- QQQ closed at $611.07gaining 4.1% for the week ending April 10, its strongest weekly performance since November 2025.

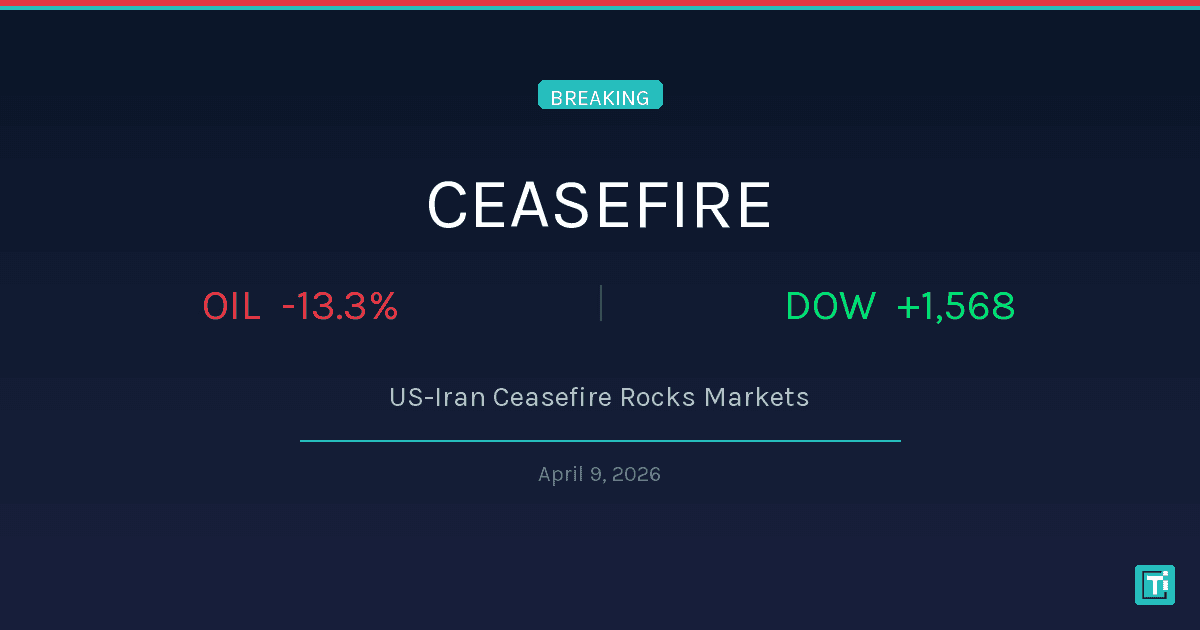

- Iran ceasefire triggered the rallywith oil crashing 16.4% to $94.41 per barrel on April 8 before bouncing back to $104.53 by Friday.

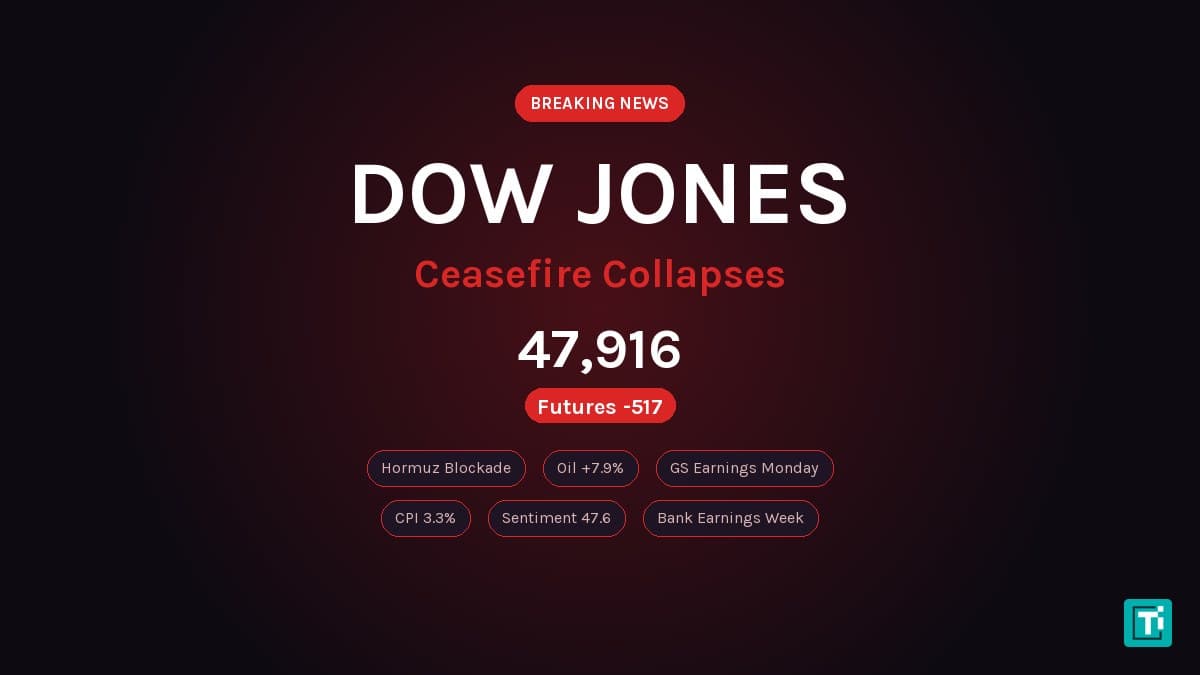

- March CPI hit 3.3% year-over-yeardriven by a 21.2% monthly gasoline surge, but core CPI came in below expectations at 2.6%.

