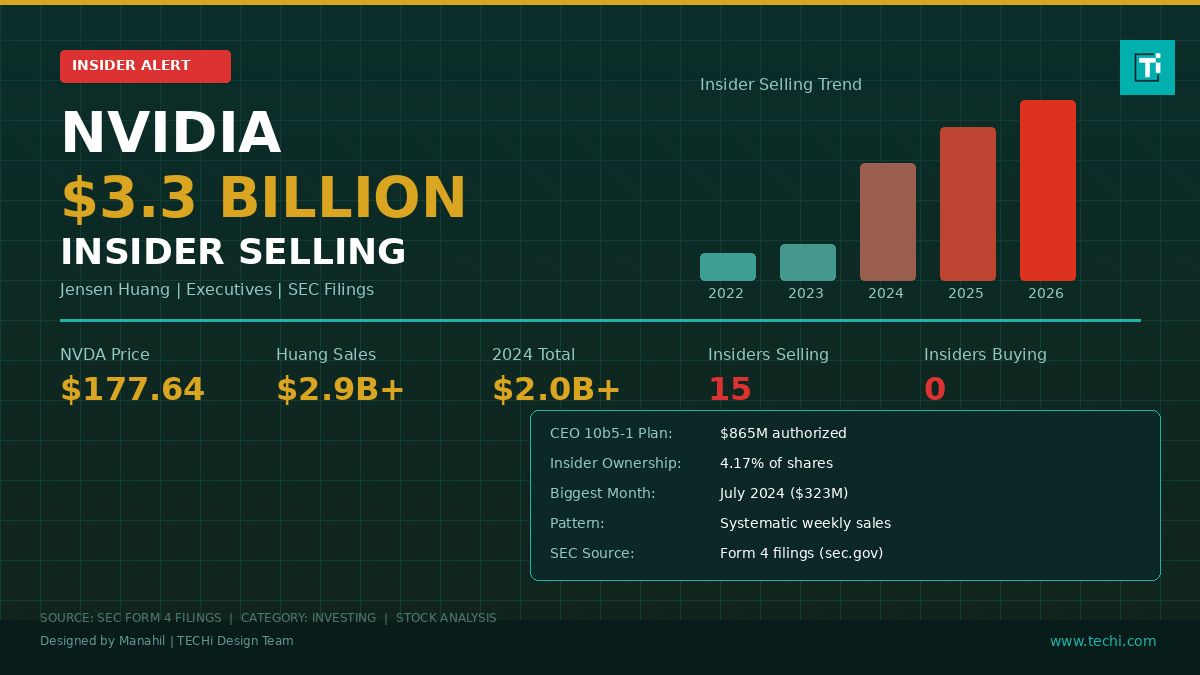

Fifteen Nvidia insiders have filed SEC Form 4 disclosures over the past 18 months. Zero have reported a single share purchase. The aggregate value of those sales now exceeds $3.3 billion, with CEO Jensen Huang alone accounting for roughly $2.9 billion of the total. For a stock trading at $177.64 and carrying a forward P/E in the mid-to-high 30s, the signal from the executive suite is worth dissecting.

Key Takeaways

- 15:0 Sell Ratio Fifteen insiders sold shares while zero bought on the open market over 18 months, one of the most lopsided ratios in the S&P 500.

- $2.9B CEO Sales Jensen Huang alone has sold more than $2.9 billion in Nvidia shares through systematic 10b5-1 trading plans since mid-2024.

- $3.3B+ Total Aggregate insider dispositions across all reporting executives and directors have surpassed $3.3 billion since early 2024.

- 10b5-1 Plans All sales were executed under pre-arranged Rule 10b5-1 plans, but the timing and scale of plan adoptions remain informative signals.

- Accelerating Pace Insider sales rose from $462M in 2023 to $2B+ in 2024, with 2025-2026 on track to match or exceed that pace despite the stock retreating from highs.

