Broadcom stock is no longer a simple semiconductor momentum trade. The latest story is that AVGO has become the public-market proxy for custom AI silicon: Google TPUs, Anthropic compute capacity, Meta MTIA chips, Ethernet networking and VMware cash flow, all moving into the June 3, 2026 Q2 earnings test. For the evergreen valuation hub, use our Broadcom Stock (AVGO): Complete Investment Analysis, AI Chip Dominance & Price Forecast 2026.

- The newest catalystBroadcom will report Q2 FY2026 after the close on Wednesday, June 3, 2026, with management hosting the call at 5:00 p.m. ET.

- The earnings setupQ1 revenue was $19.311B, up 29% YoY; AI revenue was $8.4B, up 106%; and Q2 revenue guidance is about $22.0B.

- The latest AI storyBroadcom now has fresh public agreements tied to Google TPUs, Anthropic next-generation TPU capacity, and Meta custom MTIA silicon.

- The investor tensionThe growth story is exceptional, but valuation, customer concentration, debt and AI supply execution leave no room for sloppy Q2 commentary.

- The TECHi viewExisting holders can justify staying long if position size is controlled; new buyers should avoid chasing every AI headline and demand June 3 confirmation.

The Latest Story: Broadcom Has Become the Custom AI Silicon Trade

The most important Broadcom stock update is not one single headline. It is the sequence. On March 4, Broadcom reported a record Q1 and guided Q2 revenue to about $22.0 billion. On April 6, the company filed an 8-K describing a long-term Google TPU and AI-rack supply agreement through up to 2031, plus an expanded Anthropic collaboration for about 3.5 gigawatts of next-generation TPU-based AI compute beginning in 2027. On April 14, Broadcom and Meta announced an expanded MTIA partnership with an initial commitment above 1 gigawatt and a multi-gigawatt roadmap. On May 4, Broadcom set June 3 as the next earnings date.

That is why the Broadcom story is bigger than "AI chip demand is strong." The company is no longer just selling merchant chips into a hot cycle. It is embedding itself into the custom silicon roadmaps of the largest AI infrastructure buyers in the world. For readers comparing AI chip exposure, our Broadcom vs Nvidia AI chip race and Nvidia Stock (NVDA): $1T Order Backlog, Vera Rubin & Forecast 2026 pages explain why Broadcom and Nvidia can both win while serving different parts of the AI stack.

Why AVGO Stock Reacted So Strongly

Broadcom has two traits investors usually do not get in the same AI stock. First, it has fast-growing AI semiconductor revenue. Second, it has a cash-generating infrastructure software business built around VMware. In Q1 FY2026, semiconductor solutions revenue was $12.515 billion, up 52% year over year, while infrastructure software revenue was $6.796 billion, up 1% year over year. That mix matters because AI gives Broadcom growth, while software gives the company margin and cash-flow ballast.

Reuters reported that Hock Tan told analysts Broadcom had line of sight to more than $100 billion in 2027 AI chip revenue, and that Broadcom expected Q2 AI chip revenue of $10.7 billion. That number is not a guarantee, and it depends on customer ramps, supply, timing and execution. But it explains why the stock is being valued as a strategic AI infrastructure company rather than as a conventional semiconductor supplier.

Google And Anthropic Changed The 2027 Visibility

The April 6 filing is the cleanest source for the newest long-term AI story. Broadcom said it entered into a long-term agreement to develop and supply custom TPUs for future Google TPU generations and a supply assurance agreement to provide networking and other components for Google next-generation AI racks through up to 2031. The filing also said Anthropic will access through Broadcom approximately 3.5 gigawatts of next-generation TPU-based compute capacity beginning in 2027, as part of Anthropic multiple-gigawatt commitment.

Fact check: Broadcom April 6, 2026 Form 8-K is the primary source for the Google through-2031 language and the Anthropic 3.5GW capacity figure.

Anthropic confirmed the same strategic direction from the customer side. It said the new agreement with Google and Broadcom covers multiple gigawatts of next-generation TPU capacity expected to come online starting in 2027. Anthropic also said its run-rate revenue had surpassed $30 billion, up from about $9 billion at the end of 2025, and that more than 1,000 business customers were each spending over $1 million on an annualized basis.

Fact check: Anthropic April 6 announcement verifies the multiple-gigawatt TPU capacity language, expected 2027 timing, revenue run-rate figure and customer-count figure.

Meta Added A Second April Catalyst

The Meta update matters because it broadens the custom-silicon narrative beyond Google and Anthropic. Broadcom and Meta said on April 14 that they are expanding a multi-year, multi-generation partnership around Meta Training and Inference Accelerator chips. Broadcom said the initial commitment exceeds 1 gigawatt and is the first phase of a sustained, multi-gigawatt rollout. Meta said Broadcom will work across chip design, advanced packaging and networking, built around Broadcom XPU platform.

