Apple has absorbed $3.3 billion in tariff costs since April 2025 and the meter is still running. With quarterly expenses accelerating from $800 million to $1.4 billion, a Supreme Court ruling that rewrote the tariff playbook, and a massive supply chain migration underway from China to India, the cumulative financial burden on the world’s most valuable company could approach $20 billion by the end of the decade. For AAPL shareholders watching the stock trade near $250, the question is no longer whether tariffs matter. It is whether Apple’s famous margin resilience can outlast Washington’s trade policy experiments.

Key Takeaways

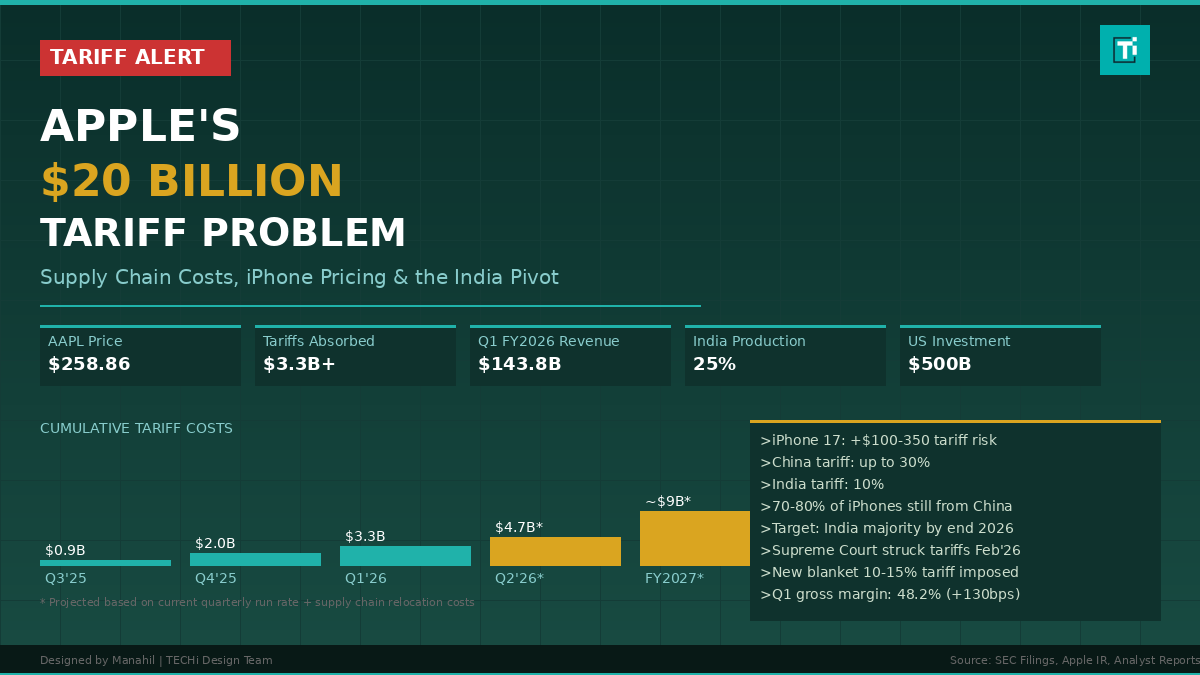

- Tariff Costs Accelerating Apple absorbed $3.3 billion in tariff costs from April to December 2025, with the quarterly rate nearly doubling from $800 million to $1.4 billion. The annual run rate now exceeds $5 billion.

- Supreme Court Mixed Verdict The February 2026 ruling struck down IEEPA-based tariffs but Trump immediately imposed a 10% blanket tariff under Section 122 with no product exemptions for Apple.

- India Manufacturing Push India now produces 25% of all iPhones globally, up from under 5% four years ago. Apple targets majority U.S.-bound production from India by end of 2026.

- iPhone 17 Pricing Risk Tariff pass-through could add $100 to $350 per device on iPhone 17 models, with the base model projected between $899 and $999.

- $20B Cumulative Exposure Under current tariff rates and supply chain restructuring costs, Apple cumulative tariff-related expenses could approach $20 billion by end of the decade.

Table of Contents

The $3.3 Billion Bill So Far

When President Trump reimposed tariffs on Chinese imports in April 2025, Apple immediately became the highest-profile corporate casualty. CEO Tim Cook disclosed on the Q2 FY2025 earnings call that tariffs would cost the company approximately $900 million for the June 2025 quarter alone. The actual figure came in slightly lower at roughly $800 million, but the trajectory was unmistakable. By the September quarter, costs climbed to $1.1 billion. The holiday quarter pushed the total to $1.4 billion as Apple shipped record volumes of iPhones through a tariff gauntlet that showed no signs of easing.

