Amazon just made the most important logistics announcement of the post-ChatGPT era. The company is opening its entire supply chain — freight, distribution, fulfillment, and parcel shipping — to every business, of every size, through a new offering called Amazon Supply Chain Services. The same infrastructure that moves, stores, and ships goods for hundreds of thousands of Amazon sellers is now available to anyone. The market grasped the implications immediately: AMZN tagged a fresh 52-week intraday high of $278.56, FedEx fell as much as 7.4% (its worst day in over a year), UPS dropped 8.9%, GXO Logistics and Forward Air both fell more than 10%, and Old Dominion Freight Line dropped more than 5%. This is a structural moment, not a tactical one.

- The announcementAmazon Supply Chain Services opens Amazon's end-to-end logistics network — freight, distribution, fulfillment, and parcel — to all businesses, not just Amazon-platform sellers. It bundles capabilities previously available only via FBA, Amazon Freight, Multi-Channel Fulfillment, and Amazon Shipping into a single integrated stack.

- The setupAmazon has spent 25 years and an estimated $250B+ in cumulative logistics capex building one of the most reliable supply chains on Earth. Competitors cannot replicate the scope on any reasonable timeline.

- The collateral damageFedEx -7.4% (worst single-day in over a year), UPS -8.9%, GXO Logistics -10%+, Forward Air -10%+, Old Dominion Freight Line -5%+. Sector-wide, not idiosyncratic — the entire legacy carrier complex re-rated lower in a single session.

- Why this matters nowAGI dramatically lowers the marginal cost of running, optimizing, and selling logistics services. Amazon's scale + AI advantage compounds — exactly when traditional carriers face the highest cost-of-capital environment in 15 years.

- The thesisWinners Take Most — and the gap widens faster in the AGI era. Amazon turns every adjacent market into an extension of its core platform. Logistics is now that adjacent market.

What Amazon Supply Chain Services Actually Is

Amazon Supply Chain Services bundles four capabilities that previously sat behind separate Amazon programs (FBA, Amazon Freight, Amazon Multi-Channel Fulfillment, and Amazon Shipping) into a single integrated stack. Any business — a Shopify merchant, a TikTok Shop brand, a brick-and-mortar retailer, an industrial supplier — can now plug into the same trucking, warehousing, fulfillment, and parcel network that moves Amazon's own goods. Our AMZN coverage hub tracks the full operational footprint behind this announcement.

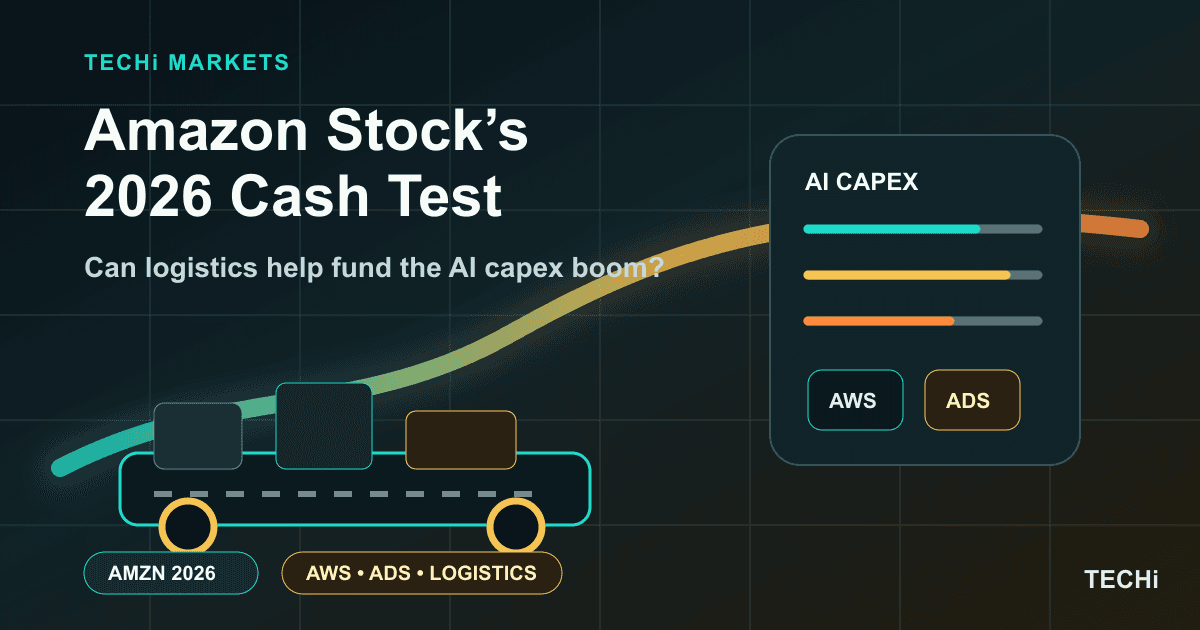

The strategic move is straightforward: take a $250B+ fixed-cost asset already operating to serve internal demand, and turn the unused capacity into a high-margin external revenue line. The economics resemble what AWS did to compute — Amazon built infrastructure for itself, opened it to everyone, and the third-party revenue layer compounded faster than the parent business it was built to serve. The same playbook is what now anchors Amazon's entire $2.93T market cap, and as we explored in our AI capex coverage, it is the dominant pattern across mega-cap technology in the AGI era.

