- The cash squeezeAlphabet spent $35.7B on capex in Q1 2026 and generated $10.1B of free cash flow after capex.

- The valuation checkUsing official TTM FCF, Alphabet is closer to 75x free cash flow; using annualized Q1 FCF, the multiple is roughly 119x.

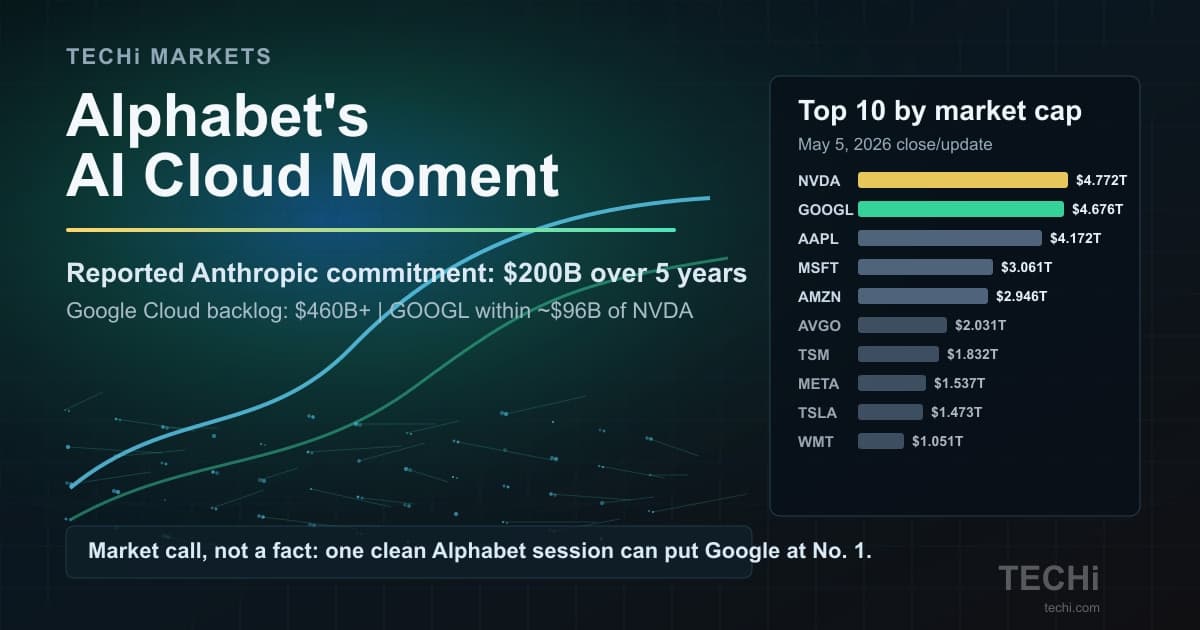

- The bull caseGoogle Cloud reached $20.0B of Q1 revenue and management cited about $462B of Cloud backlog.

- The investor moveTreat the stock as high-quality but execution-sensitive: watch Cloud backlog conversion, Search ad monetization, and 2027 capex intensity.

Alphabet's AI story has moved past model demos. The question now is capital allocation: can Google earn enough from Search, Cloud and enterprise AI to justify an infrastructure bill that is growing faster than the cash flow investors usually use to value the company?

Last updated: May 7, 2026 at 10:06 a.m. ET. U.S. markets are open. This analysis uses Alphabet's latest Q1 2026 filings, its 2025 annual report, and live May 7 market context from GOOGL market data and TECHi's Alphabet quote page.

The number bears are using against Google

The bear case starts with one uncomfortable line from Alphabet's cash-flow statement. In Q1 2026, Alphabet generated $45.8 billion of operating cash flow, spent $35.7 billion on property and equipment, and produced only $10.1 billion of free cash flow, according to the company's Q1 2026 earnings release. That means capex absorbed roughly 78% of operating cash flow in the quarter.

The trailing-twelve-month picture is less dramatic but still heavy. The same Alphabet release shows $174.4 billion of operating cash flow, $109.9 billion of property-and-equipment spending, and $64.4 billion of free cash flow over the trailing twelve months. That puts trailing capex at about 63% of operating cash flow, which is why the “AI capex is eating free cash flow” argument is not just a slogan.

The valuation version of that argument needs more care. StockAnalysis showed Alphabet at roughly $4.8 trillion of market value on May 7, 2026; divide that by Alphabet's official $64.4 billion of trailing free cash flow and the stock is closer to 75 times trailing free cash flow, not 133 times. The 133x-style soundbite only works if investors annualize the depressed Q1 free cash flow run-rate and use a harsher market-cap snapshot. On that tougher method, Alphabet is still near 119 times annualized Q1 free cash flow. Either way, the stock is priced for clean execution.

