- Price contextTSLA closed May 13, 2026 at $445.27, up 2.73%, with traders looking for follow-through during the Trump-Xi summit window.

- Original angleThe Beijing meeting is not only a diplomacy story; it is a test of whether Tesla's China exposure deserves a lower risk discount.

- What moves the stockTariff language, FSD approval progress, and Shanghai export/demand data matter more than Musk's visibility in the delegation.

- Investor readTesla can keep a China meeting premium only if political access turns into measurable policy or regulatory signal.

This article is market commentary for informational purposes only. It is not investment advice, a price target, or a recommendation to buy or sell TSLA stock.

Tesla stock is no longer trading only on Cybercab, Optimus, delivery volume, or the next software demo. The immediate question for TSLA stock is whether Elon Musk's seat inside President Donald Trump's China delegation can turn diplomatic theater into a lower-risk China story. The stock gave traders a head start: TSLA closed at $445.27 on May 13, 2026, up 2.73%, and was indicated higher in May 14 premarket trading before the U.S. regular session opened.

The new angle is simple: this is not just a meeting story. It is a multiple story. Tesla's valuation already prices the company as more than a carmaker. What the Beijing trip can change, if it changes anything, is the market's willingness to capitalize Tesla's China exposure as an asset again instead of treating it as a political liability.

That distinction matters because China cuts through three separate pieces of the Tesla price: Shanghai production, local demand, and FSD approval. A handshake with Xi Jinping does not fix those pieces by itself. A visible seat at the table can, however, alter how traders frame the next few weeks of headlines.

Why this meeting matters for TSLA price

Reuters reported that more than a dozen CEOs and senior executives joined Trump's China trip, including Tesla and SpaceX CEO Elon Musk. The broader summit is focused on trade, technology, Taiwan, agriculture, and geopolitical pressure points, with Trump and Xi beginning talks in Beijing on May 14 after economic teams reported progress on trade mechanisms, according to Reuters' summit coverage.

For Tesla, the market does not need a signed Tesla-only agreement to react. It needs evidence that China is becoming less hostile to U.S. platform companies with deep local operations. That is why Musk's presence is price-relevant even if no Tesla press release appears from Beijing.

Investors already have a clean reference point on the site: the live TSLA quote page shows the stock still below its 52-week high, with the China meeting arriving after a strong one-day move. The setup is not a depressed stock needing a rescue. It is a momentum stock trying to justify why the next leg higher deserves to be priced now rather than after hard evidence arrives.

The first hard evidence would be regulatory. Tesla said in its Q1 update that it continued to make progress on FSD approval in China, while also reporting $22.39 billion in Q1 revenue, $4.72 billion in gross profit, $941 million in operating income, and $44.74 billion in cash and short-term investments in the quarter ended March 31, 2026, according to its April 22, 2026 investor update filed with the SEC.

That cash position is one reason the stock can absorb political noise better than smaller EV rivals. The China problem is not balance-sheet survival. It is whether a premium-priced, AI-and-autonomy-heavy equity can keep treating China as a growth and software monetization market while local competitors attack the car business from below.

China is a production asset, but not an easy demand story

Tesla's Shanghai factory is still one of the most important assets in the global EV chain. The same Q1 Tesla update listed installed annual manufacturing capacity of more than 950,000 Model 3 and Model Y vehicles in Shanghai, and Tesla also said its Shanghai Megafactory is part of its energy-storage expansion.

That makes China different from a normal export market. Tesla is not simply selling American cars into China. It is using a Chinese production base to serve domestic buyers and overseas markets. If tariffs, export logistics, or technology approvals improve at the margin, the impact can show up in more than one line of the model.

