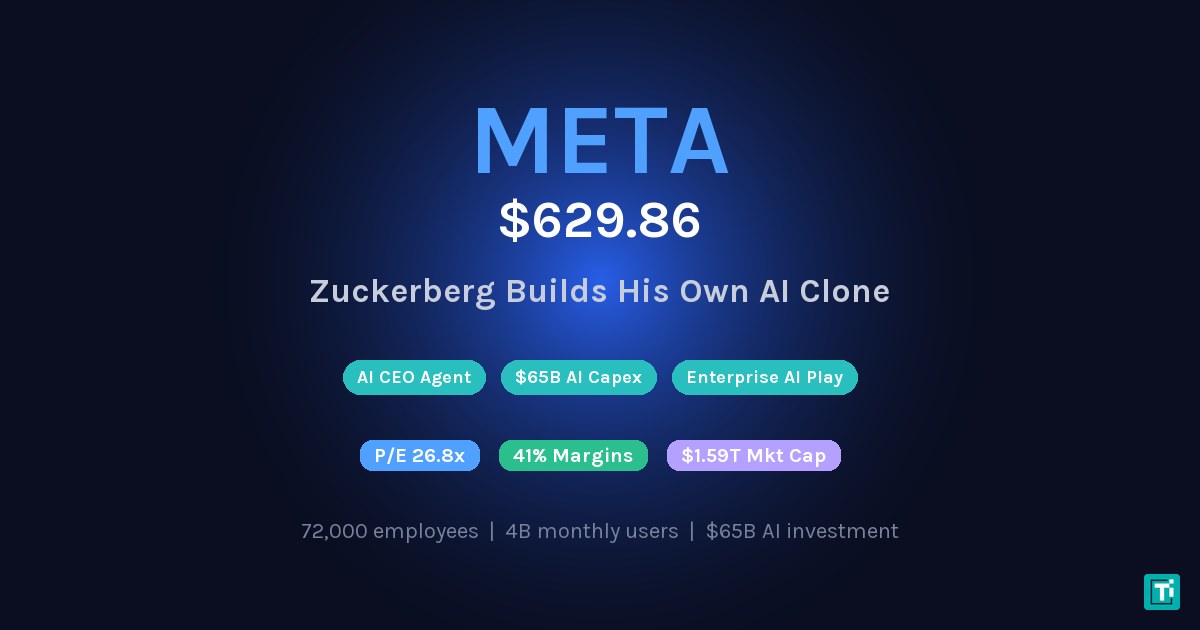

META stock closed at $629.86 on Friday, April 11, with a market capitalization of $1.59 trillion. The stock trades at 26.8 times trailing earnings. The AI Zuckerberg initiative adds strategic optionality to a company already generating 41% operating margins from its advertising business.

Key Takeaways

- Meta unveiled an AI clone of Zuckerberg that uses photorealistic avatar technology and Llama models to interact with 72,000 employees in real time, separate from a "CEO agent" productivity tool also in development.

- META stock closed at $629.86 with a $1.59 trillion market cap, 26.8x P/E ratio, 41.44% operating margins, and 30.08% net margins, placing it among the most profitable large-cap tech companies globally.

- Meta committed $60-65 billion to AI capex in 2025, and the AI Zuckerberg project transforms that abstract spending into a tangible internal product that could eventually serve as an enterprise AI sales demonstration.

- Insider selling totaled $103.2 million across 20 transactions in three months with zero insider buying, though the amount represents less than 0.05% of total insider-held share value.

- Enterprise AI agent market projected at $82B by 2028 according to Gartner, and Meta's combination of Llama models, 1 billion Meta AI users, and internal deployment gives it a distribution edge over pure-play enterprise AI startups.

Last updated: April 13, 2026 at 4:15 PM ET

What Exactly Is the AI Zuckerberg?

Meta has been developing an artificial intelligence version of its CEO capable of engaging with employees through photorealistic, real-time conversation. The project is separate from another internal initiative building a “CEO agent” designed to assist Zuckerberg with leadership and decision-making tasks.

The distinction matters. The CEO agent functions as an executive productivity tool, handling scheduling, data synthesis, and briefing preparation. The AI Zuckerberg functions as a communication layer, allowing the CEO to effectively scale his presence across a workforce of 72,000 without scheduling a single all-hands meeting or recording a single video.

Technical details remain limited given the early stage, but the underlying technology almost certainly leverages Meta’s Llama large language model family and its proprietary research in photorealistic avatars. Meta spent years and billions developing avatar technology for its metaverse division, accumulating over $80 billion in cumulative Reality Labs operating losses since 2020. Critics called that spending wasteful. The AI Zuckerberg project suggests at least some of that investment is now finding commercial application. The photorealistic rendering pipeline, the real-time facial animation models, and the natural language interaction systems developed for the metaverse are exactly the technologies powering the digital Zuckerberg.

META Stock at $629.86: Reading Between the Lines

The raw financial picture at Meta remains formidable. Operating margins sit at 41.44%. Net margins clock in at 30.08%. Nearly 4 billion people use at least one Meta platform every month across Facebook, Instagram, WhatsApp, and Messenger. These numbers place Meta among the most profitable large-cap technology companies on the planet.

At 26.8 times trailing earnings, META is not cheap by traditional value metrics. But the P/E ratio needs context. Revenue has been growing at a double-digit pace, with Q4 2025 posting 24% year-over-year revenue growth to $59.9 billion, driven primarily by AI-optimized ad targeting through Meta’s Advantage+ system. Advertisers using the platform report 30-40% improvements in return on ad spend according to Meta’s own case studies, creating a flywheel where better AI targeting generates more advertising revenue, which funds further AI development.