Why the capex comparison looks so extreme

The spending looks especially large next to Google Cloud. Alphabet's 2025 annual report shows Google Cloud revenue of $58.7 billion in 2025, while management's Q1 call lifted full-year 2026 capex guidance to $180 billion to $190 billion. That is roughly 3.1 to 3.2 times the entire 2025 Google Cloud revenue base.

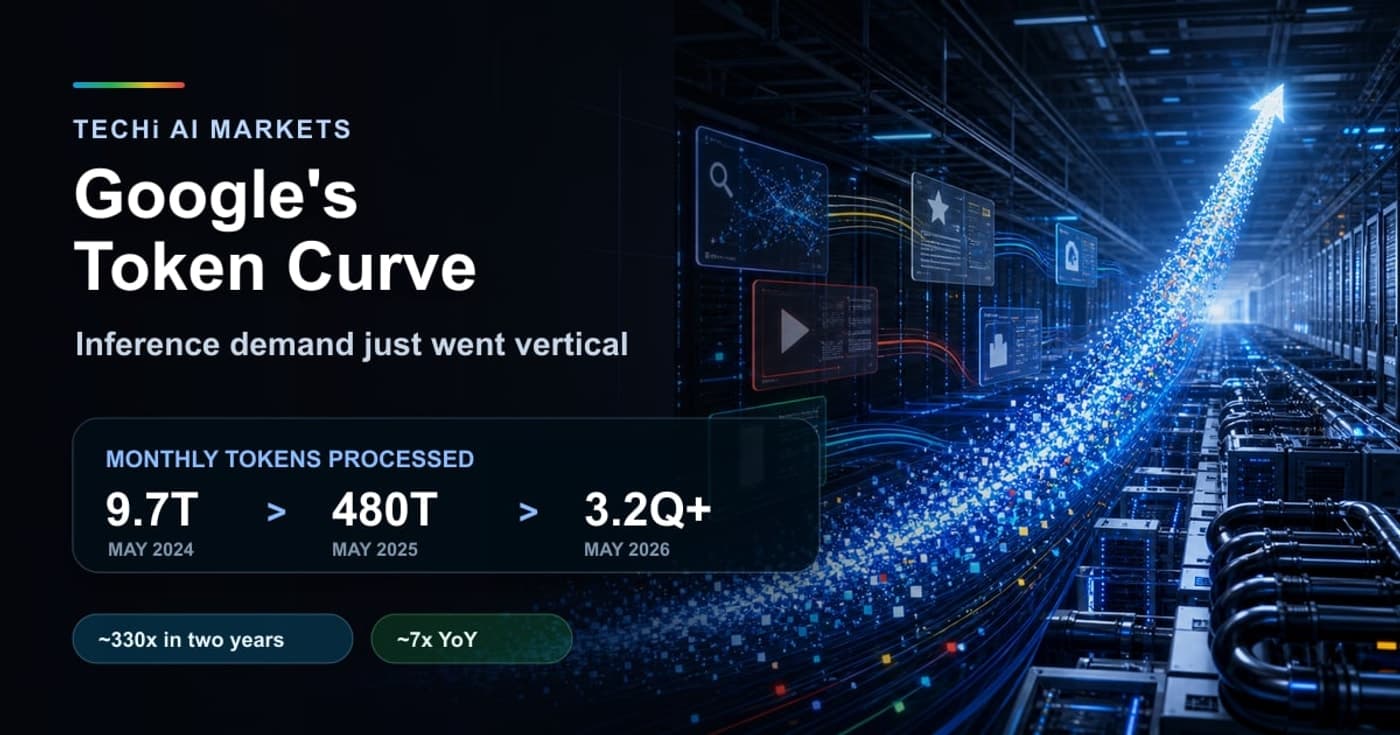

Even against the faster 2026 run-rate, the number is still huge. Alphabet reported Google Cloud revenue of $20.0 billion in Q1 2026, which annualizes to just over $80 billion before seasonality or growth. A $180 billion to $190 billion capex plan is still about 2.2 to 2.4 times that run-rate. This is why investors are not debating whether Google has AI demand; they are debating whether the return on that demand will arrive fast enough.

The strongest version of the bear case is broader than Alphabet. GQG Partners has argued in its “Dotcom Bubble on Steroids” AI series that today's AI capital cycle can produce weak economic returns even if AI itself proves transformative. That matters for Google because the company is no longer just selling ads against queries; it is funding a global compute buildout where chips, data centers, power and depreciation all hit the financial model.

The countercase: Google is not spending into a vacuum

The counterargument is that Alphabet's free-cash-flow drop is mainly a growth-spending problem, not an operating collapse. The company still generated $174.4 billion of operating cash flow over the trailing twelve months, according to its Q1 2026 release, and the Cloud business is finally acting like a second engine instead of a margin drag.