Why FedEx, UPS, GXO, and Forward Air All Collapsed Together

The sell-off across the legacy logistics complex was not surprising — it was inevitable. Investors understood within minutes that every major U.S. carrier now competes against Amazon's full vertical stack for the same customer wallet. FedEx and UPS each saw their worst trading days in over a year. GXO Logistics and Forward Air both dropped more than 10%. Old Dominion Freight Line — a bellwether for less-than-truckload demand — fell more than 5%.

The structural problem for incumbents is that Amazon does not need to win pricing on day one. Amazon already runs the network for its own demand; the marginal cost of selling unused capacity is close to zero. Traditional carriers, by contrast, must charge enough to cover their full fixed-cost stack on every shipment. That asymmetry, compounded over enough quarters, looks like the same dynamic that played out in cloud computing between 2008 and 2014.

The day-2 rebound — and what it tells us

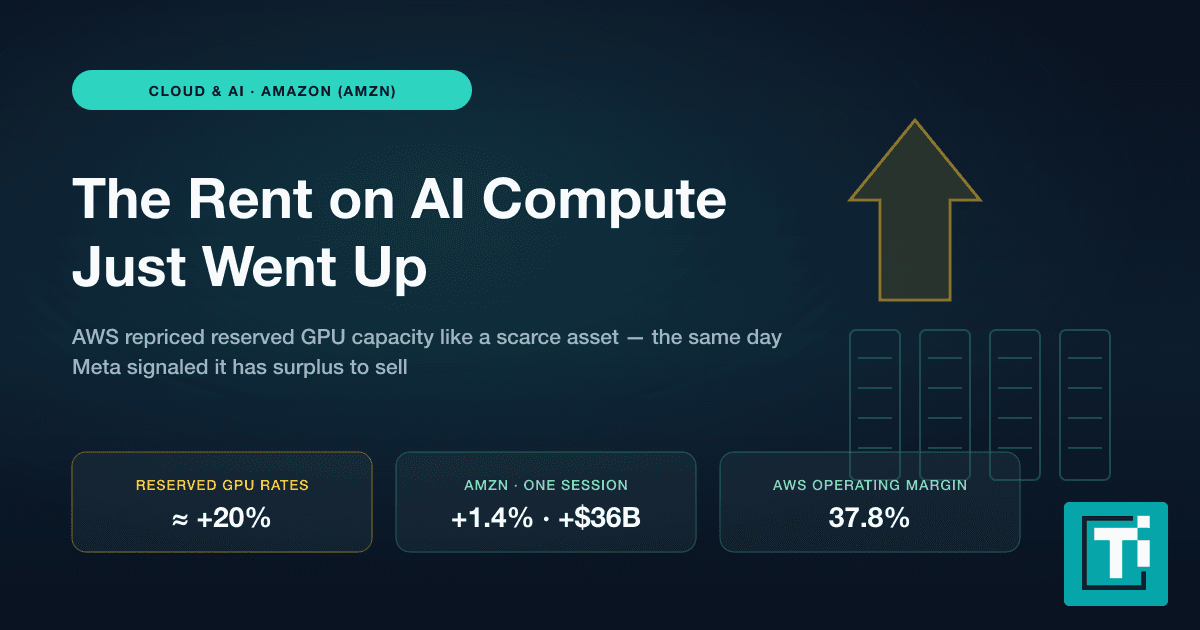

Twenty-four hours after the announcement, the carrier complex is bouncing: FDX +1.4%, UPS +1.8%, GXO +7.7%, FWRD +5.0%, ODFL +2.0% intraday. That is not vindication; it is a buy-the-dip reflex from value investors and a short-cover from systematic strategies that triggered into yesterday's collapse. The structural thesis has not changed, and the rebound does nothing to alter the multi-year math: Amazon's marginal-cost advantage compounds quarter after quarter, while the legacy carriers compete from a fixed-cost base. Watch the next earnings prints from FedEx and UPS — guidance is the variable the market will reprice on, not a one-day bounce.

The legacy carriers' three options

Each carrier now has to choose between three uncomfortable strategies: (1) compete on price and watch margins compress, (2) specialize in segments Amazon does not want — heavy industrial freight, regulated chemicals, time-critical medical — and accept a lower TAM, or (3) consolidate. Expect M&A conversations to accelerate in the second half of 2026.

