- The new angleAMD's cleanest AI stock angle is not another MI450 benchmark. It is the asset-light rack-design model behind Helios.

- ZT Systems clueAMD kept ZT design and customer enablement expertise, then moved the manufacturing-heavy piece to Sanmina.

- Investor testThe key metric is gross profit per deployed rack, not only Data Center revenue growth.

- Partner proofHPE, Celestica, TCS and Meta give AMD a visible path from open standards to deployable AI systems.

- Main riskOpen rack standards can help AMD win deployments while also limiting proprietary margin capture.

This article is for informational purposes only and does not constitute investment advice. TECHi and its authors may hold positions in securities mentioned. Always do your own research and consult a licensed financial advisor before making investment decisions.

AMD stock has spent May inside a familiar argument: can MI450, Helios and ROCm make Advanced Micro Devices a real second source for Nvidia-class AI compute? That question matters. By May 18, though, it is no longer the most interesting part of the setup.

TECHi has already covered the AMD Q1 earnings beat, the next AMD AI platform test, the broader AMD stock forecast, and the AMD versus Nvidia stock debate. The sharper question now is whether AMD is building a rack-design business that can turn open AI infrastructure into deployable systems without becoming a low-margin hardware assembler.

That distinction matters because AI factories are not bought like loose chips. The buyer needs CPUs, GPUs, networking, power, cooling, firmware, software, validation, field support and a manufacturing path that does not break when the deployment moves from a demo rack to hundreds of megawatts. The stock market can model accelerator units. It has a harder time modeling time-to-deployment. AMD is trying to make that timing problem part of its moat.

Why ZT Systems is the cleaner AMD angle

The easy read on AMD's ZT Systems deal was that AMD wanted to copy Nvidia's full-stack playbook. That is only half right.

AMD completed the ZT Systems acquisition in March 2025 and said the transaction combined rack-level expertise with AMD GPUs, CPUs, networking silicon and ROCm software. But the more revealing move came later. AMD agreed to sell ZT's U.S.-headquartered data center infrastructure manufacturing business to Sanmina while keeping the rack-scale AI design and customer enablement teams.

That is the article. AMD did not simply buy a factory. It bought deployment knowledge, kept the design layer, and pushed manufacturing scale to a partner.

The 2025 annual report fills in the accounting spine. AMD said it completed the ZT acquisition for $3.2 billion in cash and 8.3 million AMD shares, retained selected intellectual property and design employees, sold the ZT manufacturing business to Sanmina in October 2025, and entered a manufacturing services agreement with Sanmina with an initial five-year term. In plain English: AMD wants the customer-facing rack design intelligence, not the full manufacturing burden.

That is a different stock story from "AMD sells more GPUs." It is closer to "AMD becomes the architect for open AI racks while someone else handles more of the factory-scale build." If it works, AMD can improve deployment speed and customer confidence without carrying every manufacturing dollar through its own income statement.

The financial test is gross profit per deployed rack

AMD's first-quarter 2026 numbers gave the company permission to make a bigger claim. The May 5 financial release showed revenue of $10.253 billion, GAAP gross margin of 53%, non-GAAP gross margin of 55%, and Data Center revenue of $5.775 billion. Management guided second-quarter revenue to about $11.2 billion, plus or minus $300 million, with non-GAAP gross margin around 56%.

Those numbers are strong, but they also create a cleaner test. If Helios ramps as a true rack-scale platform, investors should not only ask how much Data Center revenue AMD adds. They should ask how many dollars of gross profit come with each deployed rack.

That is where the asset-light model becomes important. If AMD can keep system design, validation, customer enablement and silicon attach while Sanmina and other partners absorb more of the manufacturing mechanics, AMD may get a better mix than a vertically heavy rack business would allow. If the model fails, rack-scale revenue could look impressive while gross margin and working capital quietly disappoint.

This is the next AMD metric I would watch after the Q1 beat: not only Data Center revenue growth, but Data Center operating income, inventory, free cash flow conversion and non-GAAP gross margin as Helios starts contributing more visibly.

Helios is the product, but the ecosystem is the bet

Helios is AMD's attempt to make open AI infrastructure concrete. At the 2025 Open Compute Project Global Summit, AMD showed Helios as a rack-scale AI reference platform aligned with Meta's Open Rack Wide standard. The company said Helios uses AMD Instinct GPUs, EPYC CPUs, Pensando networking, ROCm software, liquid cooling, OCP DC-MHS, UALink and Ultra Ethernet Consortium architectures.

That sounds like a list of standards until you translate it into procurement language. Hyperscalers and sovereign AI buyers do not only want a benchmark. They want a deployment path that multiple vendors can support. Nvidia's advantage is integration. AMD's answer is a more open integration pattern.

