Update: CBRS quote page is live

Cerebras now has a live TECHi quote page for CBRS, with the current price, chart, market data, news, and related analysis. This article remains available as IPO background, so earlier filing or pricing references should be read in historical context.

Track it here: live TECHi CBRS quote page.

This article is market commentary, not financial advice. Newly public stocks can be unusually volatile, and Cerebras has only a limited public trading history.

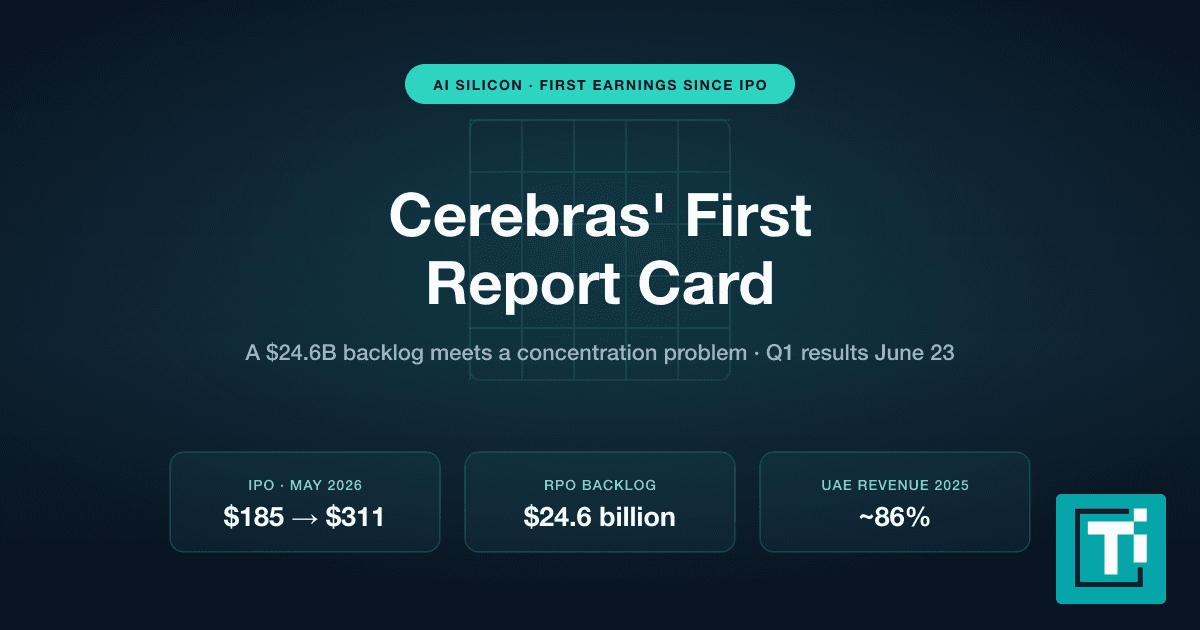

- The dealCerebras priced CBRS at $185, sold 30 million shares, and raised $5.55 billion before any underwriter option exercise.

- The popThe stock opened near $350 and closed its first trading day at $311.07, then traded lower late Friday while remaining far above the IPO price.

- The bull caseOpenAI, AWS, wafer-scale silicon, and high-speed inference give Cerebras a real claim on AI infrastructure spending.

- The riskValuation, customer concentration, operating losses, power constraints, and staged lock-up supply make the post-pop entry point dangerous.

- Our takeCBRS is worth watching closely, but the first clean setup may come after earnings and lock-up data, not during the debut frenzy.

Cerebras did not simply go public. It gave public markets a new pure-play way to bet on the most crowded question in technology: will AI inference move beyond Nvidia's GPU stack, or will every serious challenger become another expensive footnote?