Winners Take Most: The AGI Compounding Thesis

AMZN has run more than 200% since the ChatGPT moment in November 2022 — not because Amazon is an AI company, but because the AI compute platform shift validates the thesis that scale, capital, and proprietary data compound into permanent advantage. Microsoft, Apple, NVIDIA, Alphabet, Meta, and Amazon together now represent more than 30% of S&P 500 market cap. That concentration is not an accident; it is the visible output of a market structure where AGI accelerates the gap between large and small.

The Amazon Supply Chain Services launch is a textbook example. AGI lowers Amazon's marginal cost of (a) routing every package optimally, (b) onboarding new merchants without human reps, (c) pricing capacity dynamically against demand, and (d) preventing fraud and shrinkage at scale. Each of those capabilities was technically possible five years ago but operationally impractical. They are now operational. Our deeper look at Amazon's AI growth flywheel explores how the same dynamic works inside AWS and Project Kuiper.

What Investors Should Watch Next

Onboarding velocity

How fast Amazon Supply Chain Services signs up external merchants in Q3 and Q4 2026 is the single best leading indicator. The AWS comparison is instructive: AWS hit a $1B run-rate within four years of opening to external customers. If Supply Chain Services tracks even half that adoption curve, the upside is material.

Pricing strategy

The most aggressive scenario — Amazon undercuts FedEx and UPS by 15–25% on small-parcel — would compress carrier margins immediately and accelerate consolidation. A more measured rollout (Amazon prices in line with incumbents and competes on reliability) would extend the runway for FedEx and UPS by 12–18 months. Watch the first published rate sheet.

Antitrust posture

A vertically integrated retailer running the dominant fulfillment stack for its own competitors is exactly the structure regulators have flagged in past cases. Expect FTC and EU Competition Commission interest within the next 90 days. The base case is that Amazon ringfences Supply Chain Services as a separately-priced subsidiary — same playbook as AWS — but the legal scrutiny is real.

AWS-style margin trajectory

If Supply Chain Services follows the AWS template, gross margins should ramp from negative-or-breakeven in year one to 25–30% within three years. That alone would add $30–50B in annual operating income at maturity. Cramer flagged the same margin pathway in his recent Amazon coverage.

For deeper analysis on the AI-era market structure and the "Winners Take Most" thesis, Bloomberg has the full announcement breakdown, Reuters tracked the carrier sell-off intraday, and the SEC EDGAR portal will carry any 8-K filings related to the launch.

FAQ

Frequently asked questions

What is Amazon Supply Chain Services?

Amazon Supply Chain Services is a new offering that opens Amazon's entire logistics network — freight, distribution, fulfillment, and parcel shipping — to every business, regardless of whether they sell on the Amazon platform. It bundles capabilities previously available only through separate Amazon programs (FBA, Amazon Freight, Multi-Channel Fulfillment, Amazon Shipping) into a single integrated stack.

Why did FedEx and UPS stocks fall so much?

Investors immediately understood that every major U.S. carrier now competes directly against Amazon's full vertical stack. FedEx fell as much as 7.4% (its worst day in over a year) and UPS dropped 8.9%. Amazon's marginal cost of selling unused capacity is near zero, while traditional carriers must cover their full fixed-cost stack on every shipment — a structural disadvantage that compounds over time.

How much has AMZN stock gained since the ChatGPT moment in November 2022?

AMZN has gained more than 200% since November 2022, when ChatGPT launched and triggered the AI capital cycle. The stock hit a fresh 52-week intraday high of $278.56 on the Supply Chain Services announcement.

Will this trigger antitrust scrutiny?

Almost certainly. A vertically integrated retailer running the dominant fulfillment stack for its own competitors is exactly the structure that has drawn regulatory attention in past cases. Expect FTC and EU Competition Commission interest within 90 days. The base case is that Amazon ringfences Supply Chain Services as a separately-priced subsidiary, similar to AWS.

What is the "Winners Take Most" thesis?

The thesis is that scale, capital, and proprietary data compound into permanent competitive advantage — and that AGI dramatically accelerates this dynamic. Six mega-cap technology companies now represent more than 30% of S&P 500 market cap, and the gap between large and small is widening, not narrowing. Amazon Supply Chain Services is a textbook example of a dominant platform extending into an adjacent market with structurally lower marginal costs.

Should I buy AMZN stock now?

This article does not make buy or sell recommendations. AMZN trades at approximately 38× forward earnings — a premium to retail peers but in line with the AI-infrastructure cohort. Investors should evaluate whether they believe Supply Chain Services can follow the AWS margin trajectory and whether the antitrust risk is appropriately priced. Always consult a licensed financial advisor before investing.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Fatimah Misbah Hussain is a seasoned financial journalist at TECHi, specializing in stock market analysis, commodities, and tech sector finance. With a strong background in monitoring public markets and tech companies, she breaks down complex stock movements and commodity price trends into actionable insights.