- The testAMD's Q1 beat was strong, but investors now need proof that the company can turn AI demand into a broader infrastructure platform.

- The market moveAMD closed May 7 at $408.46 in TECHi's live quote stack, down 3.09% after a sharp post-earnings rally.

- The enterprise signalRackspace and AMD announced an MOU for a governed Enterprise AI Cloud using Instinct GPUs and EPYC CPUs.

- The network angleOpenAI's MRC work gives AMD's Pensando networking technology a more visible role in AI-cluster utilization.

- The riskOpen infrastructure can help AMD win deployments, but it can also reduce moat claims unless execution and margins follow.

AMD gave Wall Street the earnings beat it wanted. Now the harder part begins.

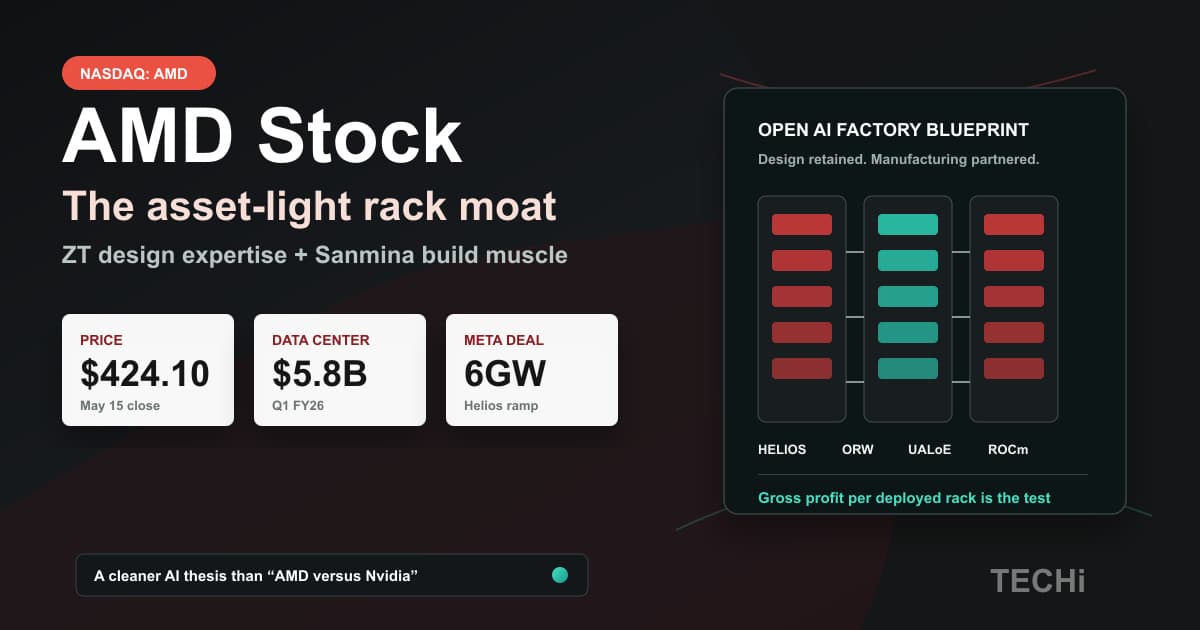

After the company reported $10.253 billion in first-quarter revenue and $5.8 billion in Data Center revenue, investors are watching whether AMD can turn stronger demand for EPYC CPUs and Instinct accelerators into a broader AI infrastructure business. The question is no longer whether AMD has momentum. It is whether that momentum can survive the next test: enterprise deployments, networking, software adoption and margins.

AMD closed May 7 at $408.46 in TECHi's live quote stack, down 3.09% on the session after a sharp post-earnings rally. That pullback does not erase the quarter. It makes the next part of the thesis cleaner. The market has rewarded the growth. Now it needs proof that AMD can become more than a supplier of AI chips.

The earnings beat gave AMD room to make a bigger claim

AMD's May 5 earnings release showed first-quarter revenue of $10.253 billion, non-GAAP EPS of $1.37, and Data Center segment revenue up 57% year over year to $5.8 billion. The company said the data-center gain came from EPYC server demand and the continued Instinct ramp. It also guided second-quarter revenue to about $11.2 billion, plus or minus $300 million, with non-GAAP gross margin expected near 56%.

Those are strong numbers. TECHi's earlier AMD Q1 earnings analysis covered the beat, the guidance raise, and the data-center mix shift in detail. This article is about what comes after that print.

The distinction matters for AMD stock. If the company is mainly selling more chips into a hot AI cycle, investors will eventually bring the debate back to supply, pricing, share and gross margin. If AMD is building a more complete AI infrastructure platform, the market can start looking at attach, software stickiness, customer roadmaps and full-stack deployments.

That is the harder claim, and it needs more evidence.

EPYC is becoming part of the AI control plane

AMD's earnings language matters because the company did not frame AI growth only around accelerators. It tied demand to both high-performance CPUs and GPUs as inferencing and agentic AI workloads scale. That is important because large AI systems do not run on accelerator headlines alone. They need host compute, scheduling, retrieval, memory movement, networking and inference operations that keep expensive clusters productive.