The AI Zuckerberg announcement adds a layer of strategic value that traditional metrics cannot capture. When a $1.59 trillion company begins deploying its own AI products at the leadership level, it sends an unmistakable signal: the technology works well enough for the highest-stakes internal use cases.

The $65 Billion Question: Is Meta Eating Its Own Dogfood?

Meta’s 2025 AI capital expenditure guidance of $60-65 billion terrified Wall Street when first announced, sending the stock down 15% in a single session. That spending funded new data centers, custom AI training chips, and the compute infrastructure powering Meta’s family of Llama models.

The AI Zuckerberg project transforms that abstract capex figure into something tangible. Every major technology company talks about AI transformation. Meta is now testing it on its own CEO. That is a fundamentally different credibility proposition than publishing research papers or releasing benchmark scores.

Consider the enterprise implications. If Meta can demonstrate that an AI avatar of its CEO improves communication, reduces meeting load, and maintains employee engagement across a 79,000-person organization, every Fortune 500 company running Microsoft Teams or Slack becomes a potential customer for similar technology. Industry analysts project a rapidly expanding multi-billion-dollar market for enterprise AI agents over the next several years.

Meta already has a distribution advantage most enterprise AI startups can only dream about. Meta AI crossed 1 billion monthly active users in early 2026. The infrastructure, the models, and the user base already exist. The AI Zuckerberg project is a proof of concept that no sales pitch could replicate.

Insider Selling: $103 Million in Three Months

Meta insiders sold $103.2 million in shares over the past three months across 20 separate transactions. Zero insider buying occurred during the same period. According to SEC filings, the selling was distributed among multiple executives rather than concentrated in a single individual.

The headline number sounds alarming. Context softens it. Mark Zuckerberg controls roughly 13% of Meta’s outstanding shares, worth approximately $207 billion at current prices. Periodic sales for tax planning, portfolio diversification, and philanthropic commitments through the Chan Zuckerberg Initiative are standard practice for executives with concentrated holdings. The $103.2 million represents less than 0.05% of insider-held value.

Still, the complete absence of insider buying during a period when Meta announced its most ambitious internal AI initiative deserves a footnote. If the leadership team views the AI Zuckerberg project as genuinely transformative, investors might reasonably expect at least symbolic open-market purchases. The lack of buying does not invalidate the bull case, but it does add nuance.

Where the Zuckerberg AI Fits in Silicon Valley’s Broader Race

Meta is not operating in isolation. Microsoft has embedded Copilot deeply into its internal operations, using AI for meeting summaries, communications drafting, and project management. Google DeepMind deploys custom AI agents for internal research coordination. Salesforce’s Einstein AI handles customer-facing interactions across thousands of enterprises.

Microsoft’s approach prioritizes breadth, embedding AI assistance into every layer of Office 365 and Teams. Google’s approach emphasizes research-grade intelligence applied to narrow problems. Meta’s approach bets on photorealism and personality, arguing that employees engage more deeply with an AI that looks and sounds like a real person than with a text-based chatbot. Meta’s own internal research on avatar interaction, developed through years of Reality Labs work, suggests that employees engage more deeply with photorealistic AI than text-based chatbots, though independent verification of these claims remains limited.

What distinguishes Meta’s approach is the photorealistic, CEO-specific implementation. Rather than building a generic corporate chatbot, Meta is creating a digital twin of its most recognizable executive. The branding implications extend well beyond internal culture. Every employee interaction with the AI Zuckerberg generates training data, edge case feedback, and product refinement that Meta can use when packaging similar technology for enterprise sale.

The risk is equally notable. If the AI Zuckerberg produces errors, makes tone-deaf statements, or feels inauthentic, the internal backlash could undermine confidence in Meta’s AI capabilities at exactly the moment the company needs full workforce buy-in on its AI infrastructure pivot.

What META Investors Should Watch Next

The AI Zuckerberg project adds optionality rather than immediate revenue impact. If it succeeds, Meta gains a compelling enterprise AI demonstration capable of opening new revenue streams beyond advertising. If it fails quietly, the financial impact is negligible given Meta’s scale.

The metric to track is not the AI Zuckerberg project itself. Watch Meta’s enterprise AI revenue disclosures in future earnings calls. Meta has historically been a consumer-facing company with 98%+ of revenue from advertising. Any meaningful B2B AI revenue reported by late 2026 would represent a strategic inflection point that the current $629.86 stock price does not fully reflect.

At 26.8 times earnings with 41% margins and double-digit revenue growth, META remains priced for continued execution on its advertising business. The AI Zuckerberg is a bet on what comes after advertising. Whether that bet pays off depends on execution, not ambition, and Meta has up to $135 billion in planned 2026 infrastructure spend suggesting it is deadly serious about getting this right.

The broader market context also favors Meta’s timing. The Nasdaq has recovered roughly half of its March selloff, and technology stocks with demonstrated AI revenue (not just AI promises) are commanding premium multiples. Meta’s Advantage+ advertising system already generates measurable AI-driven revenue. The Zuckerberg clone could eventually prove that the same AI stack works for enterprise communication. If both bets pay off simultaneously, the advertising-plus-enterprise combination would justify a significantly higher earnings multiple than META currently trades at.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. TECHi and its authors may hold positions in securities mentioned. Always conduct your own research and consult a licensed financial advisor before making investment decisions.