- The setupBroadcom has already won the custom-AI-silicon narrative; the harder question is whether gigawatt commitments deserve software-like valuation treatment.

- The numbersQ1 fiscal 2026 revenue reached $19.31 billion, AI semiconductor revenue hit $8.4 billion, and management guided Q2 AI semiconductor revenue to $10.7 billion.

- The riskBroadcom's Q1 10-Q says one semiconductor solutions distributor accounted for 42% of net revenue, while the top five end customers represented about 50%.

- The ballastVMware is the cash-flow shock absorber that helps fund R&D, dividends, debt service and buybacks, but European licensing complaints make the software multiple less automatic.

- The testThe June 3 earnings report should be read as a cash-conversion audit, not just another AI revenue beat-or-miss event.

This article is for informational and editorial purposes only. It is not investment advice, a rating, or a recommendation to buy or sell AVGO or any other security.

Broadcom stock is no longer waiting for Wall Street to discover the AI story. The harder question, after a fresh Stooq delayed quote showed AVGO at $420.34 on May 18, is whether investors should value Broadcom's gigawatt-scale AI commitments like recurring software revenue or discount them like concentrated hardware cycles.

That distinction now matters more than the usual Broadcom-versus-Nvidia debate. TECHi already has a full Broadcom stock explainer and a June earnings setup tied to Google, Meta and Anthropic. This piece is about commitment quality: how much of Broadcom's AI revenue deserves an annuity-like multiple, and how much still deserves a semiconductor-cycle discount.

Q1 made the bull case obvious

Broadcom's first-quarter fiscal 2026 print was strong enough to change the valuation conversation. The company reported $19.311 billion of revenue, up 29% from the prior-year period, adjusted EBITDA of $13.128 billion, and free cash flow of $8.010 billion, according to Broadcom's March results release. AI semiconductor revenue reached $8.4 billion, up 106% year over year, and management guided Q2 AI semiconductor revenue to $10.7 billion.

That is why AVGO no longer trades like a diversified chip-and-software conglomerate. If the Q2 AI figure lands near the guide, AI semiconductors will be close to half of company revenue for the quarter. That is not a product line. It is the center of gravity.

But the same math raises the bar. At a market value around $2 trillion, annualizing Q1 free cash flow produces a rough run-rate free-cash-flow yield near the low single digits. That calculation is blunt because Broadcom is growing quickly, but the signal is useful: the stock does not merely need more AI revenue. It needs AI revenue that converts into cash without demanding a much heavier balance sheet.

The gigawatt deals make Broadcom bigger and narrower

On April 6, Broadcom filed an 8-K saying it had entered a long-term agreement with Google to develop and supply future generations of custom TPUs, plus a supply assurance agreement for networking and other AI-rack components through up to 2031. The same Broadcom 8-K said Anthropic would access about 3.5 gigawatts of next-generation TPU-based AI compute through Broadcom beginning in 2027, dependent on Anthropic's continued commercial success.

Meta followed with a separate expansion. Broadcom and Meta said the first phase of the MTIA rollout exceeds 1 gigawatt, with plans for multiple generations of custom silicon and Broadcom Ethernet networking, according to the April partnership announcement.

This is the cleanest version of Broadcom's AI moat. The company is not simply selling chips into a market. It is embedding itself into hyperscaler roadmaps: custom accelerators, high-speed I/O, Ethernet switches, optics, packaging and rack-scale integration. When that relationship works, the switching cost is measured in years.

The tradeoff is concentration. Broadcom's Q1 10-Q says direct sales to one semiconductor solutions customer, a distributor, accounted for 42% of total net revenue. The filing also says the top five end customers accounted for about 50% of total net revenue, and distributors accounted for 55%.

That is not a footnote. It is the stock. Concentration is evidence of strategic importance when AI budgets are expanding. It becomes a source of earnings volatility when one deployment calendar moves.

The cash-conversion clues sit below the headline

Broadcom's headline free cash flow is exceptional. The next level down is more useful.