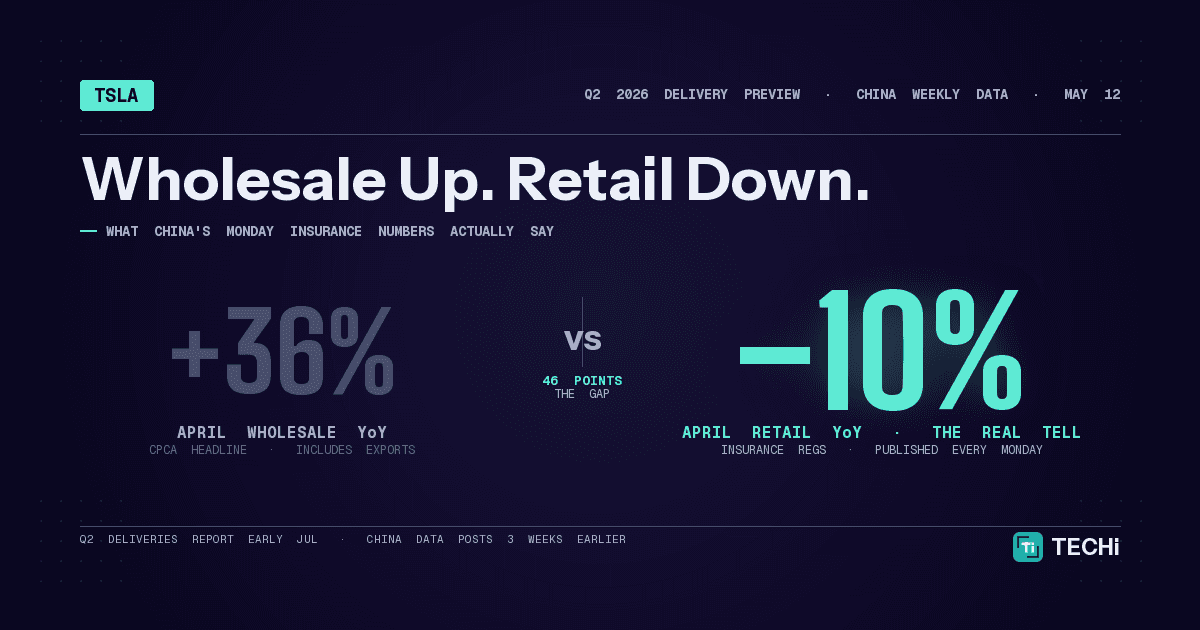

The domestic sales picture is less comfortable. CnEVPost, citing China Passenger Car Association data, reported that Tesla's China retail sales were 25,956 vehicles in April 2026, down 9.66% from a year earlier and down 53.74% from March. The same report said exports from Tesla's Shanghai plant reached 53,522 vehicles in April, the second-highest export figure in its data set.

That split is the meeting's most overlooked price angle. Shanghai is performing as an export machine even while domestic China remains uneven. A tariff or trade-truce improvement helps the export side. A regulatory win on FSD helps the local demand and software side. A photo-op without either still leaves investors with the same mixed China data they had before Air Force One landed.

The competitive pressure is visible in the rankings. CnEVPost's April market-share report showed BYD holding first place in China's passenger NEV retail market with 182,025 units and a 21.4% share, while Tesla fell outside the top 10 for April NEV retail sales. For January through April, Tesla China still ranked fifth in NEV retail sales with 138,754 units and a 5.0% share.

That is why a purely political read is too thin. Musk does not need Beijing to make Chinese consumers stop comparing Tesla to BYD, Xiaomi, Li Auto, Nio, XPeng, or Geely. He needs Beijing to keep the rules predictable enough that Tesla can compete with software, financing, charging, safety data, and manufacturing scale.

The real option is FSD, not another Model Y price cut

Tesla can cut price. China has seen that movie. The stock will not get a durable rerating because investors imagine another round of incentives or financing tweaks.

The more important lever is FSD. In November 2025, Reuters reported that Musk expected full China approval for Tesla's Full Self-Driving software in early 2026, after saying Tesla had partial approval in the market; the same report noted that FSD in China remained short of U.S. capabilities and that Chinese rivals were pushing local driver-assistance features aggressively, often with different pricing structures (Reuters via Investing.com).

That is the part TSLA bulls care about. China is not just a unit-volume market. It is a test of whether Tesla can export its software economics into a jurisdiction where regulators, data rules, mapping, local competition, and consumer expectations all look different from the U.S.

A China FSD path would not immediately make Tesla's valuation easy to defend. It would make the defense cleaner. Investors could connect Shanghai scale, a local installed base, and subscription economics instead of arguing only about vehicle gross margins.

This also explains why the new article should not be framed as Trump helping Musk sell more cars. The better frame is that Trump is trying to reduce a policy discount around U.S. companies that China still wants in the country, while Musk is trying to keep Tesla's AI/software option alive in the world's most competitive EV market.

The price levels that matter now

The current TSLA setup is stretched enough to punish weak news but close enough to its highs to reward a real catalyst. StockAnalysis data showed Tesla with a 52-week range of $273.21 to $498.83, a market cap around $1.67 trillion, and an average analyst price target of $405.47 after the May 13 close. TECHi's own Tesla stock analysis guide already treats the stock as a premium AI, EV, and robotics story, not a low-multiple automaker.