The partner map is starting to matter. HPE said it would offer AMD Helios AI rack-scale architecture worldwide in 2026, including HPE Juniper Networking scale-up switching developed with Broadcom. Celestica and AMD announced a March 2026 collaboration in which Celestica would handle R&D, design and manufacturing for Helios scale-up networking switches. TCS and AMD announced a 200MW Helios-based blueprint for India through HyperVault, aimed at enterprise and sovereign AI deployments.

None of that guarantees revenue quality. It does show that Helios is moving from slideware into a channel strategy. AMD needs that channel because a rack-scale product is not won one chip at a time. It is won through repeatable deployment patterns.

Meta makes the clock visible

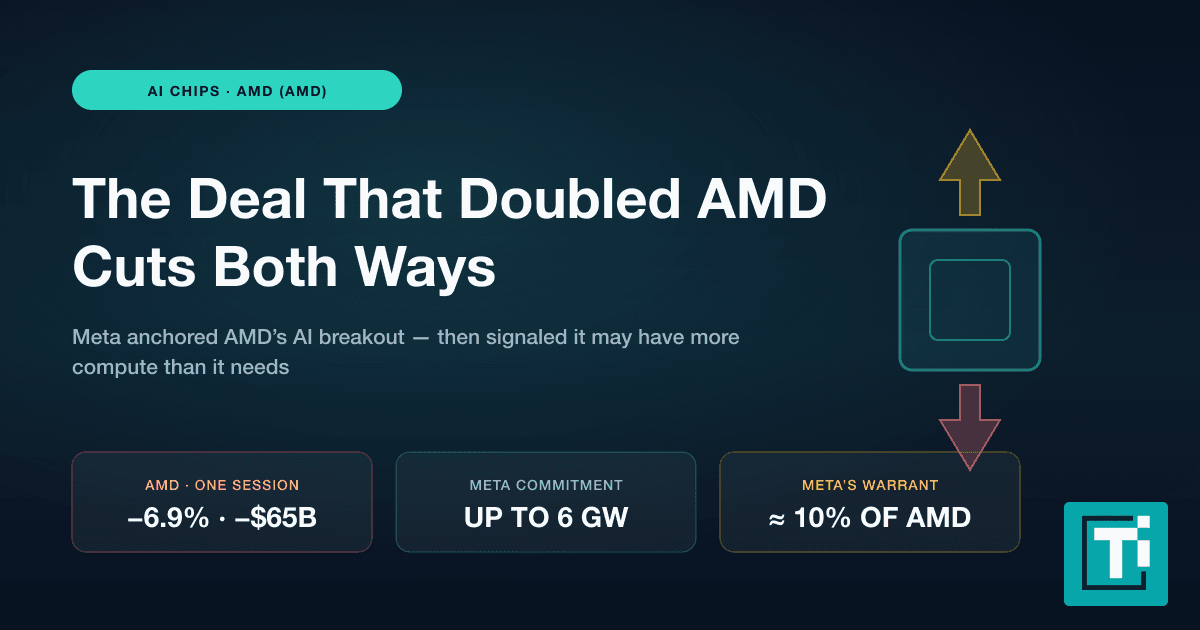

Meta is the timing anchor. In February 2026, AMD and Meta announced a multi-year agreement to deploy up to 6 gigawatts of AMD Instinct GPUs. AMD said the first gigawatt would begin shipments in the second half of 2026, built on Helios, using a custom MI450-based GPU, 6th Gen EPYC CPUs code-named Venice, and ROCm.

That means the asset-light rack thesis has a clock. Investors do not have to wait forever for evidence. The second half of 2026 should begin showing whether AMD can turn a hyperscale roadmap into shipped infrastructure, whether partner manufacturing holds schedule, and whether the gross margin profile stays healthy.

The Meta deal also changes how to read AMD's stock move. AMD closed May 15 at $424.10, down 5.69% on the day after a huge post-earnings run, according to Yahoo Finance's regular-session quote screen. That is not a broken thesis. It is a stock digesting a lot of good news before the hardest deployment phase begins.

At this price, the market is not paying for a small GPU challenger. It is paying for a second AI infrastructure platform. The difference is enormous.

Why this could help AMD more than another benchmark

Benchmarks are useful, but they are also temporary. Nvidia, AMD, Broadcom, Google, Amazon and custom silicon teams will keep trading performance claims. The more durable issue is whether customers can deploy useful capacity at scale.

This is where AMD's rack-design strategy is underrated. AMD does not need every customer to abandon Nvidia. It needs enough customers to believe there is a credible second system path for large AI clusters. That path has to reduce single-vendor dependency, fit existing data center constraints, support open networking, and make migration from smaller pilots to large deployments less painful.

