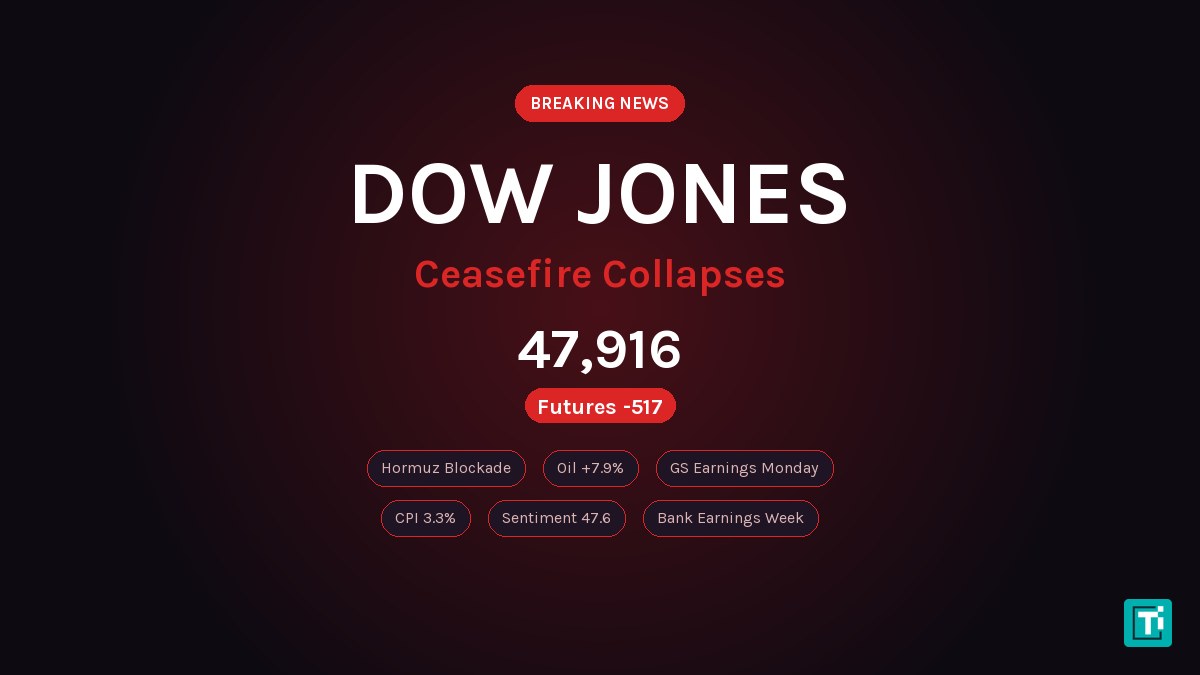

Dow futures dropped as much as 517 points overnight after Vice President JD Vance left Islamabad without a deal and President Trump ordered the U.S. Navy to blockade the Strait of Hormuz. The two-week ceasefire that had powered the Dow to a 3% weekly gain and its best five-day stretch since November 2025 lasted exactly five days before unraveling.

WTI crude surged 7.9% to $104.23 per barrel in Sunday evening trading. Brent jumped 6.7% to $101.59. Asian markets opened lower across the board: the Nikkei fell 0.72%, the Kospi dropped 0.73%, and the Hang Seng lost 0.71%. By early Monday morning ET, Dow futures had pared losses to roughly 256 points, but the damage to the ceasefire trade was done.

Last updated: April 13, 2026 at 11:00 AM ET

Table of Contents

How the Dow Got Here: Five Days From Fear to Euphoria and Back

Monday, April 6, started cautiously. The Dow gained 165 points to close at 46,669.88, buoyed by a solid March jobs report (178,000 new positions, unemployment steady at 4.3%) and whispers that Pakistan was mediating between Washington and Tehran. Tuesday drifted lower by 85 points as traders watched the clock tick toward Trump’s 8 PM ET deadline to strike Iranian power plants.