Through the end of calendar year 2025, Apple’s cumulative tariff bill reached approximately $3.3 billion, according to disclosures made across three consecutive earnings calls. Cook emphasized on each call that Apple chose to absorb these costs rather than pass them to consumers through price increases. That decision protected demand but carved directly into margins. TECHi’s comprehensive Apple stock analysis tracks the full valuation picture as these costs evolve.

The scale of the expense is best understood in context. Apple’s entire R&D budget for fiscal 2025 was approximately $30 billion. The tariff bill through just three quarters consumed more than 10% of that figure. While Apple’s $42.1 billion quarterly profit makes these numbers manageable in the short term, sustained tariff exposure at this rate creates a structural drag that investors cannot ignore.

Quarterly Tariff Cost Breakdown

Apple has disclosed tariff-related costs on earnings calls with unusual specificity for a company that typically avoids granular cost breakdowns. The following table compiles every disclosed or projected figure from SEC filings and earnings call transcripts since tariffs took effect.

| Quarter | Period | Tariff Cost | Source |

|---|---|---|---|

| Q2 FY2025 | Apr–Jun 2025 | ~$800M (actual) | Q3 FY2025 Earnings Call |

| Q3 FY2025 | Jul–Sep 2025 | ~$1.1B (projected) | Q3 FY2025 Earnings Call |

| Q4 FY2025 | Oct–Dec 2025 | ~$1.4B (estimated) | Q1 FY2026 Earnings Call |

| Cumulative Total | Apr–Dec 2025 | ~$3.3B | CNBC / Apple IR |

The acceleration pattern is clear. Each quarter brought higher tariff costs as Apple’s import volumes increased through the holiday season and tariff rates on certain product categories escalated. If Q1 FY2026 (January through March 2026) runs at a similar or higher rate, the annual run rate exceeds $5 billion per year in direct tariff expenditures alone.

The Supreme Court Ruling That Changed Everything

On February 20, 2026, the Supreme Court handed down a 6-3 ruling in Learning Resources, Inc. v. Trump that struck down the president’s reciprocal tariff program as unconstitutional. Chief Justice John Roberts wrote in the majority opinion that the International Emergency Economic Powers Act (IEEPA) did not grant the executive branch unilateral authority to impose tariffs. The ruling potentially entitled the U.S. government to refund more than $175 billion in collected tariff revenue to importers.

For Apple, the immediate reaction was relief. The reciprocal tariffs had been the primary driver of its $3.3 billion cost burden. Cook had spent months lobbying for product-specific exemptions, successfully securing exclusions for most Apple products from the highest tariff tiers. The Supreme Court decision appeared to invalidate the entire framework those exemptions operated within.

The relief lasted roughly three hours. Within the same day, Trump signed an executive order imposing a new 10% blanket tariff on all imports, invoked under Section 122 of the Trade Act of 1974 rather than IEEPA. Unlike the struck-down tariffs, this new authority had not been tested in court. Apple’s products, which had enjoyed various exemptions under the old system, were now included under the blanket rate with no carve-outs.

The ruling did accomplish one critical thing for Apple’s long-term planning: it removed the threat of arbitrary tariff escalation. Trump had previously threatened a 25% tariff on all iPhones not manufactured in the United States. With the Supreme Court limiting executive tariff authority, that specific scenario became significantly less likely. For a company making capital allocation decisions years in advance, legal guardrails matter more than the current rate.

Apple’s India Manufacturing Gambit

Apple’s most aggressive response to tariff risk has been the rapid expansion of iPhone manufacturing in India. As of early 2026, India accounts for 25% of global iPhone production, up from less than 5% just four years ago. In calendar year 2025, Indian factories assembled approximately 55 million iPhones, a 53% increase year over year. The production is led by Foxconn and Tata Electronics, which have collectively invested over $2.4 billion in Indian manufacturing capacity.

Cook signaled on the Q1 FY2026 earnings call that Apple expects the majority of iPhones sold in the United States to have India as their country of origin by the end of calendar year 2026. The target for India’s share of global iPhone production is 32% by fiscal year 2026-2027, with long-term ambitions pushing toward 50% within the next three to four years.