As of May 16, 2026, the answer is still open. Cerebras priced its IPO at $185 a share on May 13, began trading on Nasdaq under CBRS on May 14, opened at $350, hit the mid-$380s intraday, and closed its first session at $311.07. By late Friday trading on May 15, StockAnalysis showed CBRS near $294.83, down from that first-day close but still far above the IPO price.

That is exactly the tension. The IPO was a triumph for Cerebras the company. It is a harder question for investors buying after the pop.

The real story is not 'Nvidia killer'

Calling Cerebras a Nvidia killer is lazy. Nvidia is a platform company with GPUs, CUDA, networking, systems, software, enterprise distribution, and a balance sheet that can answer almost any competitive threat. Cerebras is narrower and more unusual: it built around wafer-scale silicon, selling systems and cloud access for AI training and inference.

The better frame is this: Cerebras is a public-market test of whether speed-hungry inference workloads deserve their own specialist stack. That also makes it a companion story to TECHi's broader read on how Nvidia is becoming the bank of the AI buildout, because Cerebras is now testing whether public investors want financed AI capacity from a specialist, not only from the incumbent platform.

Cerebras says its WSE-3 chip is a wafer-scale processor and says its inference platform can run some workloads up to 15 times faster than leading GPU-based solutions. The company's pricing announcement repeats that performance claim, while the Nasdaq IPO recap highlights the same architecture as the reason investors treated the listing as more than a normal semiconductor debut.

The market is not paying for another chip vendor. It is paying for a possible bottleneck breaker.

What went right

First, the offering itself was cleanly successful. Cerebras sold 30 million Class A shares at $185, above the earlier $115-$125 range and even above the later $150-$160 range. The company raised $5.55 billion before any underwriter option exercise, according to its official IPO pricing release.

Second, the customer story is much stronger than it was during the earlier IPO attempt. Cerebras' prospectus says revenue rose to about $510 million in 2025 from about $290 million in 2024. It also says the company had $24.6 billion in remaining performance obligations at the end of 2025, with OpenAI representing a major future revenue driver. That matters for anyone following the pre-public market around OpenAI's own IPO path, because Cerebras is now one of the cleaner public ways to watch OpenAI-linked infrastructure demand.

Third, the AI market wants a second public AI infrastructure story. Nvidia is still the standard, but the trade has become crowded. Cerebras gives investors a cleaner, more dramatic way to express the idea that inference capacity, power, latency, and model-serving speed will matter as much as training hardware. The AWS piece is also important because Amazon is already trying to define its own AI-chip lane through Trainium, a theme TECHi covered in its Amazon AWS and Trainium analysis.

What can go wrong

The first risk is valuation. At the IPO price, Cerebras already came public at a huge multiple of trailing revenue. When the stock opened around $350, Reuters reported via Investing.com that the implied fully diluted valuation jumped above $100 billion. That makes every execution miss more expensive.

The second risk is revenue concentration. The prospectus says MBZUAI accounted for 62% of 2025 revenue and G42 accounted for 24%, after G42 had represented 85% of 2024 revenue. That is improvement from one angle and still concentration from another. OpenAI and AWS help the story, but they also make the next phase dependent on a few extremely large relationships.

The third risk is quality of profit. Cerebras reported 2025 net income of $237.8 million, but the filing also shows a $145.9 million loss from operations and net income attributable to common shareholders of $87.9 million. The point is not that the company is weak. The point is that investors should not treat the headline profit line as if the core operating model is already mature.

The fourth risk is governance. The prospectus says Class B shares carry 20 votes each and will control about 99.2% of voting power after the offering. Public investors are getting economic exposure, not much control.

The fifth risk is supply and power. AI inference at this scale is not only a chip question. It is a data-center, power, cooling, procurement, and deployment question. Axios noted that investors should watch customer concentration, data-center moratorium pressure, power concerns, and staged lock-up releases after the first-day pop. That is the right checklist.

Our view: great company, dangerous entry point

Cerebras deserved a premium IPO. The product is differentiated, the market is real, and the OpenAI relationship changes the credibility of the story. But a great company can still be a bad first trade if retail investors pay the after-pop price without respecting lockups, concentration, and the first earnings test.