Then came Wednesday. Barely an hour before the deadline, the ceasefire was announced. The Dow exploded 1,325 points higher, a 2.85% single-session gain that represented its best day since April 2025. Oil collapsed 16.4% to $94.41 per barrel. Market breadth was overwhelming: 412 of 503 S&P 500 components advanced, with industrials leading sectors at +3.75%.

Thursday extended the rally by another 275 points to 48,185.80. That session carried a milestone: the Dow turned positive for 2026 for the first time since the Iran conflict began, briefly touching +0.25% year-to-date after spending weeks in the red.

Friday brought the first cracks. The March CPI report landed at 3.3% headline year-over-year, driven by a 21.2% monthly gasoline price surge, one of the largest single-month gasoline increases in decades. The University of Michigan Consumer Sentiment Index hit an all-time record low of 47.6. The Dow gave back 269 points to close at 47,916.57, but still held a 3% weekly gain.

Now that gain is at risk.

The Hormuz Blockade: What It Means for Markets

The Strait of Hormuz carries roughly 20% of global crude supply. A full U.S. Navy blockade does not merely disrupt Iranian exports; it introduces friction into the entire Persian Gulf shipping corridor that Saudi Arabia, Iraq, Kuwait, and the UAE depend on. The immediate market response, oil up nearly 8%, reflects that calculus.

For the Dow specifically, the transmission mechanism runs through two channels. First, energy costs. The March CPI already showed what happens when oil spikes: gasoline prices surge, headline inflation jumps, and consumer spending gets squeezed. If WTI sustains above $100, the 3.3% CPI reading from March will look like a warm-up. Second, tariff-sensitive industrials. Boeing, Caterpillar, and 3M, which collectively represent over 25% of the Dow’s price-weighted index, are already absorbing costs from the 15% Section 122 universal surcharge. Adding an energy shock on top of a tariff shock compresses margins from both ends.

Goldman Sachs Kicks Off Bank Earnings Monday

Goldman Sachs (GS) reports Q1 2026 results before the opening bell Monday morning, making it the first major bank to face investors in a quarter defined by geopolitical volatility. Wall Street consensus sits at approximately $17.0 billion in revenue (+12.9% year-over-year) and approximately $16.41 to $16.48 earnings per share (+16% year-over-year).

The number to watch is the M&A advisory pipeline. Goldman advised on $1.6 trillion in announced M&A deal volume in 2025. The question is how much of that backlog converted to realized fees in Q1, particularly given the uncertainty that the Iran conflict injected into corporate decision-making. Fixed-income trading revenue should be strong, as geopolitical volatility tends to boost institutional client activity.

The rest of the week brings JPMorgan Chase ($48.2 billion revenue expected, +6.4% year-over-year), Citigroup ($23.6 billion, +9%), and Wells Fargo on Tuesday, followed by Morgan Stanley and Bank of America on Wednesday. JPMorgan guided for net interest income plateauing at approximately $104.5 billion for full-year 2026, while investment banking fees are expected to jump as much as 18% year-over-year, at the high end of management guidance.

Financial stocks carry outsized weight in the Dow. JPMorgan alone is the second-largest component by price. If the big banks deliver strong numbers, it could offset some of the geopolitical selling pressure. If they signal deteriorating credit quality or corporate borrowers pulling back, the selloff deepens.

Consumer Sentiment at Record Lows: The Dow’s Demand Problem

The April University of Michigan reading of 47.6 was not just below consensus. It was below the previous all-time low of 50.0 set in June 2022 during peak Biden-era inflation. One-year inflation expectations jumped a full percentage point to 4.8%, the largest monthly increase since April 2025. Five-year expectations rose to 3.4%.

Nearly all of those survey responses (98%) were collected before the ceasefire was announced, which means the April reading reflects maximum fear conditions. But with the ceasefire now collapsed and oil surging again, the May reading could deteriorate further.

This hits Dow consumer components directly. Nike dropped 3.14% on Friday to $42.62 after cautious forward guidance on China demand had already taken the stock down over 15% in recent weeks. Walmart faces rising supplier prices. Disney, Coca-Cola, McDonald’s, and Procter & Gamble all depend on discretionary consumer spending that a $5.50-per-gallon gasoline environment suppresses.

