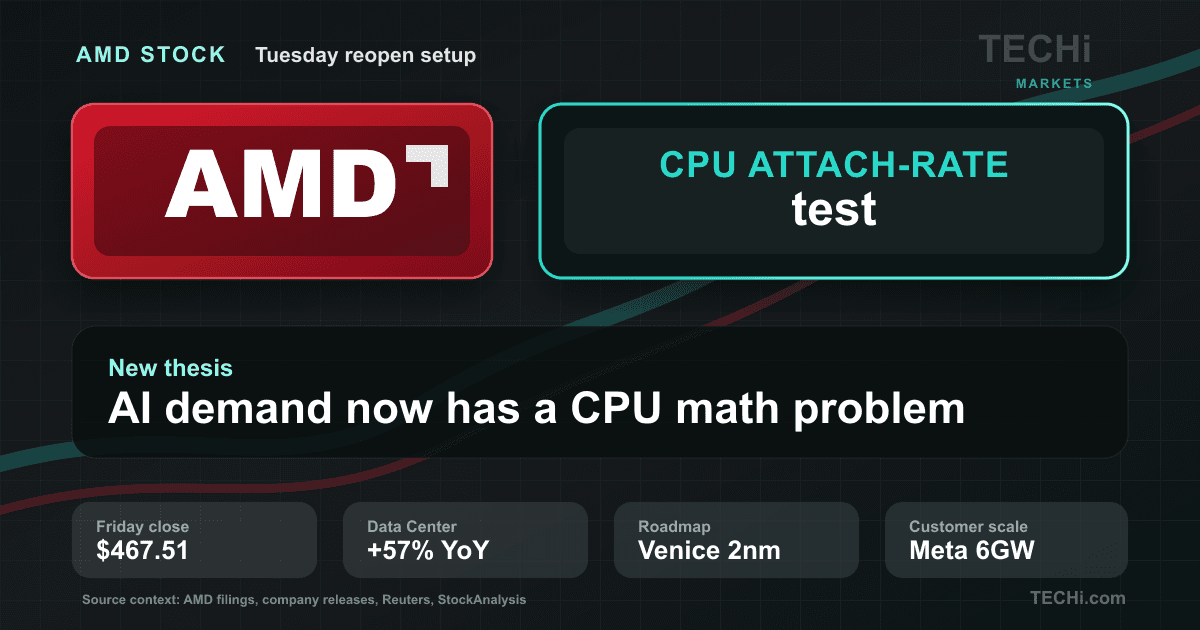

AMD reported Q1 2026 earnings after the close on May 5, and the clean read is not that the company "beat." It is that AMD crossed the line from being a PC-and-console chipmaker with a good AI story to being a data-center company whose earnings power is now led by server CPUs and AI accelerators. Revenue hit $10.3 billion, non-GAAP EPS came in at $1.37, Data Center revenue jumped 57% year over year to $5.8 billion, and management guided Q2 revenue to roughly $11.2 billion. That is why the stock, already up sharply heading into the print, traded above $413 after hours on May 5.

- The headline beatAMD reported Q1 revenue of $10.253B, up 38% YoY, and non-GAAP EPS of $1.37 versus consensus screens around $1.27-$1.29.

- The real storyData Center revenue reached $5.775B, up 57% YoY, driven by EPYC server CPUs and the Instinct GPU ramp.

- Cash generation changed the toneFree cash flow was $2.566B, a record quarterly figure for AMD and a sign that the AI infrastructure cycle is starting to flow through the model.

- Guidance did the damageQ2 revenue guidance of $11.2B, plus or minus $300M, was well above the roughly $10.5B Street setup and implies another sequential step up.

- The riskAt an after-hours price above $413, investors are already discounting a successful MI450 and Helios ramp in the second half of 2026.

The Beat Was Good. The Mix Shift Was Better.

AMD delivered the kind of quarter that changes what investors watch first. The official release showed GAAP gross margin of 53%, GAAP operating income of $1.5 billion, GAAP net income of $1.4 billion and GAAP diluted EPS of $0.84. On a non-GAAP basis, gross margin was 55%, operating income was $2.5 billion, net income was $2.3 billion and diluted EPS was $1.37. Those are strong numbers on their own. The more important detail is where the money came from.