Table of Contents

The Numbers Behind Nvidia’s Insider Exodus

The scale of insider selling at Nvidia has escalated in lockstep with the stock’s AI-fueled rally. In fiscal year 2023, total insider dispositions amounted to roughly $462 million. By 2024, that figure surged past $2 billion as NVDA shares breached $140 on a post-split basis. Through the first quarter of 2026, the running total across all reporting insiders has climbed past $3.3 billion, according to SEC Form 4 filings compiled by financial data trackers.

The pattern is consistent and broad-based. Executives, board members, and officers have all participated in the selling, though the magnitude varies widely by individual. What makes the current wave notable is not just the dollar amounts; it is the complete absence of open-market purchases by any insider during the same period. When 15 named insiders file sales and none file buys, the directional consensus is hard to ignore.

For context, the S&P 500 itself has pulled back from its February 2025 highs and currently sits around $658.93 on the SPY ETF. Nvidia’s stock, at $177.64, remains well above its 2024 lows but has retreated from the October 2025 peak near $212. The insiders who sold near those highs locked in significantly better prices than what the market offers today. TECHi’s comprehensive Nvidia stock analysis tracks the full valuation picture.

Jensen Huang’s $2.9 Billion Selling Spree

Jensen Huang is Nvidia’s co-founder, president, and CEO. He is also, by a wide margin, the company’s most prolific stock seller. Bloomberg reported on October 31, 2025 that Huang had completed a $1 billion share sale plan, bringing his cumulative dispositions to more than $2.9 billion. That figure encompasses sales executed between mid-2024 and late 2025 through a series of pre-arranged 10b5-1 trading plans.

The selling has been systematic. Between June and September 2024, Huang sold more than $700 million worth of shares. In May 2025, Barron’s reported that Huang had filed a new 10b5-1 plan authorizing the sale of up to 6 million additional shares, valued at approximately $865 million at the time of filing. The execution pattern followed a predictable rhythm: weekly sales of 25,000 to 75,000 shares, typically on Tuesdays and Wednesdays, at prices ranging from $120 to $210 per share depending on the timing.

Huang’s biggest single month was July 2024, when he unloaded $322.7 million in one batch. Yahoo Finance noted at the time that the sale brought his summer total to nearly $500 million, a figure that would have been unthinkable just two years earlier when Nvidia was a $300 billion company rather than a $4 trillion one.

The Full Roster: Who Else Is Selling

Huang is the headline, but the selling extends deep into Nvidia’s leadership. SEC Form 4 filings from December 2025 through March 2026 alone reveal more than $450 million in sales from other executives and directors. Here is how the activity breaks down across the most active sellers:

| Insider | Title | Recent Sales | Estimated Value |

|---|---|---|---|

| Jensen Huang | President & CEO | Systematic weekly sales (2024-2026) | $2.9B+ cumulative |

| Ajay K. Puri | EVP, Worldwide Field Ops | 800,000 shares (Jan-Mar 2026) | ~$148M |

| Mark A. Stevens | Director | 571,682 shares (Dec 2025-Mar 2026) | ~$102M |

| Harvey C. Jones | Director | 250,000 shares (Dec 2025) | ~$44.3M |

| Debora Shoquist | EVP, Operations | 229,840 shares (Dec 2025) | ~$41.4M |

| Colette Kress | EVP & CFO | Multiple sales (Jan-Mar 2026) | ~$28M |

| Donald F. Robertson Jr. | Principal Accounting Officer | 80,000 shares (Jan 2026) | ~$15.2M |

| A. Brooke Seawell | Director | 12,728 shares (Dec 2025) | ~$2.3M |

EVP Ajay Puri’s $148 million in sales across three months stands out. Puri, who oversees Nvidia’s global sales operations, has arguably the best real-time visibility into enterprise AI spending. Director Mark Stevens, a venture capitalist and long-time board member, disposed of more than $100 million between December 2025 and March 2026. Even CFO Colette Kress, who is legally required to be among the most cautious sellers, filed multiple dispositions totaling roughly $28 million.

TECHi previously covered a similar pattern in our analysis of combined insider sales at Nvidia and Palantir totaling $12.6 billion, which flagged the trend as a potential valuation warning signal back in December 2025.

