- The undercovered catalystOpenAI's MRC protocol makes AI networking reliability a stock-analysis issue for NVDA, not just an infrastructure engineering story.

- Why it mattersIf Spectrum-X and ConnectX keep giant clusters productive, NVIDIA can capture more value per AI factory beyond the GPU sale.

- The visible headlineGoldman Sachs kept a Buy rating and $250 target, implying roughly 18% upside from TECHi's $211.50 NVDA quote snapshot.

- The open-standard riskMRC also helps AMD, Broadcom, Intel and Microsoft, so it could reduce friction for mixed AI clusters over time.

- The earnings testThe next report must prove Data Center demand, margin durability and networking attach are strong enough to support the premium valuation.

The visible Nvidia story on May 7 is easy to understand: Goldman Sachs kept a Buy rating and a $250 target on NVDA, according to MarketScreener's analyst-rating summary. Against TECHi's $211.50 quote snapshot, that target implies roughly 18% upside. That is the headline Google News is already full of.

The more interesting stock story is not the target. It is the network.

OpenAI said on May 5 that it partnered with AMD, Broadcom, Intel, Microsoft and NVIDIA to develop Multipath Reliable Connection, or MRC, a protocol meant to improve GPU networking performance and resilience in large AI training clusters. NVIDIA followed on May 6 by saying MRC was proven first and optimized on NVIDIA Spectrum-X Ethernet hardware. That matters for Nvidia stock because the AI factory bottleneck is shifting from buying more GPUs to keeping enormous clusters fed, synchronized and productive.

Why MRC changes the NVDA debate

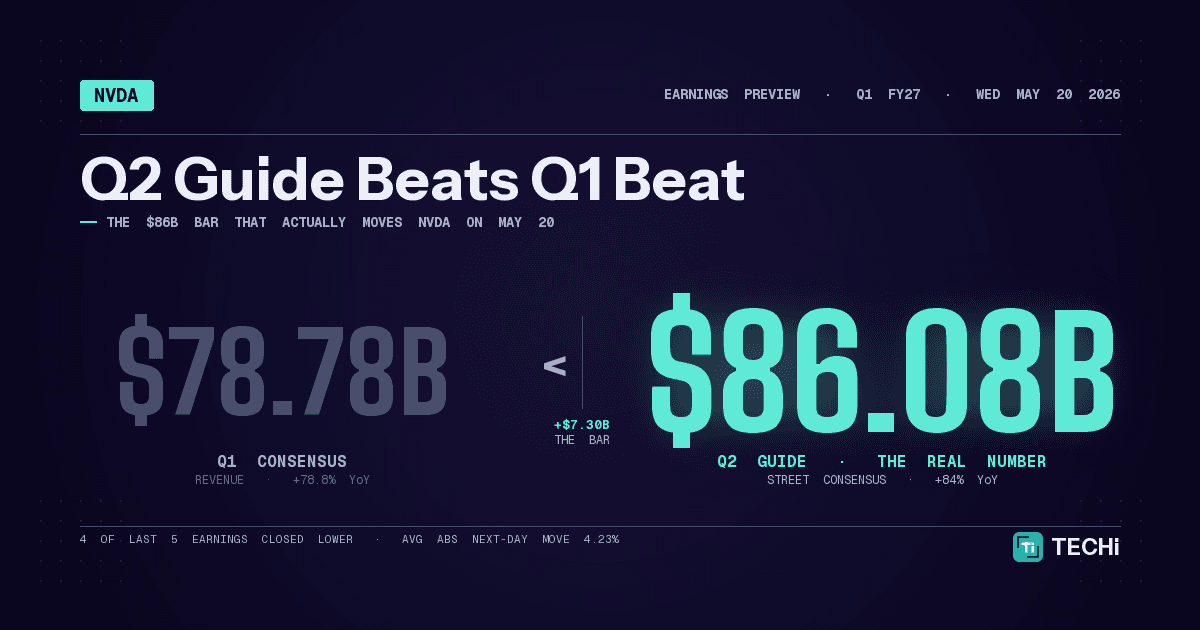

A standard Nvidia bull case starts with chips. It points to Blackwell demand, Rubin timing, hyperscaler capex and the company's latest earnings guide. Those facts are still central. NVIDIA reported Q4 fiscal 2026 revenue of $68.1 billion and Data Center revenue of $62.3 billion, then guided Q1 fiscal 2027 revenue to $78.0 billion, plus or minus 2%, while assuming no Data Center compute revenue from China.

MRC adds a different question: how much of every AI infrastructure dollar can NVIDIA capture after the GPU is already sold?

OpenAI's post says MRC lets a single transfer spread packets across hundreds of paths, route around failures in microseconds and simplify network control planes. It also says MRC is already deployed across OpenAI's largest NVIDIA GB200 supercomputers, including Oracle Cloud Infrastructure's Abilene, Texas site and Microsoft's Fairwater systems. Those are not marketing demos. They are production clusters where wasted GPU time is real money.

That is why TECHi's existing Nvidia stock guide should be read together with the newer AI networking news. The stock is no longer just a read on accelerator units. It is a read on rack-scale attach: GPUs, CPUs, NVLink, Spectrum-X, ConnectX, DPUs, switches, software and serviceable uptime.