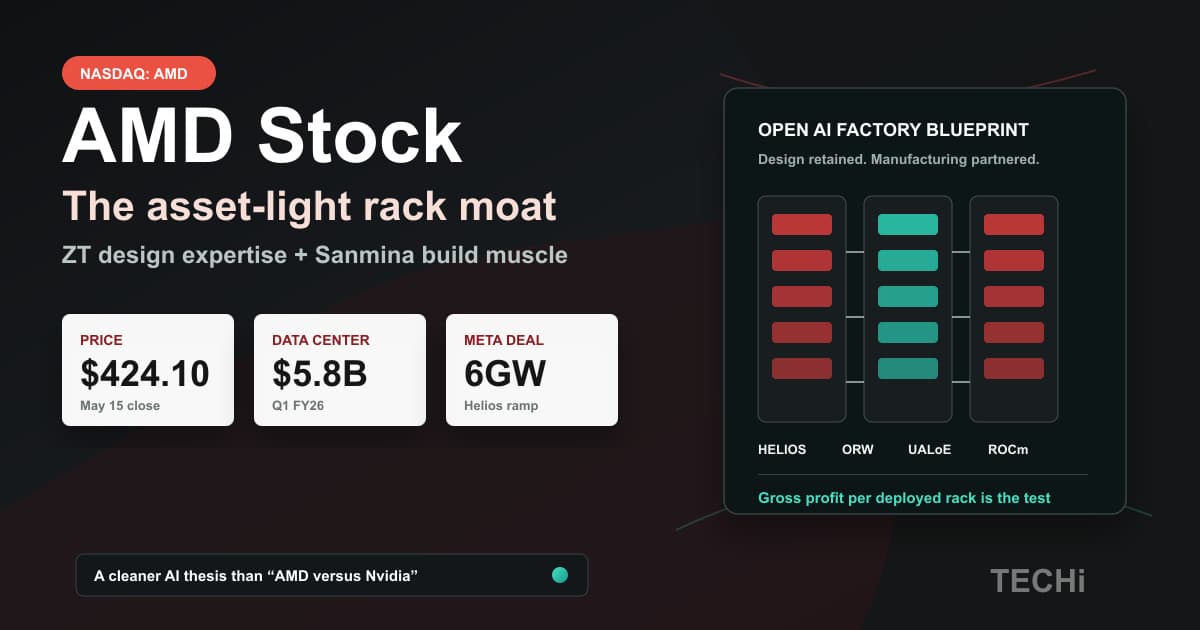

Data Center is now the largest segment by a wide margin. AMD posted $5.775 billion of Data Center revenue in Q1, up 57% from the year-ago quarter and up sequentially from Q4. The segment generated $1.599 billion of operating income. That matters because server CPUs and AI GPUs carry a very different investor narrative than consumer PCs and game-console cycles. The revenue is larger, the customers are more strategic, and the purchase decisions are tied to multi-year AI infrastructure commitments rather than replacement cycles.

Why Data Center Revenue Is the Whole Article

AMD has had good quarters before. What makes this one different is that the company no longer needs investors to imagine a future where AI infrastructure becomes a primary driver. It is already happening in the reported segment table. EPYC server CPUs remain the durable foundation, and Instinct GPU shipments are now large enough to move the consolidated income statement. That combination is much healthier than a one-product AI story.

The strategic implication is simple: AI inference and agentic workloads do not only need accelerators. They need host CPUs, memory bandwidth, networking, platform software and rack-level integration. That is why AMD management emphasized server growth as much as GPU demand. The company is not trying to win the AI cycle by selling a single chip into a single market. It is trying to make EPYC plus Instinct plus Helios a second-source infrastructure platform for hyperscalers that do not want one vendor controlling the entire stack. AMD vs Nvidia Stock: Which AI Chip Maker Deserves Your Money? is the deeper context for that fight.

Guidance Was the Real Catalyst

The Q1 beat was enough to support the stock. The Q2 guide is what forced a repricing. AMD expects revenue of approximately $11.2 billion, plus or minus $300 million. At the midpoint, the company said that represents about 46% year-over-year growth and about 9% sequential growth. Consensus going into the print was closer to $10.5 billion. That gap tells investors AMD is not merely clearing a low bar. It is raising the bar while the AI infrastructure cycle is still accelerating.