Why Insiders Sell: The 10b5-1 Defense

Every time insider selling makes headlines, the same rebuttal surfaces: these are pre-planned sales under Rule 10b5-1 trading plans, which means the insiders are not acting on material nonpublic information. The defense has merit. Under SEC rules adopted in 2023 (strengthening the original 2000 rule), insiders must adopt trading plans during an open trading window and impose a mandatory cooling-off period of 90 days before the first trade executes. Plans must be entered in good faith, and insiders cannot have overlapping plans.

The existence of a 10b5-1 plan does not mean the selling is uninformative. Insiders choose when to adopt plans, how many shares to include, and what price triggers to set. A CEO who files a plan to sell 6 million shares at a time when his stock is near all-time highs is making a deliberate portfolio decision, regardless of whether the actual executions are automated. Academic research from Stanford and MIT has found that 10b5-1 plan adoptions themselves predict negative excess returns over the following 6 to 12 months, particularly when multiple insiders adopt plans within a short window.

The broader trend across the tech sector supports this interpretation. As TECHi documented in our coverage of tech titans dumping billions in stock during 2025, Nvidia was far from the only company experiencing a wave of insider dispositions. The pattern was particularly concentrated among AI-linked names.

What History Says About Insider Selling at AI Peaks

Insider selling spikes at technology inflection points are not new. Cisco Systems executives sold aggressively throughout 1999 and early 2000, right before the company’s stock declined 80% from its dot-com peak. Intel insiders ramped up sales ahead of the 2015-2016 slowdown in the PC market. More recently, Zoom Video Communications insiders sold more than $2 billion in stock during 2020-2021, shortly before the work-from-home premium evaporated and shares fell from $560 to under $60.

None of these parallels are perfect fits. Nvidia’s revenue growth trajectory, driven by data center GPU demand from hyperscalers, is fundamentally stronger than Zoom’s pandemic-driven spike or Cisco’s switch-selling business in 2000. The question is not whether Nvidia is “the next Cisco,” because it almost certainly is not. The question is whether a stock priced for near-perfect execution across the next three years has adequately discounted the risks that its own executives appear to be hedging against.

Billionaire investors outside of Nvidia have also taken notice. Hedge fund manager David Tepper sold portions of his Nvidia position in a move that TECHi analyzed in David Tepper’s Nvidia and Amazon sales: AI warning or smart profit-taking.

The Bull Case: Why Insider Selling Might Not Matter

There are legitimate reasons to discount insider selling as a standalone signal. First, Nvidia’s executives hold positions that are wildly concentrated relative to their personal net worth. Jensen Huang’s Nvidia stake is worth north of $150 billion. Selling $2.9 billion represents approximately 1.9% of that position; any financial advisor would recommend far more aggressive diversification. Second, the sales occur against a backdrop of genuine operational momentum: Nvidia reported Q4 FY2025 data center revenue of $35.6 billion, a year-over-year increase of 93%. The Blackwell GPU architecture is shipping in volume, the Vera Rubin platform is in development, and the company’s $1 trillion order backlog provides substantial revenue visibility.

Third, insider selling at mega-cap technology companies is structurally higher than at smaller firms because executive compensation at this scale is overwhelmingly equity-based. Stock options and RSUs that vest on a schedule create a constant flow of taxable events that require selling. When a company’s stock price has appreciated 2,000% over five years, even routine option exercises generate headline-grabbing dollar amounts.

For a detailed look at Nvidia’s product roadmap and forward catalysts, see TECHi’s Nvidia stock forecast and analysis for 2026, which covers the Vera Rubin architecture and $1 trillion backlog thesis.

The Bear Case: Valuation Meets Distribution

The counter-argument is more nuanced than “insiders are selling so the stock must drop.” The bear case rests on three pillars. First, the selling is not random diversification; it is accelerating. Insider sales rose from $462 million in 2023 to $2 billion in 2024 to a pace that extrapolates well above $2 billion again in 2025-2026. If insiders believed the best gains were still ahead, the rational strategy would be to defer sales and capture more upside. Instead, the cadence is quickening.

Second, the insider ownership percentage has been steadily declining. At roughly 4.17% (as of Q4 2025 filings), Nvidia insiders now hold a smaller fraction of the company than insiders at most comparable semiconductor firms. As ownership shrinks, the alignment of incentives between management and shareholders becomes a progressively more relevant concern for institutional holders.