In Q1, trade receivables rose by $1.315 billion in cash-flow terms, while inventory rose by $692 million. Inventory on the balance sheet increased to $2.962 billion from $2.270 billion at the prior fiscal year-end. A company preparing for hyperscaler AI deployments should build inventory and carry receivables with billings. The point is not that the movement is bad. The point is that investors should not treat every AI revenue guide as if it has already turned into cash.

The next Broadcom print should be read like a cash-quality audit. Does free cash flow keep rising with revenue? Does inventory growth look proportionate to planned AI-rack deployments? Do receivables and contract assets move cleanly into cash? If those answers stay favorable, AVGO's premium multiple has a better foundation.

VMware is the shock absorber, not the side plot

Infrastructure software generated $6.796 billion of Q1 revenue, or 35% of Broadcom's total, even though the segment grew only 1% year over year. That slow growth rate hides the reason VMware matters: cash flow, renewal leverage and operating discipline.

Broadcom is also trying to make VMware relevant to enterprise AI, not just legacy virtualization. On May 5, the company announced VMware Cloud Foundation 9.1, describing it as an AI- and Kubernetes-native private-cloud platform with support across AMD, Intel and Nvidia hardware. If more enterprises run inference and agentic workflows inside private infrastructure for cost, privacy or compliance reasons, Broadcom has a software route into that spend while its custom silicon business serves hyperscalers.

That dual exposure is rare. The risk is that VMware's economics are now politically and commercially sensitive. CISPE, the European cloud-provider group, filed a March 2026 competition complaint alleging VMware licensing changes, bundling, upfront payments and minimum commitments that it said pushed costs up by more than 1,000% for some providers, according to the group's competition complaint statement.

That does not break the VMware thesis. It changes the multiple. A software cash machine with no regulatory heat deserves one valuation. A software cash machine under antitrust pressure deserves another.

The buyback says management believes the cash is real

Broadcom returned $10.9 billion to shareholders in Q1 through dividends and buybacks. The 10-Q shows the company repurchased 23 million shares for $7.85 billion, at an average price of $340.15, and the board authorized another $10 billion repurchase program through December 31, 2026.

The capital-return profile is one reason Broadcom stands apart from most AI hardware names. The company had $67.970 billion of principal debt at February 1 and paid $801 million of Q1 interest expense, so the balance sheet is not clean in a narrow sense. But Q1 free cash flow covered the dividend, the interest bill and a large buyback program.

Buybacks also raise expectations. At this market value, a $10 billion authorization is meaningful but not decisive. AVGO works from here if AI revenue scales, VMware protects margins and free cash flow stays unusually strong.

What to watch on June 3

Broadcom says it will report second-quarter fiscal 2026 results after the close on June 3, 2026, with management hosting a call at 5:00 p.m. Eastern, according to the company's investor center. The release should be read less like a normal earnings print and more like an audit of AI-revenue quality.

The checklist is straightforward. First, did AI semiconductor revenue meet or exceed the $10.7 billion guide? Second, did free cash flow keep pace? Third, did receivables, inventory and contract assets rise in line with revenue or faster than revenue? Fourth, did the customer-concentration language ease or intensify? Fifth, did management describe VCF 9.1 as real incremental AI demand or mainly as retention packaging?

The headline question is not whether Broadcom is an AI stock. It obviously is. The question is whether its AI revenue deserves a software multiple.

TECHi take

The strongest Broadcom bull case is elegant: hyperscalers need custom silicon, Broadcom is embedded in their roadmaps, VMware supplies cash and private-AI relevance, and management returns excess cash with unusual discipline. That can justify a premium valuation.

The strongest bear case is not that AI demand disappears. It is that investors are treating concentrated, gigawatt-scale hardware commitments as if they were recurring software contracts. Broadcom's own filings show exposure to a small number of customers, timing swings, distributor concentration, inventory risk, debt service and VMware regulatory friction.