The shift carries real costs. Production expenses in India run approximately 5% to 8% higher than equivalent operations in China, according to supply chain analysts. The logistics infrastructure is less mature, worker training cycles are longer, and the supplier ecosystem that Apple spent decades cultivating in Shenzhen and Zhengzhou does not yet exist at comparable scale in Chennai or Bengaluru. Apple reportedly airlifted 600 tons of iPhones from India to the U.S. in late 2025 on chartered flights to beat tariff deadlines, an expensive workaround that underscores the logistical friction of the transition.

India’s Production Linked Incentive (PLI) scheme has been a critical enabler. The program offers manufacturers financial incentives for meeting production targets in India, partially offsetting the higher operational costs. Foxconn is building a new facility near Bengaluru, and Tata Electronics is expanding capacity at multiple sites. The combined investment pipeline for Apple-related manufacturing in India is estimated to exceed $5 billion through 2028.

The $500 Billion Investment Pledge: Real or Theater?

In February 2025, Apple announced its largest-ever U.S. spending commitment: more than $500 billion over four years. The pledge came with headline-grabbing specifics including 20,000 new jobs, a 250,000-square-foot server manufacturing facility in Texas slated to open in 2026, an expansion of the U.S. Advanced Manufacturing Fund from $5 billion to $10 billion, and a commitment to be the largest customer at TSMC’s Fab 21 facility in Arizona.

The timing was not subtle. The announcement landed weeks before Trump was expected to finalize new tariff schedules, and the White House praised it publicly. But analysts immediately questioned the substance behind the number. AppleInsider characterized the pledge as ‘business as usual,’ noting that much of the $500 billion represented spending Apple would have made regardless of tariffs, including payroll for existing U.S. employees, ongoing data center investments, Apple TV+ production budgets across 20 states, and payments to thousands of existing U.S.-based suppliers.

The genuinely incremental spending appears to be considerably smaller than the headline figure. The server factory in Texas, the TSMC investment, the manufacturing fund expansion, and new hiring represent meaningful but more modest commitments. Analysts at Wedbush Securities estimated that the truly new spending was closer to $400 million annually in net-new manufacturing investment, not $500 billion in total economic activity. The distinction matters because it reveals Apple’s tariff strategy: make the political gesture large enough to buy goodwill while keeping actual incremental costs contained.

iPhone 17 Pricing: What Consumers Should Expect

The iPhone 17 lineup, expected to launch in September 2026, will be the first major product cycle where tariff-driven supply chain restructuring directly influences retail pricing. Analysts project that tariff-related costs could add between $100 and $350 to every iPhone 17 model compared to equivalent iPhone 16 pricing, depending on the model tier and the tariff environment at the time of launch.

Current estimates place the base iPhone 17 at $899 to $999, a meaningful step up from the iPhone 16’s $799 starting price. The Pro and Pro Max models could see proportionally larger increases given their higher component costs and more complex assembly requirements. Wedbush Securities projected that if Apple were forced to manufacture iPhones entirely in the United States, the cost per unit could reach $3,500, making domestic production economically impractical at any scale.

Apple’s India manufacturing expansion is designed to mitigate these pressures. If the majority of U.S.-bound iPhones originate from India by late 2026, and if the blanket tariff rate remains at 10% rather than the threatened 25%, the price impact on consumers would land at the lower end of projections. Cook has consistently stated that Apple will absorb what it can. But with $3.3 billion already absorbed and costs accelerating, the question is how long that commitment holds before some portion gets passed through to the consumer.

Apple’s Financial Fortress: Q1 FY2026 Earnings

Apple’s fiscal first quarter of 2026 (October through December 2025) demonstrated exactly why the company can absorb tariff pain that would cripple most competitors. Revenue hit $143.8 billion, up 16% year over year and a new all-time record. iPhone revenue reached $85.3 billion, growing 23% as the iPhone 16 cycle exceeded expectations. Services revenue set its own record at $30 billion, climbing 14%. Operating cash flow hit $53.9 billion for the quarter.

