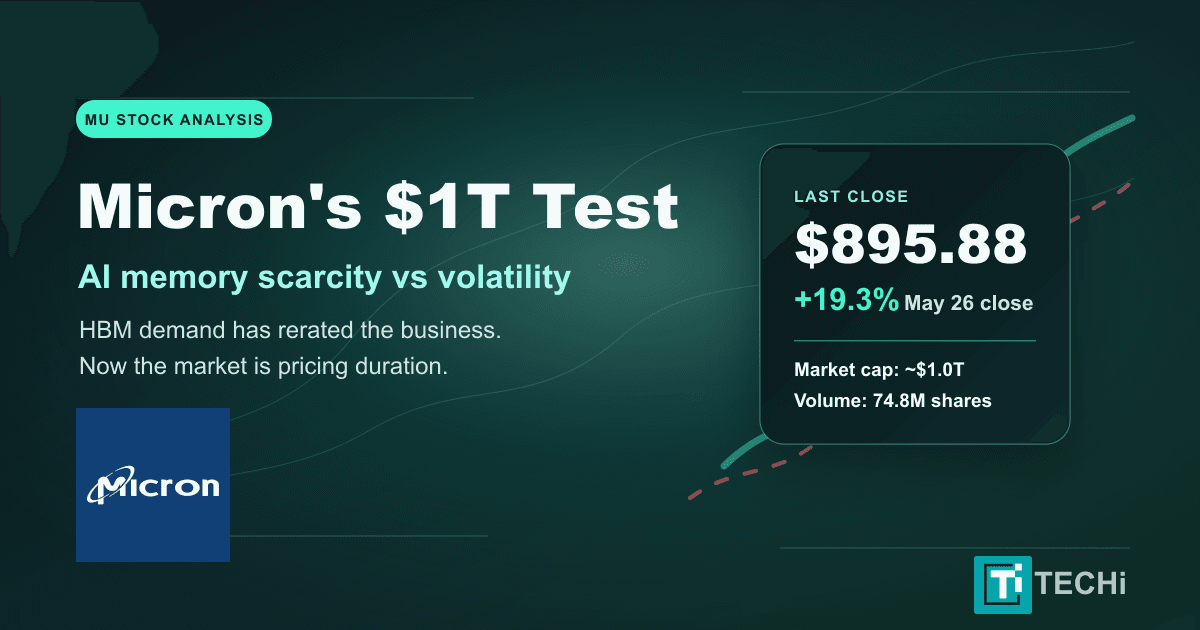

Micron Technology did not merely have a good Tuesday. It became the market’s cleanest one-stock expression of a memory shortage that AI infrastructure can no longer hide. Finviz showed MU closing at $640.20 on Tuesday, May 5, 2026, up $63.75, or 11.06%, while MarketBeat showed the stock up 69.45% over the past month. That is the setup investors have to judge now: the business momentum is real, but the stock has already pulled forward a lot of future good news.

- The moveMU closed at $640.20 on May 5, up 11.06% on the day, and MarketBeat showed a 69.45% one-month gain. Sources: Finviz, StockInvest.us and MarketBeat.

- The driverMicron’s fiscal Q2 revenue nearly tripled year over year to $23.86B, with non-GAAP EPS of $12.20 and adjusted free cash flow of $6.9B. Source: Micron Q2 FY2026 release.

- The AI memory squeezeMicron expects DRAM and NAND supply-demand conditions to remain tight beyond calendar 2026. Source: Micron Q2 FY2026 prepared remarks.

- The fresh catalystMicron announced shipping of its 245TB 6600 ION data-center SSD on May 5, positioning it for AI data lakes, cloud and hyperscale workloads. Source: Micron product release.

- The answerBe bullish on the business, cautious on the entry. Existing holders can use rules and sizing; new buyers should avoid chasing a full position after a near-70% monthly move.

The Rally Is Not Random

Micron’s latest reported quarter explains why the market suddenly cares. The official fiscal Q2 2026 earnings release showed revenue of $23.86 billion versus $13.64 billion in the prior quarter and $8.05 billion a year earlier. GAAP net income was $13.79 billion, GAAP diluted EPS was $12.07, non-GAAP diluted EPS was $12.20 and adjusted free cash flow was $6.9 billion. Those figures do not look like a normal commodity-memory rebound. They look like a shortage with pricing power.