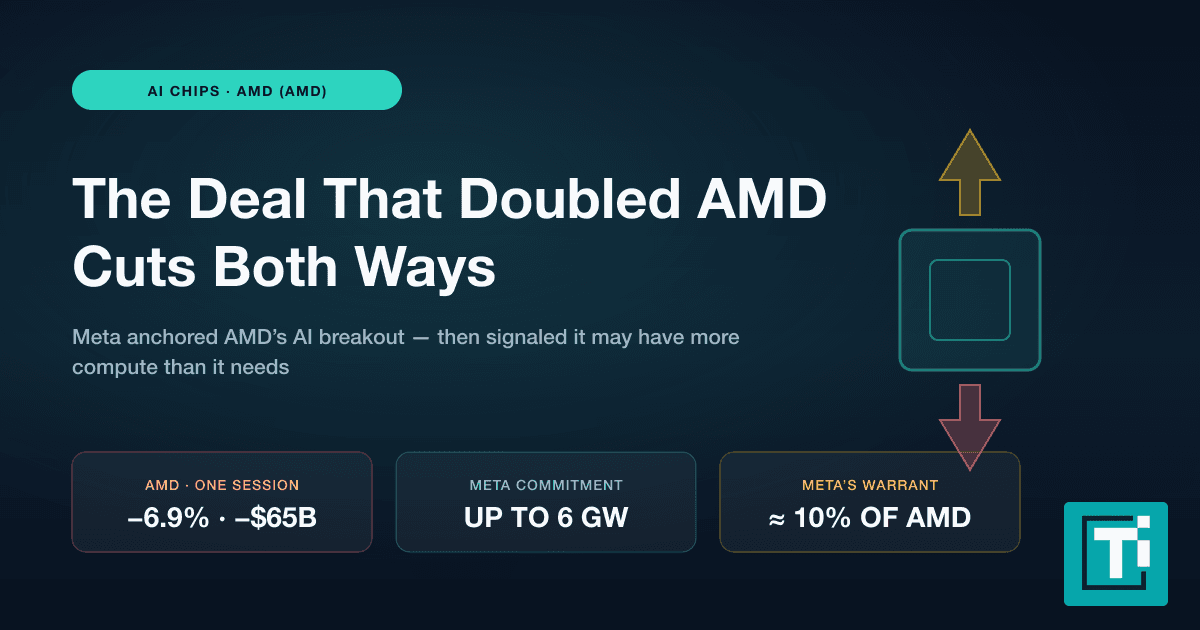

That guide also makes the first half of 2026 look like a bridge rather than a peak. The market is already looking toward the second half, when the MI450 Series and Helios rack-scale platform are expected to ramp more visibly. AMD said customer engagement around MI450 and Helios is strengthening, and the company highlighted Meta plans to deploy up to 6 gigawatts of AMD Instinct GPUs, with the first gigawatt powered by a custom MI450-based GPU. AMD's $60B Meta Deal: How It Breaks NVIDIA's AI Monopoly is the clearest example of why this quarter is being treated as a platform inflection.

Client And Gaming Helped, But They Are No Longer The Center

Client and Gaming revenue was $3.605 billion, up 23% year over year. The client business contributed $2.885 billion, up 26%, helped by Ryzen demand and PC share gains. Gaming was $720 million, up 11%, with Radeon GPU demand offsetting some semi-custom weakness. Those are respectable results. They also show why the story has moved elsewhere. A healthy PC cycle is now a support beam for AMD, not the main event.

Embedded revenue was $873 million, up 6% year over year. That business is still important because Xilinx gave AMD a broader footprint in adaptive computing, industrial systems and edge workloads. But in this quarter, Embedded mostly confirms that AMD has a diversified base underneath the data-center acceleration story. The market is paying for the acceleration, not the ballast.

The Nvidia Question

Every AMD earnings article eventually reaches the same question: does this threaten Nvidia? The honest answer is narrower and more useful. AMD does not need to take Nvidia down to make shareholders money. It needs to become the credible second platform for a market that is too large, too strategic and too power-constrained to be served by one vendor. If AMD captures a durable minority share of AI accelerator deployments while continuing to take server CPU share, the earnings base can expand quickly without Nvidia losing its leadership position.