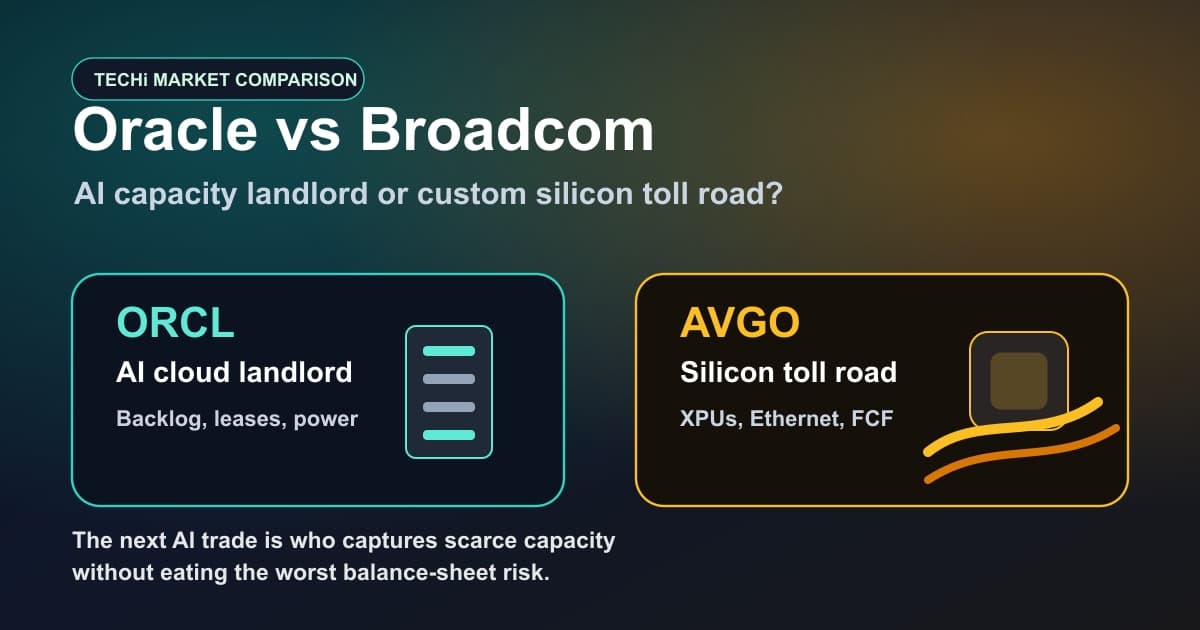

The right frame is not only Broadcom versus Nvidia. It is Broadcom as a cash-converting AI infrastructure underwriter. If June 3 shows the $10.7 billion AI guide converting into free cash flow without stressing working capital, AVGO's premium multiple looks less speculative. If it does not, investors may still own a great company attached to a less forgiving price.

FAQ

Frequently asked questions

What is the main 2026 test for Broadcom stock?

The main test is whether Broadcom's gigawatt-scale AI commitments convert into durable free cash flow or behave like concentrated hardware cycles tied to a few hyperscaler customers.

When does Broadcom report Q2 fiscal 2026 earnings?

Broadcom says it will report second-quarter fiscal 2026 results after the market close on June 3, 2026, with a management call at 5:00 p.m. Eastern.

Why does customer concentration matter for AVGO?

Broadcom's Q1 fiscal 2026 10-Q says one semiconductor distributor accounted for 42% of net revenue and the top five end customers represented about 50%, making deployment timing a major earnings-quality issue.

How does VMware affect the Broadcom stock thesis?

VMware gives Broadcom a high-margin infrastructure software cash-flow base, but licensing complaints in Europe mean investors should treat its software economics as valuable but not risk-free.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Fatimah Misbah Hussain is a seasoned financial journalist at TECHi, specializing in stock market analysis, commodities, and tech sector finance. With a strong background in monitoring public markets and tech companies, she breaks down complex stock movements and commodity price trends into actionable insights.