That puts EPYC closer to the center of the AMD stock debate. For years, AMD's server CPU gains were treated as a strong but familiar share story. The new version is more strategic. CPUs become part of the control plane around AI workloads, sitting beside accelerators and helping move data through the system.

That does not make AMD equal to Nvidia. It does change the comparison. TECHi's AMD versus Nvidia stock analysis focused on AI chip economics. The next competitive test is utilization: which company helps customers get more useful compute out of the infrastructure they already bought?

Rackspace adds an enterprise AI proof point

The freshest development is not another analyst target. Rackspace and AMD announced a memorandum of understanding on May 7 to build a governed Enterprise AI Cloud for regulated enterprises and sovereign workloads. Rackspace described the proposed stack as a private and hybrid AI environment using AMD Instinct GPUs, AMD EPYC CPUs and Rackspace's operating model.

That is useful because regulated enterprises do not only need a faster accelerator. They need deployment control, service accountability, data governance, inference operations and predictable infrastructure. If AMD can show up in those environments as part of a stack, the stock story gets broader than a chip-by-chip comparison.

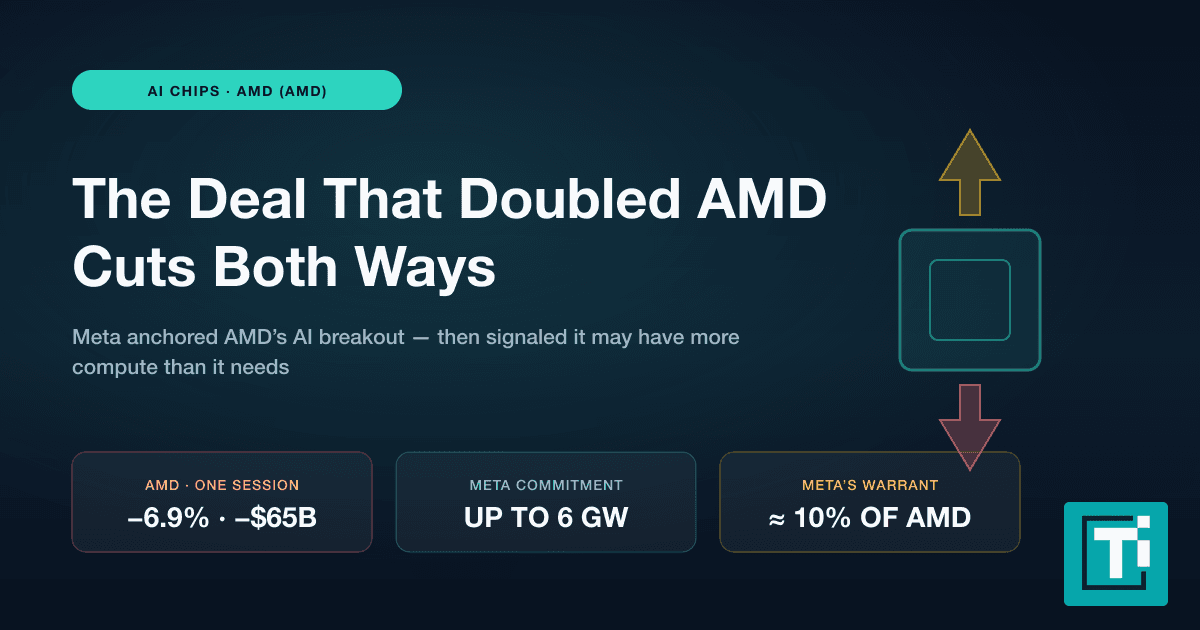

There is a limit. An MOU is not booked revenue. It is a framework, not proof of scale. Investors should treat it as a signal, not a purchase order. Still, it is the kind of enterprise proof point AMD needs after its Meta AI infrastructure deal pushed the narrative toward hyperscale demand.

OpenAI's networking work raises the same question

The networking side makes AMD's platform test sharper. OpenAI said it worked with AMD, Broadcom, Intel, Microsoft and Nvidia on Multipath Reliable Connection, or MRC, a protocol meant to improve large AI training networks by spreading traffic across many paths and improving resilience. AMD separately said it helped shape the MRC specification and connected the work to its Pensando networking technology.

This is where AMD can make a more serious infrastructure argument. Nvidia's lead is not just GPUs; it is the ability to make the cluster work. AMD has to prove it can compete in a more open, multi-vendor version of that world. EPYC handles host compute. Instinct handles acceleration. Pensando addresses programmable networking. ROCm has to keep improving so customers can run real workloads without friction.

For investors, that turns the question from "Can AMD sell more AI chips?" into "Can AMD help customers run AI systems better?" That is a more valuable question, but it is also harder to answer.

Goldman's target is a headline, not the thesis

TheStreet reported on May 7 that Goldman Sachs upgraded AMD to Buy and raised its price target to $450 from $240 after earnings. That number will get attention because it is simple. It should not become the whole argument.