Fact check: Broadcom April 14 release and Meta Newsroom independently verify the MTIA partnership, the >1GW initial commitment and the chip design/packaging/networking scope.

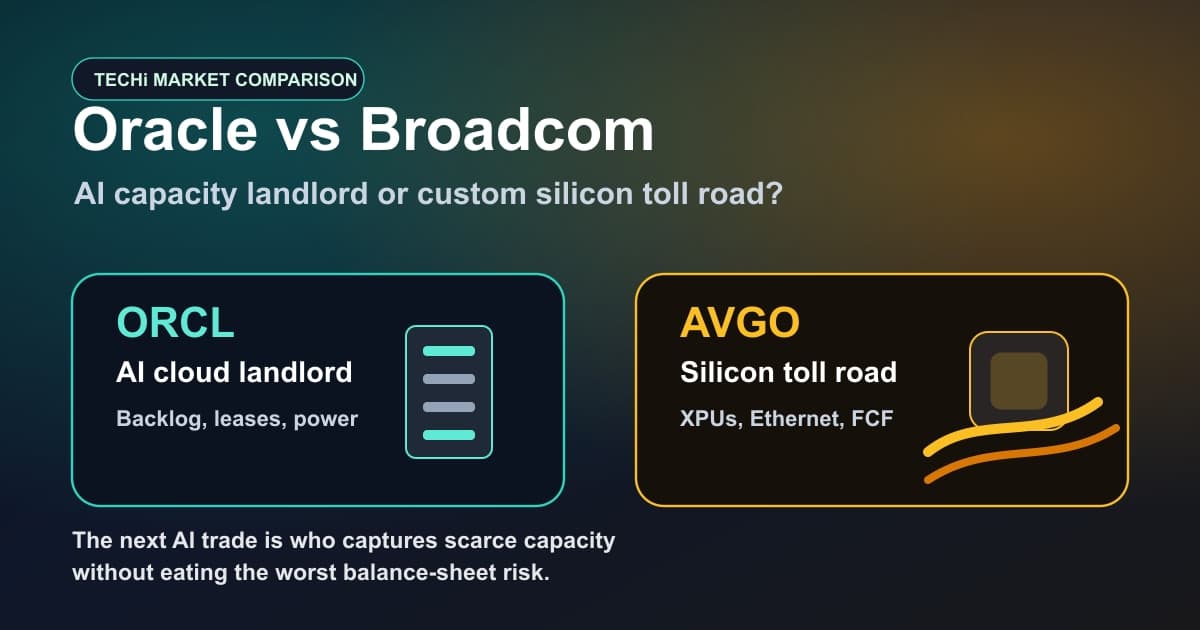

This is strategically important because Meta, Google, Anthropic and OpenAI do not all want the same compute stack. Some workloads will stay on Nvidia GPUs. Some will use AMD alternatives. Some will use internally designed accelerators built with partners. Broadcom wins when hyperscalers decide that a custom accelerator plus high-speed Ethernet fabric can lower cost, improve efficiency or reduce dependency on one supplier. Our AMD Stock (AMD): Complete Investment Analysis & Forecast 2026 and AI Capex Is Now 75% of U.S. GDP Growth: Why Big Tech's Spending Boom Cannot Be Stopped coverage lays out the broader AI infrastructure spending cycle behind that shift.

Valuation: Broadcom Is Strong, But Not Invisible To Price

The market has already repriced Broadcom. MarketBeat recently showed AVGO around $427, a P/E ratio above 80, a Moderate Buy consensus rating and a consensus price target near $435. That does not mean the stock is overvalued. It does mean the easy part of the re-rating has likely happened. From here, the stock needs earnings quality, not just another AI headline.

Fact check: MarketBeat company table listed AVGO around $427, P/E near 83, Moderate Buy and a $435.30 consensus target; TECHi AVGO quote page tracks the live stock hub.

The good news is that Broadcom is not a pre-revenue AI story. In Q1, the company generated $8.260 billion of cash from operations and $8.010 billion of free cash flow. It also returned $10.9 billion to shareholders through dividends and repurchases in the quarter, and announced a new $10 billion buyback authorization through December 31, 2026.

Fact check: Broadcom Q1 release verifies operating cash flow, free cash flow, capital returns and the new buyback authorization.

The Risks Investors Cannot Ignore

The biggest risk is customer concentration. Broadcom said in its Q1 10-Q that direct sales to one semiconductor solutions customer, a distributor, accounted for 42% of net revenue in Q1 FY2026, and that aggregate sales to its top five end customers accounted for about 50% of net revenue. That concentration can help revenue visibility when the largest customers are ramping. It can hurt quickly if one deployment slips.

Fact check: Broadcom Q1 FY2026 Form 10-Q discloses the 42% direct-customer concentration and approximately 50% top-five end-customer exposure.