Third, Nvidia’s valuation assumes a sustained AI spending cycle with limited competition erosion. Custom silicon from hyperscalers (Google’s TPU, Amazon’s Trainium, Microsoft’s Maia), plus AMD’s MI300X gaining traction and Intel’s Gaudi 3, all represent share loss vectors that could materialize over the next 18 to 24 months. Insiders may simply be pricing in a wider range of outcomes than the consensus $265 price target suggests.

Nvidia Stock Technical Snapshot

NVDA shares closed at $177.64 on the most recent trading session, sitting roughly 16% below the October 2025 all-time high of $212.19. The stock has found support near the $170-$175 range multiple times since February 2026, while the 200-day moving average continues to rise, currently near $160. Volume has been consistent, averaging above 100 million shares daily. For daily price updates, check TECHi’s Nvidia stock today tracker.

How Retail Investors Should Read Form 4 Filings

SEC Form 4 filings are publicly available on the SEC’s EDGAR database within two business days of the transaction. Retail investors looking to track insider activity should focus on several key signals rather than individual transactions.

Cluster selling, where multiple insiders sell within a short window, carries more predictive weight than isolated sales. The buy-to-sell ratio matters more than the absolute dollar amounts; a company where five insiders buy and two sell sends a very different message than one where fifteen sell and zero buy. Transaction type is also important: open-market purchases (where insiders spend their own money) are far more bullish than option exercises, which are often tax-driven.

For Nvidia specifically, every insider sale in the past 18 months has been a planned disposition or option exercise, not a spontaneous open-market sale. But the absence of any open-market buying, even at prices 16% below all-time highs, is the signal that sophisticated investors pay the most attention to.

The Bottom Line

Nvidia’s insider selling tells a story of deliberate, sustained portfolio reduction by the people with the best information about the company’s future. Jensen Huang has monetized roughly $2.9 billion of his position. His direct reports and board members have collectively added another $400 million or more in recent months. The 15-to-0 sell-to-buy ratio is among the starkest in mega-cap tech.

Does that mean NVDA is a sell? Not necessarily. Insider selling is a necessary but not sufficient condition for bearishness. The AI spending cycle is real, the Blackwell architecture is generating record revenue, and Nvidia’s competitive moat in training-grade GPUs remains wide. But retail investors who are adding to positions at $177 should at least ask why the people running the company are moving in the opposite direction.

The most recent CNBC report confirmed that Nvidia insiders sold more than $1 billion in shares over just one year, and that pace has only accelerated since. TECHi’s analysis of the $20 billion Nvidia-Groq deal explores how acquisitions fit into the broader AI strategy that insiders are simultaneously selling into.

How much Nvidia stock have insiders sold in total?

Nvidia insiders have sold more than $3.3 billion in stock over the past 18 months, according to SEC Form 4 filings. CEO Jensen Huang accounts for roughly $2.9 billion of that total, with the remaining $400 million-plus coming from executives including EVP Ajay Puri, CFO Colette Kress, EVP Debora Shoquist, and multiple board directors.

Why is Jensen Huang selling Nvidia stock?

Huang sales are executed through pre-arranged 10b5-1 trading plans, which are designed to allow insiders to sell shares on a predetermined schedule without acting on material nonpublic information. His most recent plan, filed in May 2025, authorized the sale of up to 6 million shares worth approximately $865 million.

Are any Nvidia insiders buying stock right now?

No. Over the trailing 18 months, zero Nvidia insiders have reported open-market purchases of company stock. Fifteen insiders have filed sales during the same period, creating a 15-to-0 sell-to-buy ratio.

Is insider selling a reliable indicator that a stock will drop?

Insider selling alone is not a reliable sell signal. Research shows that cluster selling by multiple insiders within a short period is more predictive than individual transactions. The absence of any insider buying is often considered a stronger signal.

What is the analyst price target for Nvidia stock in 2026?

The median 12-month analyst price target for Nvidia is $265 per share as of early April 2026, implying roughly 49% upside from the current price of $177.64.