Gross margin came in at 48.2%, up from 46.9% a year earlier, despite the escalating tariff burden. Net income reached $42.1 billion, or $2.84 per share, beating consensus estimates by 6.3%. Greater China revenue surged 38% to $25.53 billion, a notable acceleration that suggested Apple’s position in the Chinese market was strengthening even as geopolitical tensions escalated. TECHi’s Apple Stock Today tracker provides real-time updates on these financial metrics.

| Metric | Q1 FY2026 | Q1 FY2025 | Change |

|---|---|---|---|

| Revenue | $143.8B | $124.3B | +16% |

| iPhone Revenue | $85.3B | $69.1B | +23% |

| Services Revenue | $30.0B | $26.3B | +14% |

| Gross Margin | 48.2% | 46.9% | +130bps |

| EPS | $2.84 | $2.40 | +19% |

| Operating Cash Flow | $53.9B | N/A | Record |

These numbers provide the context for understanding why Apple can stomach a $3.3 billion tariff bill without panicking. When you generate $53.9 billion in operating cash flow in a single quarter, $1.4 billion in tariff costs represents a 2.6% drag. Painful, but not existential. The risk is not that tariffs will break Apple in any single quarter. The risk is cumulative erosion of margin over multiple years if costs continue accelerating.

Bull Case: Why Apple Can Absorb the Pain

Apple’s Services segment is the single most important counterweight to tariff pressure. At $30 billion per quarter and growing 14% annually, Services operates at estimated gross margins above 70%, well above the hardware average. Every dollar of revenue that shifts from hardware to Services reduces Apple’s sensitivity to import tariffs. By fiscal 2027, Services is projected to exceed $140 billion in annual revenue, representing more than a third of total sales.

The India transition, while expensive in the near term, should reduce tariff exposure by 2027. If India reaches 32% of global iPhone production by fiscal 2026-2027, and India-origin products face a lower tariff rate than China-origin products, the quarterly tariff bill could decline meaningfully from the $1.4 billion peak. Apple’s investments in Indian manufacturing infrastructure are front-loaded costs that pay dividends over a decade.

The Supreme Court’s IEEPA ruling also removed the worst-case scenario from the table. Trump’s May 2025 threat of a 25% tariff on all iPhones not made in the U.S. would have added an estimated $20 billion or more in annual tariff costs if applied to Apple’s full import volume. With the court limiting executive tariff authority, that existential threat receded. The current 10% blanket tariff, while costly, is manageable within Apple’s margin structure. Investors tracking broader stock market conditions can see how tariff uncertainty has affected the entire tech sector.

Bear Case: The $20 Billion Scenario

The math behind the $20 billion figure requires no exotic assumptions. Apple paid $3.3 billion in tariffs through the end of 2025. If the quarterly run rate holds at $1.4 billion under the current tariff regime, calendar year 2026 alone adds another $5.6 billion. Through 2027, the cumulative direct tariff cost would reach approximately $14.5 billion. Add in the higher production costs from India (5% to 8% premium over China on roughly $100 billion in annual iPhone manufacturing costs), the capital expenditure on new facilities, and the logistics premium of a multi-country supply chain, and the $20 billion threshold is breached well before the end of the decade.

The bear case further assumes that tariff rates could increase rather than decrease. The Section 122 authority invoked after the Supreme Court ruling has a two-year sunset provision, but Congress could extend or replace it. A second Trump term scenario, or bipartisan consensus on China trade restrictions, could result in tariff rates that make the current 10% look generous. The political incentive to appear tough on trade with China shows no signs of fading from either party.

Meanwhile, Apple’s valuation leaves limited room for margin compression. At a forward P/E above 31 and a market cap of $3.69 trillion, investors are pricing in continued margin expansion. If tariff costs eat into that expansion, or worse, cause margins to contract, the stock’s premium multiple becomes harder to justify. TECHi’s analysis of Apple’s downside valuation risks explores what a sustained margin compression scenario could mean for the share price.

AAPL Stock Technical Snapshot

Apple shares are trading near $250 as of early April 2026, well below the 52-week high of $288.62 set during the October 2025 rally and roughly 48% above the 52-week low of $169.21. The stock has pulled back alongside the broader market, with the S&P 500 down approximately 5.8% year to date and the Nasdaq off 8.1%.

Of the 31 analysts covering AAPL, the consensus rating is Buy with an average 12-month price target of $295.31, implying roughly 17% upside from current levels. The next major catalyst is Q2 FY2026 earnings on April 30, 2026, where investors will get the first detailed look at tariff costs under the post-Supreme Court regime. WWDC 2026 (June 8-12) represents another potential catalyst if Apple Intelligence 2.0 delivers a compelling AI roadmap. For the broader market context, check TECHi’s outlook on what to expect from the stock market in 2026.