The second risk is balance-sheet and interest-rate sensitivity. Broadcom had $67.970 billion of future scheduled principal debt payments as of February 1, 2026 and said a 50-basis-point market-rate move would change the fair value of its borrowings by about $2.0 billion. The company also said it was in compliance with debt covenants. That is not a crisis signal, but it means investors should keep debt service in the model.

Fact check: Broadcom 10-Q debt footnote and market-risk section verify the debt principal schedule, covenant compliance and interest-rate sensitivity.

The third risk is expectation risk. BofA reiterated a Buy rating and $450 target after the Google and Anthropic deals, while Investing.com also noted more cautious ratings elsewhere, including D.A. Davidson Neutral at $375. When a stock becomes a consensus AI winner, even good news can be sold if it arrives below the market story.

Fact check: Investing.com analyst-ratings coverage verifies the BofA Buy/$450 reference and the more cautious D.A. Davidson $375 target cited in the same market wrap.

What Should Investors Do Next?

If You Already Own AVGO

The cleanest move is to stay disciplined rather than automatically sell strength. Broadcom has real revenue, real cash flow, real customer disclosures and a near-term Q2 catalyst. But if AVGO has become too large a position after the rally, trim position size back to a risk level you can hold through a volatile June 3 print.

Fact check: Q1 cash-flow and guidance data support the fundamental case; the position-size recommendation is TECHi investment-risk analysis, not a source claim.

If You Want To Buy AVGO Now

Do not buy solely because the latest AI customer headline sounds large. The better approach is to decide what evidence you need from June 3: Q2 revenue at or above the $22.0 billion guide, AI semiconductor revenue near or above the $10.7 billion expectation, clean adjusted EBITDA quality around the 68% guide, and specific customer-ramp language for 2027.

Fact check: Broadcom Q1 release is the source for the $22.0B Q2 revenue guide, $10.7B expected Q2 AI semiconductor revenue and 68% adjusted EBITDA guide.

If You Are Trading The Earnings Catalyst

The obvious setup is a June 3 catalyst trade. The harder question is whether expectations are too high. AVGO can beat numbers and still trade sideways if management does not expand the 2027 visibility story. Traders should separate the company from the stock: Broadcom can remain an excellent company while the share price pauses after a strong run.

Fact check: Broadcom Q2 date notice verifies the June 3 catalyst; the trading framework is TECHi analysis.

Bottom Line

Broadcom stock deserves its place near the center of the AI infrastructure trade. The company has the verified Q1 numbers, the Q2 guide, the Google/Anthropic filing, the Meta expansion, the VMware cash engine and the shareholder-return profile that most AI infrastructure names cannot match. That is the bull case.

Fact check: Broadcom Q1 release, April 6 8-K, Broadcom-Meta release and Q1 10-Q support the claims in this paragraph.

The caution is equally clear. At roughly the mid-$400 consensus target area and with the stock already pricing in major AI wins, investors should not treat AVGO as risk-free. The next good decision is not "buy everything" or "sell everything." It is to anchor the position around June 3 evidence: AI revenue, margin quality, customer concentration, supply security and management visibility into 2027.

FAQ

Frequently asked questions

What is the latest Broadcom stock story?

The latest Broadcom stock story is the sequence of AI infrastructure catalysts: Q1 FY2026 revenue of $19.311 billion, Q2 guidance of about $22.0 billion, an April 6 Google/Anthropic 8-K, an April 14 Meta MTIA expansion and a June 3 Q2 earnings catalyst.

How much AI revenue did Broadcom report in Q1 FY2026?

Broadcom reported Q1 FY2026 AI revenue of $8.4 billion, up 106% year over year, and said it expects AI semiconductor revenue of $10.7 billion in Q2.

What did Broadcom announce with Google and Anthropic?

Broadcom said it will develop and supply future Google TPUs and networking components through up to 2031, while Anthropic will access through Broadcom about 3.5 gigawatts of next-generation TPU-based compute capacity beginning in 2027.

What did Broadcom announce with Meta?

Broadcom and Meta announced an expanded multi-year, multi-generation MTIA partnership with an initial commitment above 1 gigawatt and a sustained multi-gigawatt rollout roadmap.

Should investors buy Broadcom stock now?

This article does not make buy or sell recommendations. Investors should weigh Broadcom AI momentum against valuation, customer concentration, debt, margin quality and June 3 Q2 earnings execution.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Muhammad Zeshan Sarwar covers mobile technology, consumer electronics, and the intersection of crypto with mainstream products. He reviews phones and wearables against their shipping firmware rather than launch-day marketing, and tracks the crypto-in-app integrations Apple and Google actually allow on their platforms. His reporting spans hardware launches, iOS and Android ecosystem shifts, and the wallet and payments layer bridging both.