For investors who received IPO allocation at $185, the decision is different from the decision facing someone buying above $290 or $300. Allocation buyers already have a margin of safety from the public-market pop. Open-market buyers are underwriting a much more aggressive version of the story.

The cleanest recommendation is this: do not chase the first emotional candle. Watch the first two earnings reports, the pace of OpenAI deployment, whether AWS turns into binding revenue at scale, and how the stock absorbs lock-up supply. If those data points improve, CBRS can earn part of its premium. If they disappoint, the stock can still be right about AI and wrong at the price.

What to watch next

The first public earnings call will matter more than the IPO pop. Investors should listen for remaining performance obligation conversion, gross margin by hardware versus cloud services, deployment timing, power availability, customer additions outside OpenAI/G42/MBZUAI, and any update on AWS milestones.

The second watch item is insider and employee supply. A normal six-month lock-up cliff is not the only setup here. Axios reported that more shares begin unlocking early and that additional releases come in stages through October. That can be healthy if demand is deep. It can also cap rallies if early holders take liquidity.

The third watch item is Nvidia's response. Cerebras does not need to beat Nvidia everywhere. It needs to win enough high-speed inference workloads where its architecture gives customers a reason to shift spending. If Nvidia narrows the speed gap or bundles economics aggressively, Cerebras will have to prove that its speed advantage converts into durable revenue. For readers comparing the broader chip trade, TECHi's AMD vs Nvidia stock analysis is the better benchmark than simple 'Nvidia killer' talk.

How this changes the IPO market

This is the broader point: Cerebras may have reopened the window for AI infrastructure IPOs. If a specialist chip company can price above range, raise $5.55 billion, and still trade far above issue price after its debut, bankers will test the market with more AI, data-center, power, and model-infrastructure names.

That does not mean every AI IPO will work. It means the market is no longer closed to expensive growth stories if they have real customers, a clear bottleneck, and a narrative that public investors can understand in one sentence.

For Cerebras, the sentence is simple: faster inference is valuable. The hard part starts now: proving that it is valuable enough to support the valuation public investors just gave it.

Earlier TECHi coverage and source trail

TECHi's earlier guide, Cerebras IPO: Valuation, Timeline, How to Invest & Everything You Need to Know, covered the setup before the pricing decision. Our follow-up, Cerebras Raises IPO Range to $150-$160 - 20x Oversubscribed, tracked the demand build before the final $185 price.

For the primary record, use Cerebras' May 13 pricing announcement, the SEC final prospectus, and Nasdaq's IPO debut recap. For market color, compare Reuters' debut report, Axios' post-pop lockup analysis, and Kiplinger's investor-caution piece.

FAQ

Frequently asked questions

What is the Cerebras stock ticker?

Cerebras trades on the Nasdaq Global Select Market under the ticker symbol CBRS.

How much did Cerebras raise in its IPO?

Cerebras priced 30 million Class A shares at $185 each, raising $5.55 billion before any underwriter option exercise.

Should investors buy CBRS after the IPO pop?

The article's view is to avoid chasing the debut frenzy and watch the first earnings reports, customer concentration, lock-up supply, and OpenAI/AWS deployment progress.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Omer Sheikh covers Elon Musk-led and Musk-adjacent companies for TECHi, with a focus on Tesla, xAI, SpaceX, X, Neuralink, The Boring Company, and the public-market read-throughs from their product cycles, capital needs, AI infrastructure plans, supply chains, and regulatory risk. He also follows MicroStrategy/Strategy and its Bitcoin treasury strategy, using his finance background to connect balance-sheet decisions, capital markets, valuation, catalysts, and downside risk. His work is built for readers who want the investment case behind the headline: what changed, what it means for cash flow or market value, and what would prove the thesis wrong.