A higher target only holds if AMD's AI revenue becomes more visible, more profitable and more platform-like. The Q1 print gave AMD momentum. Rackspace gives it an enterprise AI proof point. OpenAI's MRC work gives it a networking relevance story. Meta gives it a hyperscale anchor. The missing piece is sustained execution through product ramps, software adoption and margin durability.

That is why the May 7 pullback matters. A stock can be fundamentally stronger and still pause after a violent move. For AMD, the pause shifts the debate from excitement to proof.

The risk is that open infrastructure helps everyone

The same open-stack story that helps AMD also limits how much credit AMD alone can claim. OpenAI's MRC work includes several major chip and infrastructure players, including Nvidia. Open networking standards can reduce friction for customers, but they do not automatically create a proprietary AMD moat.

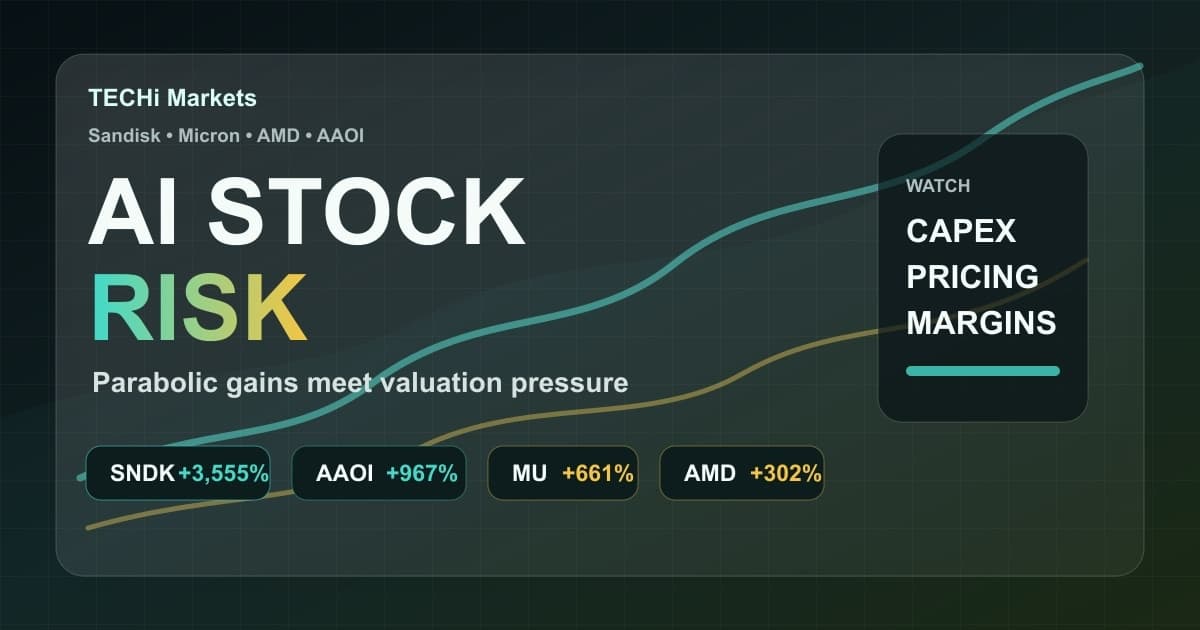

AMD also has ordinary semiconductor risks underneath the AI story. Its earnings materials cite competitive pressure, export restrictions, component availability, customer concentration and manufacturing execution as risks. Gross margin is especially important now because investors have already rewarded revenue growth. If AI infrastructure revenue scales without enough margin expansion, the platform argument weakens.

The cleaner read on AMD stock is this: the Q1 beat gave the company credibility, but the next move depends on proof that EPYC, Instinct, Pensando and ROCm can work together as a durable AI infrastructure stack. That is a stronger story than a one-day earnings reaction, and it is the test investors should watch next.

FAQ

Frequently asked questions

Why is AMD stock's CPU story no longer hidden?

AMD's Q1 2026 release tied data-center growth to demand for high-performance CPUs and accelerators as inferencing and agentic AI scale, making the CPU thesis part of the public stock debate.

What is the next test for AMD stock after Q1 earnings?

The next test is whether AMD can prove a full AI infrastructure platform story built around EPYC CPUs, Instinct GPUs, Pensando networking and ROCm software, rather than only a strong chip-sales cycle.

What did Rackspace announce with AMD?

Rackspace and AMD announced a memorandum of understanding on May 7, 2026 for a governed Enterprise AI Cloud using AMD Instinct GPUs and EPYC CPUs for regulated and sovereign workloads.

How does OpenAI's MRC work affect AMD?

OpenAI's MRC work matters because AMD helped shape the specification and linked it to its programmable networking technology, giving AMD a role in the AI-cluster utilization debate beyond GPUs alone.

Is this AMD stock article investment advice?

No. The article is editorial analysis for informational purposes and is not a recommendation to buy or sell AMD stock.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

CEO of TECHi. Building the operating system for serious tech investors. Previously led engineering at scale. Focus: AI capex thesis, semiconductor supply chain, and the equity tape.