The business-unit mix is just as important. In Micron’s prepared remarks, DRAM revenue was $18.8 billion, up 207% year over year, while NAND revenue was $5.0 billion, up 169% year over year. Cloud Memory Business Unit revenue was a record $7.7 billion, Core Data Center revenue was a record $5.7 billion, and Mobile and Client revenue was a record $7.7 billion. The stock is not rising because investors forgot Micron is cyclical. It is rising because this cycle is being fed by AI data-center demand, power constraints and multi-year customer planning.

Why Tuesday’s 11% Pop Happened

The immediate May 5 spark was a mix of product news, analyst enthusiasm and momentum. Micron announced that its 245TB 6600 ION SSD is now shipping, calling it the world’s highest-capacity commercially available SSD and saying it is designed for AI, cloud, enterprise and hyperscale workloads. Micron said the 245TB E3.L drive requires 82% fewer racks than HDD-based deployments for equivalent raw storage capacity, and that its lab testing showed up to 84 times better energy efficiency for AI workloads versus HDD-based systems.

The Motley Fool framed the product as a direct AI data-center catalyst, while Investing.com tied the move to Street-high analyst targets, severe supply constraints, and memory costs becoming a larger budget issue for major technology buyers. Finviz’s analyst table showed DA Davidson initiating coverage at Buy with a $1,000 target, and Investing.com reported Melius Research initiating at Buy with a $700 target and TD Cowen lifting its target to $660 from $550.

That does not make the stock automatically cheap at any price. MarketBeat’s analyst tracker showed 39 analyst ratings with a Buy consensus, but its average 12-month price target was $478.24, implying downside from the roughly $640 share price it displayed. That disagreement is the article. Bulls see a memory company being re-rated into an AI infrastructure bottleneck. Skeptics see the classic late-cycle trap: the stock looks optically cheap on peak earnings just as expectations get stretched.

The Bull Case: Micron Is No Longer Just “A Memory Stock”

The strongest bull argument starts with Micron’s own supply commentary. In its Q2 prepared remarks, Micron said it expects DRAM and NAND industry bit demand in calendar 2026 to be constrained by supply and that supply-demand conditions should remain tight beyond calendar 2026. Management also guided fiscal Q3 revenue to $33.5 billion, plus or minus $750 million, non-GAAP gross margin to roughly 81%, and non-GAAP EPS to $19.15, plus or minus $0.40.

That is why bullish coverage has become aggressive. Seeking Alpha’s bullish HBM analysis argued that sold-out 2026 HBM production and binding customer commitments change the visibility profile of the business. TIKR highlighted Micron’s revenue growth from $6.8 billion in fiscal Q3 2024 to $23.9 billion in fiscal Q2 2026 and emphasized HBM as the key AI-memory driver. PC Gamer and TechRadar both focused on management’s shortage language, including demand running materially above available supply.

The forward multiple is the other bull talking point. Finviz showed a trailing P/E of 30.22 and a forward P/E of 6.68 on May 5. If Micron really earns close to what aggressive 2026 estimates imply, the stock is not expensive on a simple earnings multiple. But that “if” carries almost all of the risk.

The Bear Case: This Is Still A Cycle, And The Stock Is Hot

The caution case is not that Micron’s numbers are fake. They are excellent. The caution case is that memory stocks often look cheapest near peak earnings. The Motley Fool’s April rally analysis made that point directly: memory chip stocks are historically cyclical, and the worst entry can come when earnings are roaring. FX Leaders also warned that a nearly 70% move in recent weeks leaves less room for disappointment, especially with heavy capex and geopolitical uncertainty in the background.

The technical setup backs that up. Finviz showed RSI at 81.74, while StockInvest.us called the stock high risk because it moved $46.27 between its day low and day high on May 5 and showed extreme overbought conditions on RSI14. Momentum can stay extreme longer than cautious investors expect, but it is still momentum. Buying after an 11% day and a nearly 70% month is not the same risk as buying before the breakout.

There is also capex risk. Micron’s fiscal Q2 2026 10-Q said the company estimates 2026 property, plant and equipment capital expenditures, net of government incentives, above $25 billion. The same filing warns that investments in capital expenditures may not generate expected returns or cash flows, and that export controls, tariffs and trade regulation can affect global operations. Those are not abstract risks when a company is building capacity into a shortage.