At $445, the market is already above the average target shown by StockAnalysis. That does not make the rally wrong. It does mean the next $50 of upside needs more than diplomatic access. It needs a reason for analysts and portfolio managers to stop penalizing China exposure and start valuing it as a source of software optionality again.

Three near-term price signals matter more than the photo album from Beijing.

First, watch whether the summit produces tariff language that directly helps cross-border manufacturing or EV supply chains. Tesla warned in its March 2026 10-Q that changes in government policies, incentives, or tariffs can affect production, costs, competition, and durable-goods demand, and the company also said 2026 capital expenditures are expected to exceed $25 billion because of AI, compute, data centers, manufacturing, and fleet growth (Tesla 10-Q).

Second, watch whether Chinese regulators offer any practical signal on FSD, data handling, maps, testing scope, or customer access. A vague improvement in diplomatic tone is useful for sentiment. A visible change in approval scope is useful for valuation.

Third, watch weekly China insurance and delivery signals. TECHi is already tracking why Tesla's real Q2 number posts every Monday in China. If those data points keep weakening, the stock can fade even if the summit headlines sound friendly.

The trade: policy optionality, not a clean buy signal

There is a bullish case from here. If the summit stabilizes trade language, if FSD China approval moves closer, and if Shanghai keeps exporting at a high rate, the stock can retest the upper part of its 52-week range. In that case, $498.83 becomes less of a memory and more of a live resistance level.

The base case is less dramatic. Tesla may keep a meeting premium for a few sessions while traders wait for concrete follow-through. That would leave TSLA pinned between a strong narrative and a valuation that already discounts a lot of future AI and autonomy profit.

The bear case is also clear. If the Trump-Xi meeting produces pageantry but no tariff, FSD, or trade detail relevant to Tesla, the stock can give back part of the China premium. The average analyst target below the current price becomes a reminder that TSLA's market value still requires investors to pay today for businesses that are not yet carrying the income statement.

This is why the best investor answer is not a simple buy-or-sell call. Tesla stock has a real catalyst window, but the catalyst is not Musk being visible near power. The catalyst is whether that visibility changes the cost, approval, or demand assumptions that sit inside the TSLA multiple.

For readers comparing this setup with longer-term Tesla scenarios, TECHi's Tesla stock price prediction is the broader roadmap. The Beijing trip is narrower. It is a short-term test of whether political access can bring forward part of the autonomy-and-China thesis that bulls usually place several quarters into the future.

Bottom line for Tesla stock

Musk's trip with Trump gives TSLA stock a better story than it had a week ago. It does not automatically give it better earnings power.

The stock price is reacting to a possibility: China policy risk may be easing just as Tesla is trying to turn Shanghai scale, FSD, energy storage, and AI infrastructure into a wider platform story. That possibility deserves attention because China touches real assets, real volume, and real software upside.

The discipline is to separate signal from access. A photo with the delegation is access. A tariff mechanism, a cleaner FSD path, a data-rule opening, or stronger China retail demand would be signal.

Until the signal arrives, Tesla stock is trading on a China meeting premium. That premium can hold for a few days on sentiment. To last longer, it needs to show up in the next policy readout, the next FSD clue, or the next China delivery data.

FAQ

Frequently asked questions

Why is Tesla stock moving around Trump's China visit?

Tesla stock is reacting to the possibility that a Trump-Xi meeting with Elon Musk in the business delegation could reduce policy risk around China, tariffs, Shanghai exports, or Tesla's FSD approval path.

What TSLA price level matters after the China meeting?

The key upside reference is Tesla's 52-week high near $498.83, while the average analyst target shown by StockAnalysis sits below the May 13 close.

Does Elon Musk's China trip guarantee a Tesla catalyst?

No. The trip creates policy optionality, but TSLA needs a concrete signal on trade, FSD approval, data rules, or China demand to turn meeting momentum into durable valuation support.

What should Tesla investors watch next?

The next signals are any summit language on tariffs or market access, Chinese regulatory signals around FSD, and weekly China delivery or insurance data.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Fatimah Misbah Hussain is a seasoned financial journalist at TECHi, specializing in stock market analysis, commodities, and tech sector finance. With a strong background in monitoring public markets and tech companies, she breaks down complex stock movements and commodity price trends into actionable insights.