Technical Levels: Where the Dow Finds Support

The Dow rejected the 48,000-48,220 resistance zone on Thursday and has been selling off since. If Monday’s pre-market losses carry into the regular session, the first meaningful support sits at 46,670 (Monday’s closing level before the ceasefire rally). Below that, technical analysts at OANDA’s MarketPulse identify 45,244 as a major technical pivot, the 100% measured move of the 2022 sell-off. The psychological floor is 45,000.

On the upside, the 50,000 level that the Dow stalled at earlier in 2026 remains the major target. OANDA’s MarketPulse characterizes the Dow as a potential value haven if investors rotate out of overvalued growth names and into industrial and financial blue chips, but that thesis requires energy costs to stabilize, something a Hormuz blockade makes significantly harder.

The Tariff Clock Is Ticking Too

Behind the geopolitical headlines, a policy deadline is approaching. The 15% Section 122 universal surcharge expires on July 24, 2026. The administration must either negotiate new trade agreements or get congressional approval to extend it. The effective U.S. tariff rate has already risen to 10.3%, up from 2.4% in 2024, the highest level since 1947 according to the Penn Wharton Budget Model. The average household is absorbing an estimated $1,500 annual tax increase from tariffs alone.

Caterpillar, directly exposed to 25% China duties, edged up roughly 0.43% on Friday, but the stock remains vulnerable if trade tensions escalate alongside the military situation. On April 10, the U.S. Trade Representative outlined proposed 25% duties on certain electronics and auto parts, adding another layer of cost pressure to Dow industrial components.

What Monday’s Session Will Tell Us

The Dow enters Monday carrying the weight of a collapsed ceasefire, a naval blockade of the world’s most important oil chokepoint, record-low consumer confidence, and a CPI report that showed inflation re-accelerating. Against that, Goldman Sachs earnings could remind the market that corporate America is still generating substantial revenue growth, and the Fed has signaled it will look through supply-driven price shocks.

The week ahead represents the most consequential five sessions for the Dow since the Iran conflict began. If the index holds above 46,000 through the bank earnings gauntlet while absorbing a Hormuz blockade, it demonstrates the kind of fundamental resilience that justifies MarketPulse’s value-haven thesis. If it breaks 45,000, the entire ceasefire rally was a dead-cat bounce inside a broader selloff that has been building since the Dow failed at 50,000 earlier this year.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. TECHi and its authors may hold positions in securities mentioned. Always conduct your own research and consult a licensed financial advisor before making investment decisions.

Why are Dow Jones futures falling on April 13?

Dow futures dropped as much as 517 points after the U.S.-Iran ceasefire collapsed over the weekend. VP JD Vance left Islamabad without a deal, and President Trump ordered the U.S. Navy to blockade the Strait of Hormuz, sending oil prices surging nearly 8%.

What did the Dow Jones close at on Friday?

The Dow Jones Industrial Average closed at 47,916.57 on Friday, April 10, 2026, down 269 points (-0.56%) for the session but up 3% for the week, its best weekly performance since November 2025.

Which bank stocks report earnings this week?

Goldman Sachs reports Monday April 13. JPMorgan Chase, Citigroup, and Wells Fargo report Tuesday April 14. Morgan Stanley and Bank of America report Wednesday April 15. Consensus expects Goldman Sachs revenue of $16.9 billion (+12% YoY) and JPMorgan revenue of $48.2 billion (+8% YoY).

How does the Hormuz blockade affect the Dow?

The Strait of Hormuz carries roughly 20% of global crude supply. A blockade pushes oil prices higher (WTI surged 7.9% to $104.23), which increases energy costs for consumers and businesses. This hits Dow industrials like Boeing, Caterpillar, and 3M through higher input costs, and consumer stocks like Nike, Walmart, and Disney through reduced discretionary spending.

Is the Dow Jones positive for 2026?

The Dow briefly turned positive for 2026 on Thursday April 9 at +0.25% YTD after the ceasefire rally, and closed Friday at roughly +1.3% YTD. However, Monday futures losses from the ceasefire collapse threaten to push the index back into negative territory for the year.