- Hyperscaler AI capex reaches $660 billionin 2026 with roughly $450 billion earmarked for AI infrastructure across Amazon, Alphabet, Microsoft, and Meta.

- Consumer sentiment collapsed to 47.6a record low, even as S&P 500 companies are expected to deliver 13% earnings growth this quarter.

QQQ closed at $611.07 on Friday, April 10, capping a 4.1% weekly gain that marks the Invesco QQQ Trust's strongest performance since November 2025. The Nasdaq Composite finished at 22,902.89, up roughly 907 points from where it started the week. For context, the S&P 500 gained 3.6% over the same five sessions, and the Dow added 3%.

Three forces drove the move: a last-minute ceasefire between the United States and Iran that sent oil crashing, a March CPI report that spooked Friday's session, and a hyperscaler capital spending cycle that continues to provide a structural floor beneath the Nasdaq-100's biggest constituents.

The Ceasefire That Saved the Week

By Monday morning, April 7, traders were positioned for the worst. President Trump had set an 8 PM ET deadline to strike Iranian power plants if Tehran did not agree to terms. Oil hovered near $112 per barrel. The Strait of Hormuz, through which roughly 20% of global crude flows, had been the epicenter of a conflict that had already pushed energy prices up 70% from pre-crisis levels.

Then the calculus changed. Barely an hour before Trump's deadline on Tuesday evening, the U.S., Iran, and Israel agreed to a two-week ceasefire. Markets responded immediately. On Wednesday morning, the Dow surged 1,325 points for its best single session in over a year. The Nasdaq Composite jumped 2.8%, or 617 points. WTI crude collapsed 16.4% to $94.41 per barrel, the steepest single-day decline since April 2020.

QQQ rode the wave, gaining 2.97% on Wednesday alone for its sixth consecutive up day. But the relief was short-lived in the oil pits. By Friday, crude had bounced back above $104 per barrel as traders questioned whether the ceasefire would hold through weekend negotiations in Islamabad between Vice President JD Vance and Iranian officials.

CPI Reality Check: 3.3% Headline, But Look Deeper

Friday's session told a different story. The Bureau of Labor Statistics reported that March headline CPI rose 0.9% month-over-month, pushing the annual rate to 3.3%, the highest reading since May 2024. Gasoline prices drove the majority of the increase, surging 21.2% in a single month, the largest monthly spike since the BLS began tracking the component.

Energy costs overall climbed 10.9%, accounting for roughly three-quarters of the total monthly CPI increase. For anyone filling a tank in March while Strait of Hormuz supply fears were peaking, this was not a surprise. It was confirmation.

The number that mattered more to equity traders was core CPI, which strips out food and energy. Core came in at +0.2% monthly and 2.6% annually, both a tenth of a percentage point below consensus. That gap, small as it sounds, was enough to prevent a full-blown selloff. The Nasdaq still eked out a 0.35% gain on Friday, even as the Dow dropped 269 points and the VIX settled at 19.23.

Fed Chair Powell's response reinforced the market's interpretation. He signaled the Fed would look through what it considers a supply-driven shock, focusing instead on whether long-term inflation expectations (five- to ten-year horizon) have shifted. So far, they have not.

The $660 Billion AI Floor

Strip away the geopolitics and the inflation noise, and QQQ's structural story comes down to one number: $660 billion. That is the approximate combined capital expenditure budget for the four largest hyperscalers in 2026, nearly double what they spent in 2025.

Amazon leads at $200 billion. Alphabet follows at $175 to $185 billion. Microsoft is projecting $120 to $140 billion, a 59% increase from fiscal 2025. Meta rounds out the group at $115 to $135 billion. Roughly 75% of that aggregate spend, approximately $450 billion, is earmarked specifically for AI infrastructure.

This matters for QQQ because these four companies, along with NVIDIA, Apple, and Tesla, collectively represent over 40% of the Nasdaq-100's weighting. When Amazon commits $200 billion to data center buildouts, that spend flows directly into NVIDIA's GPU revenue (NVDA closed at $188.63), Broadcom's custom ASIC orders, and the semiconductor supply chain that TSMC anchors with its $35.7 billion Q1 2026 revenue, up 35% year over year.

Goldman Sachs projects that seven major tech companies will drive 46% of S&P 500 earnings growth in 2026. The firm maintains a year-end S&P 500 target of 7,600, premised on 12% aggregate earnings growth, and argues the market has reached an inflection point where AI deployment costs have fallen enough for the broader corporate sector to adopt profitably.