ZT's design teams can help AMD learn from cloud customers before the order is final. Sanmina can give AMD a manufacturing path without forcing AMD to become a heavy EMS operator. HPE, Celestica and TCS can turn Helios into something buyers can procure, service and regionalize. Meta gives the platform a large workload anchor.

That combination is more interesting than an AMD-versus-Nvidia bar chart. Nvidia still has the deeper software moat, the stronger accelerator economics and far higher Data Center scale. But AMD's best chance is not to clone Nvidia. It is to make open rack-scale AI infrastructure a safer buying decision.

If AMD succeeds there, the stock deserves a different question: how much of the AI factory bill of materials can AMD influence even when it does not own every layer?

The bear case: open racks can become open margins

The risk is built into the same thesis. Open standards help customers trust AMD, but open standards also make it harder for AMD to claim proprietary economics.

If Helios becomes a common open blueprint, partners and customers may capture a lot of the value. Hyperscalers can use AMD to negotiate better terms with Nvidia. OEMs and manufacturing partners can own more of the customer relationship. Standards can reduce friction, but they can also reduce pricing power.

There is also execution risk. Rack-scale AI systems are difficult because power, cooling, networking, firmware, storage, scheduling and serviceability all have to work together. A delay in one layer can delay recognition in another. AMD's own Q1 materials still frame many Helios and MI450 claims as forward-looking, and that is the right way to treat them before volume deployments are visible.

The manufacturing partnership lowers one risk but creates another. If AMD relies on partners for complex rack and cluster-scale production, it needs partner quality, supply-chain timing and customer handoffs to work. Investors should not assume an asset-light strategy is automatically asset-easy.

What I would ask AMD next

The next AMD stock questions should be more specific than "How big is AI demand?" Demand is already visible. The better questions are operational.

- How much of future Data Center growth is coming from rack-scale systems rather than standalone CPUs or accelerators?

- Can AMD quantify Helios-related gross margin or at least comment on whether rack-scale mix is accretive, neutral or dilutive?

- Is Sanmina's five-year manufacturing services agreement enough to support the first wave of cloud deployments?

- How many Helios deployments are moving from co-design to purchase commitments?

- Are HPE, Celestica and TCS expanding AMD's reach or mostly supporting known hyperscaler demand?

- Does ROCm adoption improve because Helios reduces integration work for customers?

The answers will tell investors whether AMD is building a business model or only a product roadmap.

The bottom line

AMD stock is no longer just a bet on a faster accelerator. It is a bet on whether AMD can make open AI infrastructure deployable at the rack level.

That is why ZT Systems and Sanmina matter. AMD bought design expertise, kept the customer enablement layer, sold the manufacturing-heavy part, and is now trying to use Helios as the system pattern that ties together Instinct, EPYC, Pensando, ROCm and open networking standards.

The bull case is elegant: AMD becomes the asset-light architect of open AI factories. The bear case is equally clean: open systems help AMD win seats at the table but leave too much profit with customers, OEMs, manufacturing partners and cloud operators.

That is the AMD stock debate I would track on May 18. Not whether AMD can post another strong AI quarter. It already did. The better question is whether AMD can turn rack-scale design into gross profit, not just headlines.

FAQ

Frequently asked questions

What is the new AMD stock angle on May 18, 2026?

The new angle is AMD's asset-light rack-design strategy: AMD retained ZT Systems design and customer enablement expertise, moved manufacturing to Sanmina, and is using Helios to make open AI infrastructure deployable at rack scale.

Why does ZT Systems matter for AMD stock?

ZT Systems matters because it gave AMD rack-scale design and customer deployment expertise. AMD kept that layer while divesting the manufacturing-heavy business, which could improve time-to-deployment without turning AMD into a full manufacturing operator.

What is AMD Helios?

AMD Helios is a rack-scale AI architecture built around AMD Instinct GPUs, EPYC CPUs, Pensando networking, ROCm software and open infrastructure standards such as Open Rack Wide, UALink and Ultra Ethernet.

What metric should investors watch for this AMD thesis?

Investors should watch Data Center operating income, non-GAAP gross margin, inventory, free cash flow conversion and evidence that Helios deployments add high-quality gross profit rather than only headline revenue.

What is the biggest risk to the AMD rack-design thesis?

The biggest risk is that open rack standards help AMD win deployments but limit proprietary economics, leaving more value with hyperscalers, OEMs, manufacturing partners or cloud operators.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Warisha Rashid writes about the intersection of corporate strategy, venture capital, and macro for TECHi — why certain acquisitions close when the Fed pivots, why a Series C prices at a markdown, and how capital rotation reshapes competitive positioning. She reads PitchBook, CB Insights, and S&P Capital IQ filings alongside the earnings commentary most coverage ignores. Her work focuses on M&A rationale, startup unit economics, and the policy signals that move private markets before they show up in public ones.