Price: ~$250 | Market Cap: $3.69T | P/E (Forward): 31.8x

52-Week Range: $169.21 – $288.62 | Avg. Price Target: $295.31

Next Earnings: April 30, 2026 | Dividend Yield: ~0.5%

How Investors Should Position Around Tariff Risk

The April 30 earnings call will be the most important data point for Apple investors this quarter. Management’s guidance on tariff costs under the new Section 122 framework will determine whether the $1.4 billion quarterly run rate is the new baseline or an anomaly tied to the old tariff structure. Investors should listen for three signals: updated quarterly tariff cost projections, any indication of consumer price increases on upcoming products, and progress updates on the India manufacturing transition timeline.

For long-term holders, Apple’s tariff exposure is a headwind, not a thesis-breaker. The Services flywheel, installed base growth exceeding 2.5 billion active devices, and the upcoming Apple Intelligence product cycle provide multiple growth vectors that can outpace tariff drag. For new positions, the pullback from $288 to $250 offers a more attractive entry point, but sizing should account for the earnings uncertainty on April 30.

Investors also watching Nvidia’s insider selling patterns and broader tech stock valuations will notice a common theme across the sector: elevated multiples meeting rising cost pressures. Apple is better positioned than most to navigate this environment, but the company is not immune to it. Portfolio construction that acknowledges tariff risk across the entire tech sector, not just Apple, is the more prudent approach heading into mid-2026.

The Bottom Line

Apple’s tariff problem is not a crisis. It is a structural cost that compounds over time. The $3.3 billion already absorbed is manageable for a company generating $42 billion in quarterly profit. But compounding $5 billion or more per year in tariff and supply chain costs, while simultaneously funding a multi-billion dollar manufacturing migration to India, tests even Apple’s legendary financial resilience. The $20 billion cumulative figure is not inevitable, but it is plausible under current policy trajectories.

Cook has played the hand well so far. He secured tariff exemptions when they were available, absorbed costs to protect demand, announced a politically shrewd $500 billion investment pledge, and accelerated the India shift faster than anyone expected. The Supreme Court ruling gave Apple a legal ceiling on tariff escalation that provides planning certainty the company did not have six months ago. If the April 30 earnings call shows tariff costs stabilizing or declining under the new framework, the $20 billion bear case becomes less likely and AAPL’s premium multiple becomes easier to defend.

But make no mistake: this is the most expensive trade policy environment Apple has ever operated in, and the costs are still being counted.

How much has Apple paid in tariffs so far?

Apple has absorbed approximately $3.3 billion in tariff-related costs from April through December 2025, as disclosed across three quarterly earnings calls. The quarterly cost accelerated from roughly $800 million in the June 2025 quarter to $1.4 billion in the December 2025 quarter.

Will the iPhone 17 be more expensive because of tariffs?

Analysts project tariff-related costs could add between $100 and $350 to iPhone 17 models compared to iPhone 16 pricing. The base iPhone 17 is currently estimated at $899 to $999. The final impact depends on the tariff rate in effect at launch and the proportion of units manufactured in India versus China.

What did the Supreme Court tariff ruling mean for Apple?

The February 2026 Supreme Court ruling struck down Trump’s IEEPA-based reciprocal tariffs as unconstitutional. However, Trump immediately imposed a new 10% blanket tariff under Section 122 of the Trade Act of 1974. For Apple, the ruling removed the threat of a 25% tariff on iPhones but introduced a new flat-rate tariff with no product exemptions.

How much of iPhone production has moved to India?

As of early 2026, India accounts for approximately 25% of global iPhone production, up from less than 5% four years ago. In 2025, Indian factories assembled roughly 55 million iPhones. Apple targets moving the majority of U.S.-bound iPhone production to India by the end of 2026.

Could Apple’s tariff costs really reach $20 billion?

The $20 billion figure represents a cumulative estimate through the end of the decade under current tariff rates. Apple has already paid $3.3 billion. At the current quarterly run rate of $1.4 billion, annual costs exceed $5 billion. Adding supply chain restructuring expenses, India production premiums, and logistics costs, the cumulative total could approach or exceed $20 billion by 2030.

Disclaimer: This article is for informational purposes only and does not constitute investment advice, a recommendation, or a solicitation to buy or sell any securities. The financial data, projections, and analysis presented reflect publicly available information and the editorial judgment of TECHi’s research team. All investors should conduct their own due diligence or consult a qualified financial advisor before making investment decisions. Past performance is not indicative of future results. TECHi and its authors may hold positions in the securities discussed.