The harder issue is software. Nvidia still owns the developer mindshare, the training ecosystem and the default procurement path for frontier AI labs. AMD is improving ROCm and wrapping more of the system into rack-scale designs, but customers will only standardize on AMD at scale if deployment friction keeps falling. That is why the MI450 and Helios ramp matters more than the Q1 EPS beat. The beat proves demand. The ramp has to prove trust.

What The Best Coverage Got Right

The official AMD release is the source of truth for the numbers. MarketBeat captured the earnings-screen setup: $1.37 actual EPS versus $1.29 consensus and $10.25 billion revenue versus $9.90 billion expected. Investing.com captured the immediate reaction, including the after-hours move above $413 and the Street focus on server revenue. Bloomberg framed the pre-print risk correctly: AMD had already rallied hard, so the company needed a clean beat and a better guide to justify the move. The guide delivered that.

For readers tracking the paper trail, the May 5 Form 8-K carries the official filing, MarketBeat has the earnings dashboard and call transcript page, Investing.com has the market-reaction wrap, and TheStreet shows how Wall Street had already been lifting expectations into the print. This article uses those sources for numbers and market context, then builds the TECHi view around the business mix shift.

What To Watch Next

1. MI450 and Helios shipment timing

The stock reaction assumes AMD can move from strong customer forecasts to actual H2 shipments without a messy supply ramp. Watch every update on MI450 sampling, Helios production timing, HBM4 supply and customer acceptance.

2. Server CPU share gains

The sleeper upside is not just GPUs. Agentic AI makes server CPU demand more important because inference systems still need host compute, orchestration and efficient general-purpose processing. If EPYC keeps taking share while Instinct ramps, AMD has two engines running at once.

3. Gross margin durability

Non-GAAP gross margin was 55% in Q1 and AMD guided Q2 to roughly 56%. Investors should watch whether AI accelerator volume expands margin or whether aggressive pricing, memory costs and system-level ramp expenses absorb the benefit.

4. Customer concentration

Hyperscaler deals are powerful because they bring visibility and scale. They also concentrate demand. If a small number of mega-customers controls the ramp, AMD has to execute on both product and allocation politics.

Bottom Line

AMD did what it had to do, and then more. Q1 proved that Data Center is now the center of the company. Q2 guidance proved management sees the acceleration continuing. The stock reaction proves investors are willing to pay for AMD as an AI infrastructure platform, not merely a chip-cycle beneficiary.

The next test is execution. If MI450 and Helios ramp cleanly and EPYC keeps gaining share, this quarter will look like the early proof point of a larger re-rating. If the second-half ramp slips, the stock has already priced in enough optimism to punish disappointment. That is the trade after May 6, 2026: AMD finally has the numbers to deserve the AI premium, but now it has to ship into that premium every quarter.

FAQ

Frequently asked questions

How much revenue did AMD report in Q1 2026?

AMD reported Q1 2026 revenue of $10.253 billion, up 38% year over year.

What was AMD non-GAAP EPS in Q1 2026?

AMD reported non-GAAP diluted EPS of $1.37, up 43% from $0.96 in Q1 2025.

How much did AMD Data Center revenue grow?

AMD Data Center revenue was $5.775 billion in Q1 2026, up 57% year over year, driven by EPYC processors and Instinct GPU shipments.

What is AMD guidance for Q2 2026?

AMD expects Q2 2026 revenue of approximately $11.2 billion, plus or minus $300 million, with non-GAAP gross margin around 56%.

Why did AMD stock jump after earnings?

AMD stock jumped after hours because the company beat Q1 estimates, posted strong Data Center growth, generated record free cash flow and guided Q2 revenue above Street expectations.

Is AMD stock a buy after Q1 2026 earnings?

This article does not make buy or sell recommendations. Investors should weigh AMD Data Center momentum against valuation, supply execution, software maturity and customer concentration risks.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Fatima Fakhar covers the AI infrastructure stack for TECHi — GPU roadmaps, ASIC design wins, foundry capacity, and the LLM benchmarks that actually hold up outside vendor demos. She tracks Nvidia, AMD, TSMC, and Broadcom earnings alongside SemiAnalysis teardowns, and tests consumer-facing AI tools herself before writing about them. Her reporting leans skeptical on hype cycles and specific on the numbers that matter: utilization rates, HBM allocations, and the gap between announced and shipping silicon.