Tariff Overhang: The July 24 Expiration

There is a policy risk that markets have not fully priced. After the Supreme Court struck down IEEPA tariffs in February, the administration pivoted to Section 122 of the Trade Act of 1974, imposing a 15% universal surcharge on most imports. That surcharge is explicitly temporary: it expires on July 24, 2026.

The administration must either negotiate new trade agreements before that date or seek congressional approval to make the surcharges permanent. Neither path is straightforward. A separate 25% semiconductor tariff, implemented in January under Section 232, remains in place with exemptions for U.S. data centers, R&D, and consumer applications.

Apple absorbed between $800 million and $1.1 billion in tariff costs per quarter throughout 2025 despite a $500 billion reshoring commitment. AAPL closed at $260.48 on Friday. Microsoft (MSFT: $370.87), Meta (META: $629.86), and Alphabet (GOOG: $315.72) face less direct hardware exposure but are not immune to the inflationary ripple effects on enterprise budgets.

Consumer Sentiment Collapse Versus Earnings Resilience

The University of Michigan Consumer Sentiment Index cratered to 47.6 in April, a record low. That reading sits well below the 50-level that historically precedes consumer spending contractions. Gas prices averaging roughly $4.12 per gallon nationally, according to AAA data, combined with 3.3% headline inflation, are squeezing household budgets in ways that show up first in sentiment surveys and later in retail spending data.

And yet corporate earnings tell a different story. S&P 500 companies are expected to deliver 13% year-over-year earnings growth when the reporting season hits full stride this month. JPMorgan Chase and Bank of America report on April 14 and 15, providing what analysts are calling the definitive test of whether the banking sector's loan books and trading desks reflect the economic stress that consumer surveys suggest.

The disconnect between collapsing sentiment and resilient earnings is not new. Corporate profit margins have been insulated by pricing power, AI-driven productivity gains, and a labor market that added 178,000 jobs in March with unemployment holding at 4.3%. The question is how long that insulation holds if energy costs remain elevated and the ceasefire unravels.

What to Watch This Week

Three catalysts will determine whether QQQ's momentum extends or reverses.

First, the Islamabad negotiations. If the ceasefire collapses, oil retests $112 and the entire weekly gain is at risk. If it firms into a longer-term agreement, energy-driven inflation pressures ease and the Fed's "look through" stance gets validated.

Second, bank earnings. JPMorgan's commentary on commercial lending, credit quality, and trading revenue will set the tone for the entire earnings season. Any sign that corporate borrowers are pulling back would undercut the 13% earnings growth consensus.

Third, the Fed's April 29 meeting. No rate action is expected, but the statement's language on inflation will signal whether the March CPI print has shifted the committee's thinking. The current rate stands at 3.50% to 3.75%, with the median projection calling for one cut in 2026.

QQQ's 4.1% weekly gain was earned in a market that swung between war fears, ceasefire euphoria, and inflation anxiety. The underlying fundamentals, $660 billion in AI capital spending, 13% expected earnings growth, and a Fed willing to look through supply shocks, remain intact. Whether those fundamentals can overpower a 47.6 consumer sentiment reading and a ceasefire that has not yet survived its first weekend is the bet every QQQ holder is making heading into Monday.

FAQ

Frequently asked questions

Why did QQQ surge this week?

QQQ gained 4.1% for the week ending April 10, 2026, primarily driven by the U.S.-Iran ceasefire announced on April 8 that sent oil prices crashing 16.4% and triggered a broad risk-on rally across global markets. The Nasdaq Composite posted its best weekly performance since November 2025.

What is QQQ trading at right now?

QQQ closed at $611.07 on Friday, April 10, 2026, with a daily range of $609.58 to $613.67. The Nasdaq Composite finished at 22,902.89.

How does the March CPI report affect QQQ?

March headline CPI came in at 3.3% year-over-year with gasoline prices surging 21.2% month-over-month. However, core CPI (excluding food and energy) was slightly below expectations at 2.6% annually. Fed Chair Powell indicated the Fed would look through the supply-driven energy shock, which limited the downside impact on tech stocks.

What is driving tech stocks higher in 2026?

The primary driver is the hyperscaler AI capital spending cycle. Amazon, Alphabet, Microsoft, and Meta are collectively spending approximately $660 billion in 2026, with roughly $450 billion earmarked for AI infrastructure. This spending flows directly into Nasdaq-100 components like NVIDIA, Broadcom, and the broader semiconductor supply chain.

Is QQQ a good buy after the April rally?

QQQ faces a mixed outlook. Supporting factors include $660 billion in AI capex, 13% expected S&P 500 earnings growth, and a Fed willing to look through supply-driven inflation. Risks include a fragile Iran ceasefire, record-low consumer sentiment at 47.6, tariff uncertainty with the Section 122 surcharge expiring July 24, and headline CPI at 3.3%. Investors should assess their risk tolerance and consult a financial advisor.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Fatimah Misbah Hussain is a seasoned financial journalist at TECHi, specializing in stock market analysis, commodities, and tech sector finance. With a strong background in monitoring public markets and tech companies, she breaks down complex stock movements and commodity price trends into actionable insights.