A billionaire hedge fund manager, David Tepper, sold off his shares in Nvidia and Amazon in the fourth quarter of 2025 and this led to questions about the potential lurking dangers behind artificial-intelligence and cloud-computing giants.

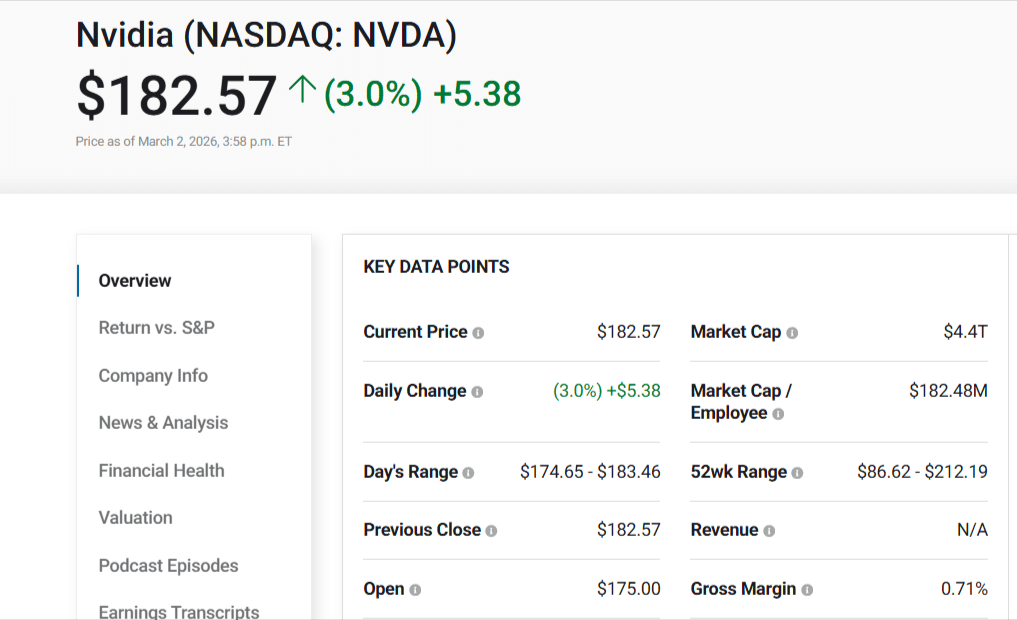

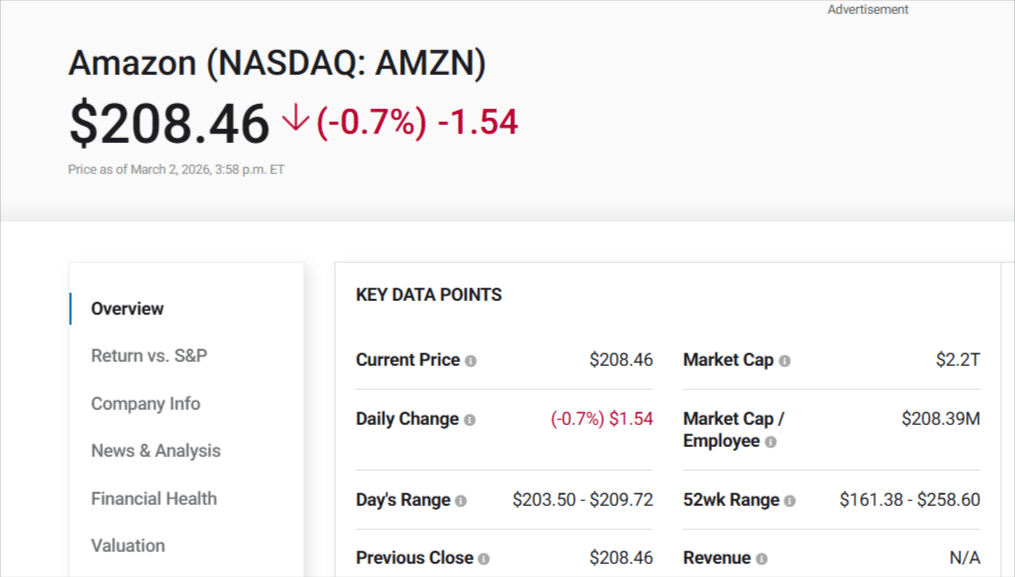

Nvidia is trading at $182.57, with a rise of 3.0% shares per day, and Amazon is trading at $208.46; both securities are showing slight year to year growth, but they are still lower than their prior highs.

Old News, Smart Profits

The revealed 13F reports were announced forty-five days following the fiscal quarter encompassing the portfolio adjustments undertaken in late 2025 as a result of market uncertainties attributed to the tariff policies by President Trump.

In both instances, the liquidation of its Nvidia positions to an estimated 1.7 million shares, and the sale of its Amazon shares by 13%, likely to achieve profits following the Nvidia, with Q2, 2025 gush, were head-cutting measures.

The lack of full divestiture is not an indication of bearishness but it is a tactical selling of stocks whose price to sales ratio is greater than 26 by the peers of Nvidia and a stable yet less aggressive growth by Amazon.

Betting Big on AI Backbone

For Micron Technology, Inc., Tepper's Appaloosa became extremely popular. According to the filing, Micron shares increased by an astounding 250%, with Appaloosa adding precisely 1,000,000 shares over the course of the quarter.

The fund currently owns 1.5 million shares of Micron, which is worth more than $428 million. Tepper seems to be going "down the stack," looking for value in the AI-powering hardware rather than the chip designers.

Outlook

Recent investment circles have shown the shift of the existing focus of AI leadership toward the focus on the key players in the dynamics of the supply-chain dynamics. Micron Technology has become a critical beneficiary with its revenue stream recording a sharp and sustained upward trend that can be ascribed to the sustained capital investment in data-center infrastructure.

At the same time, the competition base of Nvidia in the field of graphics processing units is only getting stricter, and the lack of memory supplies only strengthen the strategic location of Micron. It is reasonable to conclude that, with the ongoing surge in spending on artificial-intelligence infrastructure, memory licensors will have an opportunity to obtain sustainable, multi-year growth precedents.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Warisha Rashid writes about the intersection of corporate strategy, venture capital, and macro for TECHi — why certain acquisitions close when the Fed pivots, why a Series C prices at a markdown, and how capital rotation reshapes competitive positioning. She reads PitchBook, CB Insights, and S&P Capital IQ filings alongside the earnings commentary most coverage ignores. Her work focuses on M&A rationale, startup unit economics, and the policy signals that move private markets before they show up in public ones.