What Should Investors Do Next?

For existing shareholders, the cleanest answer is discipline, not panic. The business case improved materially, and selling only because a stock went up can be as lazy as buying only because it went up. But if MU has grown from a 5% position to a 12% or 15% position in one month, trimming back to a planned allocation is risk management, not a bearish call.

For new buyers, caution is the better default. Micron may still be cheap if the current memory shortage persists through 2027 and HBM demand keeps pricing tight. The problem is that a new buyer today is no longer paying for uncertainty. They are paying after the market has seen the shortage, repriced the earnings power and started to circulate $700 and $1,000 targets. That does not mean “do nothing forever.” It means do not confuse a great company setup with a great entry price.

A practical approach is to split the decision into three triggers. First, watch the next earnings setup, which MarketBeat lists around late June 2026 on its MU chart page. Second, watch whether fiscal Q3 guidance at $33.5 billion and roughly 81% non-GAAP gross margin survives real-world pricing, mix and supply constraints. Third, watch the stock’s reaction to good news. If Micron keeps rising on strong volume after consolidating, the market is still accumulating. If the stock sells off on good news, expectations have probably run ahead of the fundamentals.

What The Top Coverage Gets Right, And What It Misses

The bullish articles are right that Micron is not the sleepy commodity-memory trade investors knew a decade ago. HBM, AI data lakes, high-capacity SSDs and strategic supply agreements give the company more visibility than a standard DRAM upcycle. The cautious articles are right that memory supply eventually responds to profit signals, and Micron is already spending heavily to add capacity. The mistake is choosing only one side.

The best answer sits in the middle: Micron deserves a higher-quality multiple than it used to, but investors should not pretend cyclicality disappeared. Use AMD vs Nvidia Stock: Which AI Chip Maker Deserves Your Money? for the live quote context and Micron Sparks Wild HBM Boom Surge to compare the move against the rest of the AI hardware trade. MU can keep working, but the easy money was made before the stock became the most obvious AI-memory winner on the screen.

Bottom Line

Micron’s stock-price explosion is fundamentally justified and tactically dangerous at the same time. The business is benefiting from real AI-driven demand, tight DRAM and NAND supply, record margins, record cash generation and a product roadmap that now touches HBM, SSDs and data-center memory bottlenecks. Those facts support the long-term bull case.

But the stock has already surged 11% in a day and roughly 70% in a month. That makes the next decision less about believing in Micron and more about respecting price. Existing holders should stay rules-based. New buyers should be patient or build slowly. Traders should protect gains. The right stance after a move this violent is not bearish. It is bullish with guardrails.

FAQ

Frequently asked questions

Why did Micron stock jump 11% on May 5, 2026?

Micron stock jumped after a combination of AI-memory momentum, analyst target increases, and Micron’s May 5 announcement that its 245TB 6600 ION data-center SSD is now shipping. Finviz and StockInvest.us showed MU closing at $640.20, up 11.06%.

How much is Micron stock up over the past month?

MarketBeat showed Micron stock up 69.45% over the past month as of its May 6, 2026 chart page.

Is Micron stock still cheap after the rally?

Micron can look cheap on forward earnings if fiscal 2026 estimates hold, but that multiple depends on peak-cycle margins, tight memory supply and continued AI demand. Investors should treat the valuation as scenario-dependent.

What should existing Micron shareholders do now?

Existing shareholders can hold if the thesis remains intact, but should rebalance if the position has grown beyond their planned allocation after the stock’s rapid move.

Should new investors buy MU after a 70% monthly rally?

This article does not make buy or sell recommendations. A cautious approach for new investors is staged entry or waiting for a pullback or fresh earnings confirmation rather than chasing a full position after the move.

What are the main risks for Micron stock?

The main risks are memory-cycle normalization, heavy capital spending, execution risk on new capacity, geopolitical and trade restrictions, and investor expectations already pricing in strong AI-memory demand.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Nouman S. Ghumman covers tech regulation, antitrust, and data-privacy policy for TECHi. He tracks DOJ and FTC enforcement actions, European Digital Markets Act compliance filings, and the state-level privacy laws filling the federal gap. His coverage reads court dockets and regulatory notices rather than reaction-cycle commentary, and connects policy moves to concrete impacts on Big Tech valuations and market structure.