The hidden valuation lever is utilization

OpenAI explains the problem clearly: in synchronous pretraining, one late transfer can slow the entire job, and link or switch failures become more frequent as clusters grow. Its MRC design can connect more than 100,000 GPUs with only two tiers of Ethernet switches in a multi-plane network, reducing components, power and failure points compared with conventional designs.

For investors, the important word is not just speed. It is utilization.

If a hyperscaler is spending billions on AI factories, a network layer that prevents expensive accelerators from sitting idle can justify higher system-level spending. NVIDIA's own Spectrum-X MRC post frames the protocol as a way to keep GPU utilization high by balancing traffic across available paths and rerouting around failures at hardware speed. That pushes the bull case beyond the usual "sell more Blackwell" line.

This is also where Corning's NVIDIA data-center story fits. AI factories are not one component. They are power, cooling, optics, glass, networking, racks, GPUs and software stitched into one capital project. The better NVIDIA makes the whole stack behave, the harder it is for buyers to treat the GPU as a commodity line item.

Why openness is both bullish and dangerous

The bear case starts with the same fact. MRC is open. AMD says OpenAI, Microsoft and industry partners are contributing MRC to the Open Compute Project so the broader ecosystem can use it. That means AMD, Broadcom and Intel can benefit from the same standard that helps NVIDIA's Spectrum-X pitch.

That does not make MRC bearish for NVDA by itself. Open standards often expand a market before they redistribute it. The risk is that MRC gives hyperscalers more confidence to build heterogeneous clusters over time. In that world, NVIDIA still wins if its full stack remains the easiest way to hit performance, uptime and deployment targets. It loses leverage if open networking lets buyers mix NVIDIA, AMD custom accelerators, Broadcom switching and in-house silicon with less friction.

That is why the comparison with AMD's latest AI data-center quarter matters. AMD does not need to dethrone NVIDIA to affect the multiple. It only needs to become credible enough that mega-customers can use it as a second platform. The same logic applies to Broadcom's AI chip and networking setup: custom silicon and networking are not side stories anymore.

What earnings must prove next

The earnings test is straightforward. NVIDIA has to show that the $78 billion revenue guide was not a peak optimism number, that Data Center demand remains supply-constrained rather than budget-constrained, and that gross margins can hold near the mid-70s while systems become more complex.

The MRC news sharpens that test. If management talks about Spectrum-X, Ethernet, rack-scale systems, Vera CPUs, NVLink Fusion or networking attach with more specificity, the market should listen. NVIDIA's fiscal 2026 10-K describes Data Center systems as co-designed with GPUs, CPUs, NVLink switches, DPUs, NICs, scale-out networking and software stacks. That language is the economic model hiding behind the product names.

It also explains why the company's AI infrastructure positioning has held up even when competitors announce big wins. The moat is not only CUDA. It is the operational burden of making a giant AI factory work.

The risks are not small

NVIDIA is priced for excellence, and excellence leaves little room for sloppy execution. The 10-K lays out risks around export controls, China access, supply constraints, customer concentration, product transitions and dependence on global manufacturing partners. The latest company guide explicitly assumes no China Data Center compute revenue, so a China recovery would be upside, but China uncertainty remains a real risk.

There is also a margin risk. Rack-scale systems may increase NVIDIA's dollar content per deployment, but they also carry more components, more supply-chain coordination and more pressure from customers who are writing enormous checks. If the market sees revenue upside but gross margin erosion, the stock can still struggle.

For a broader capex view, TECHi's piece on whether Google can justify massive AI infrastructure spending is the right companion read. Nvidia stock can keep working only if customers continue to convert AI capex into usable compute, and eventually into products with real revenue.

Bottom line for Nvidia stock

The strongest May 7 Nvidia angle is not that Goldman has a $250 target. It is that OpenAI just showed investors where the next bottleneck sits. In giant AI clusters, networking reliability decides how much purchased compute can actually be used.

That is good for NVIDIA if Spectrum-X, ConnectX and the broader rack-scale platform become mandatory infrastructure for frontier AI labs. It is dangerous if open MRC accelerates a future where hyperscalers can stitch together rival accelerators and networking vendors with less pain.

The near-term stock setup is therefore clean. NVDA has momentum, a clear earnings catalyst and a fresh infrastructure proof point. The next leg higher needs more than a beat. It needs evidence that NVIDIA is capturing the AI factory stack, not just the GPU line inside it.

FAQ

Frequently asked questions

What is the hidden catalyst for Nvidia stock?

The undercovered catalyst is OpenAI's MRC networking protocol, which highlights how much value NVIDIA may capture from AI factory networking, utilization and rack-scale systems beyond GPU shipments.

Why does MRC matter for NVDA investors?

MRC is designed to keep very large GPU clusters productive through congestion and failures. If NVIDIA's Spectrum-X and ConnectX hardware become the preferred way to run it at scale, NVDA's revenue opportunity can expand beyond accelerators.

What is the main risk to this Nvidia stock thesis?

MRC is an open standard developed with AMD, Broadcom, Intel, Microsoft and NVIDIA, so it can also make mixed-vendor AI clusters easier for hyperscalers over time.

Is the article recommending buying Nvidia stock?

No. The article is stock analysis for informational purposes only and is not financial advice or a recommendation to buy, sell or hold NVDA.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

CEO of TECHi. Building the operating system for serious tech investors. Previously led engineering at scale. Focus: AI capex thesis, semiconductor supply chain, and the equity tape.