The performance of Amazon equity has been poor during the last twelve months; however, when it is compared to major competitors in technology like Google, Meta and Microsoft, it provides a more delicate story.

The company is a concurrent dualistic value system that is a low-margin global retail space and a high-margin cloud and digital services ecosystem. As a result, it is difficult to directly compare it with software-centric counterparts, despite the common goal of leadership in the field of artificial intelligence.

According to recent research, Amazon keeps on recording a healthy growth and retains a justifiable valuation. However, its profitability and free cash flow remain under strain, which is mainly due to the massive amounts of money spent on artificial intelligence infrastructure, data centers, and new technologies.

Although these outlays can be part of long-term growth, they depress short term performance and have increased investor apprehension.

Income Growing: Decent, but Not the Swiftest

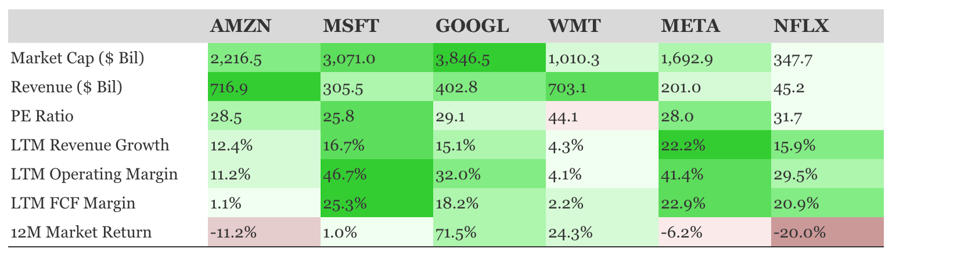

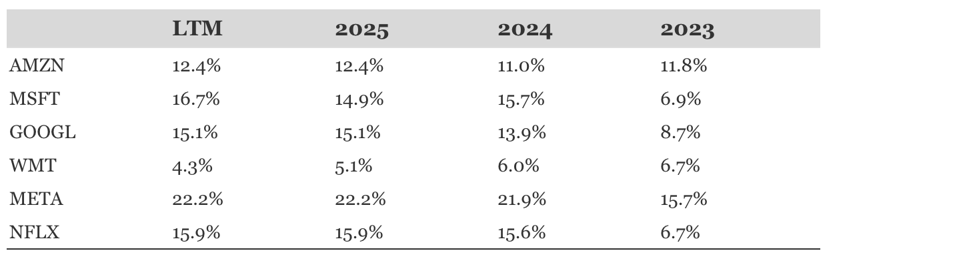

Amazon revenues have also grown at a decent pace of about 12.4% which is notable considering the size of the company. This performance clearly outweighs the achievements of the traditional retail rivals like Walmart, and it serves to prove that Amazon's e-commerce platform, combined with cloud services, still has the potential to draw customers in the difficult environment of the global landscape.

However, in comparison to major players in the field of artificial-intelligence and software, including Microsoft, Google, and Meta, Amazon fails to show up as an engine of growth. There is a faster payoff on digital products, advertising platforms and enterprise-software solutions in these organizations.

This is facilitated by their business models that help increase revenue without the high logistics and fulfilment expenses that continue to plague Amazon. Therefore, Amazon has solid growth, but it is not adequate to counter the concerns of investors about increasing spending and decreasing margins.

Effectiveness versus Microsoft and other Peers

The main weakness of Amazon is profitability. It has an operating margin of about 11.2, indicating the complex nature of the retail and cloud activities. Despite the fact that Amazon Web Services maintains a high-margin profile, the retailing segment continuously undermines the aggregate performance by shipping, labor and infrastructural expenses.

This performance is significantly different to that of Microsoft of about 46.7. The paradigm of software-based Microsoft requires significantly less physical infrastructure, and Google and Meta also have a higher margin of profit due to the nature of digital advertisement and cloud computing being scalable.

That split then highlights an organizational bottleneck to Amazon; despite increasing sales, much of the profit is used to maintain delivery systems, build new warehouses, and increase the amount of AI and cloud computing resources, thus making it difficult to turn growth into higher profitability.

Assessing and Exchange Rejoinder

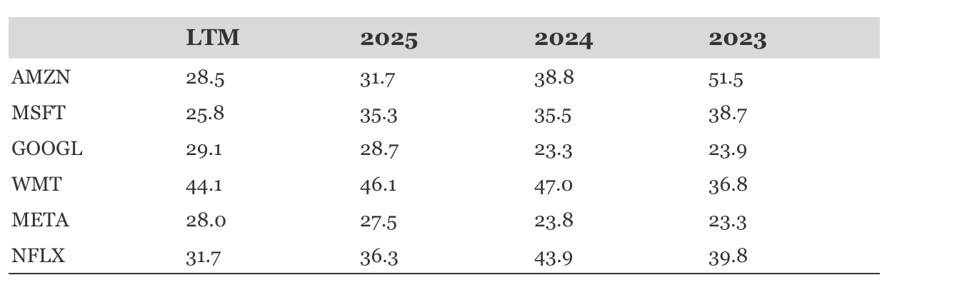

Amazon has experienced an 11.2% depreciation of its equity in the last twelve months, and its value is estimated at a price-to-earnings ratio of 28.5. This appraisal implies that the market participants are still looking forward to the long-term expansion but are not willing to pay high premiums at a time when the profitability is still limited.

In its turn, companies like Microsoft, Google, and Meta are considered to be more obvious beneficiaries of the existing AI cycle. Their cash flows are more stable, and their capital needs are easily met due to strong margins and cash flows.

Conclusion of Essentially Victories

Microsoft currently seems to be the most beneficial member of this group. It has better margins, high software demand and changing AI services that can offer a balanced combination of growth and profitability. The good standings of Google and Meta are also attributed to their powerful platforms and effective operating models. Amazon's future depends on two key factors.

First, Amazon Web Services must maintain and strengthen its cloud dominance. Second, the company must protect its retail margins as competition and market saturation increase. The story may change in case Amazon manages to transform its existing intensive investment in AI into a measurable profit increase. Until the middle term, however, the investors appear to be drawn to the less dirty, more lucrative growth plays provided by Microsoft, Google, and Meta.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Fatimah Misbah Hussain is a seasoned financial journalist at TECHi, specializing in stock market analysis, commodities, and tech sector finance. With a strong background in monitoring public markets and tech companies, she breaks down complex stock movements and commodity price trends into actionable insights.