Google Cloud's acceleration is the most important defense. Alphabet said Cloud revenue rose 63% to $20.0 billion in Q1 2026, and management told investors on the Q1 call that Cloud backlog reached about $462 billion. That backlog does not guarantee a perfect return on capex, but it is a much stronger demand signal than a vague “AI future” pitch.

There is also a strategic reason Google may be more comfortable spending than some peers. Alphabet's 2025 annual report says the company's AI infrastructure supports both its own products, including Search and YouTube, and services for Google Cloud customers, while also using both GPUs and its custom TPUs. TECHi's earlier coverage of Google's TPU push against Nvidia explains why that vertical stack matters: Google is not only renting compute; it is trying to control more of the cost curve.

Search is the harder risk to model

The capex math is visible. The Search risk is messier. Pew Research found that Google users who saw an AI summary clicked a traditional search result in 8% of visits versus 15% when no AI summary appeared, and users clicked a link inside the AI summary in only 1% of visits. For publishers, that is a traffic problem. For Google, it is a monetization test.

Google's answer is to put ads closer to the AI answer layer. In 2025, Google said Search and Shopping ads in AI Overviews were expanding to desktop in the U.S. and that it was testing ads in AI Mode; the same post said AI Overviews were driving more than 10% higher usage for query types where they appeared in the U.S. and India. That does not eliminate cannibalization risk. It shows Google is already trying to move the ad unit with the user behavior.

This is the key distinction for investors. If AI Overviews reduce publisher clicks but keep users inside Google, Alphabet can still defend the ad business. If AI answers reduce commercial intent, ad density or pricing, then Search margin could compress at the same time that depreciation from AI infrastructure rises. That is the real bear case, and it is more serious than a single FCF multiple.

What investors should do next

Existing holders do not need to panic because capex is high. They need to watch whether the spending produces measurable output. The first metric is Cloud backlog conversion: management said just over half of the roughly $462 billion backlog should convert to revenue over the next 24 months, according to the Q1 call transcript. If that timing slips, the capex story weakens.

The second metric is capex intensity. Alphabet's $180 billion to $190 billion 2026 guide is now the baseline, not the shock. Investors should watch whether 2027 guidance keeps climbing faster than Cloud revenue, Search revenue and operating cash flow. TECHi's Google stock analysis hub is the right internal reference page for tracking the stock against those fundamentals.

The third metric is Search monetization. Pew's click data shows the risk side, while Google's ads-in-AI-Overviews plan shows the defense. The question for investors is whether AI search expands total commercial queries enough to offset lower outbound clicks. That answer will show up in Google advertising growth, traffic acquisition cost pressure and operating margin, not in product demo language.

For new money, the bar is higher. A company trading near 75 times trailing free cash flow, or around 119 times annualized Q1 free cash flow, does not offer much room for a messy capex cycle. Alphabet can still be a great business and a demanding stock at the same time. That is the tension.

The bottom line

Google can justify this AI infrastructure spending only if three things happen together: Cloud backlog turns into high-margin revenue, Search ads survive the move from links to answers, and capex growth stops outrunning operating cash flow. The company has the assets to pull that off. The valuation leaves little room for delays.

The best stance is cautious patience. Long-term holders can keep owning Alphabet if they believe Cloud and Search will compound through AI. New buyers should demand a cleaner entry or stronger proof that the $180 billion-plus infrastructure wave is turning into cash, not just capacity. Investors comparing Alphabet with other AI infrastructure beneficiaries can start with TECHi's coverage of AI data-center suppliers and the broader AI stocks list.

This article is for information only and is not investment advice. Investors should consider their own risk tolerance, time horizon and financial situation before buying or selling Alphabet shares.

FAQ

Frequently asked questions

Is Alphabet really spending $180 billion to $190 billion on capex in 2026?

Yes. Alphabet management raised 2026 capex guidance to $180 billion to $190 billion on the Q1 2026 earnings call, citing unprecedented internal and external demand for AI compute resources.

Is Google stock trading at 133 times free cash flow?

Not on Alphabet's official trailing-twelve-month free cash flow. Using roughly $4.8 trillion of May 7, 2026 market value and $64.4 billion of trailing FCF, the multiple is closer to 75x. Using annualized Q1 FCF creates a much harsher number near 119x.

Could AI Overviews hurt Google Search revenue?

Yes, it is a real risk because Pew Research found lower click-through rates when AI summaries appear. Google is countering by placing and testing ads inside AI Overviews and AI Mode, so the key question is whether AI search preserves commercial intent.

What should investors watch before buying Alphabet?

Watch Cloud backlog conversion, 2027 capex guidance, Google advertising growth, and whether free cash flow starts recovering after the 2026 infrastructure buildout.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Fatimah Misbah Hussain is a seasoned financial journalist at TECHi, specializing in stock market analysis, commodities, and tech sector finance. With a strong background in monitoring public markets and tech companies, she breaks down complex stock movements and commodity price trends into actionable insights.