Update: CBRS quote page is live

Cerebras now has a live TECHi quote page for CBRS, with the current price, chart, market data, news, and related analysis. This article remains available as IPO background, so earlier filing or pricing references should be read in historical context.

Track it here: live TECHi CBRS quote page.

Investment disclaimer: This article is for informational and educational purposes only. It is not financial advice or a recommendation to buy, sell, or hold any security. Newly public stocks can be volatile; verify live market data and consult a licensed financial advisor before making investment decisions.

Update: Cerebras Raises IPO Range to $150-$160

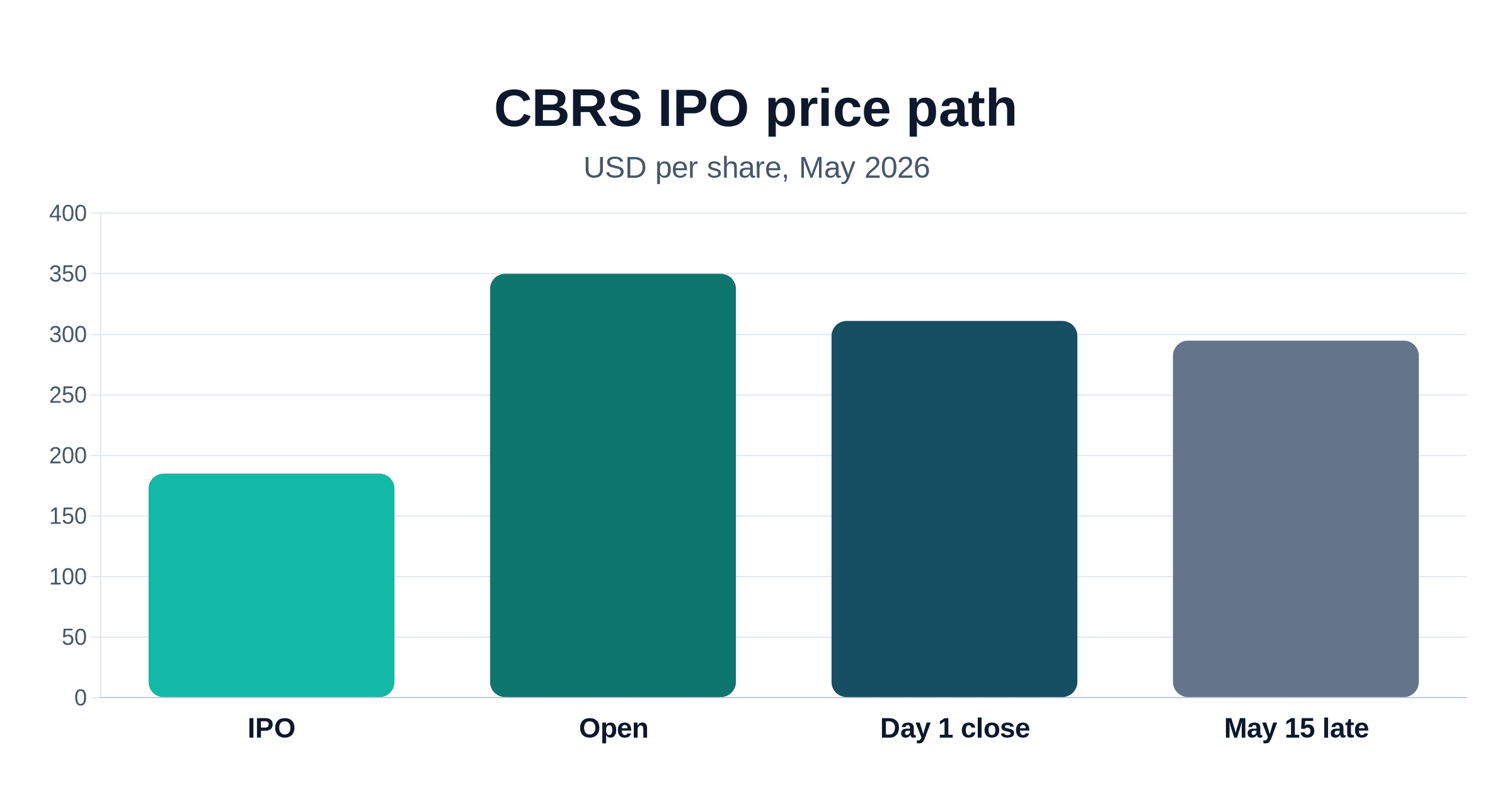

The price range was bumped from $115-$125 to $150-$160 after the underwriter book closed more than 20x oversubscribed, lifting the implied fully diluted valuation to about $48.8 billion and the gross proceeds to up to $4.8 billion. The full breakdown of the bump, the 96x sales multiple, and the OpenAI concentration math lives in TECHi’s pricing-day piece. The sections below preserve the original filing’s $115-$125 numbers for historical record.

- IPO termsCerebras is offering 28 million Class A shares at an updated $150-$160 range (up from $115-$125 after >20x oversubscription) and lists on Nasdaq as CBRS.

- ValuationAt the top of the range, market reports put the IPO valuation near $26.6 billion, above the February private round but below earlier $40 billion chatter.

- OpenAI catalystOpenAI has agreed to add 750MW of Cerebras-backed low-latency compute through 2028, and the S-1 describes a deal valued at more than $20 billion.

- AWS channelAWS plans to deploy Cerebras CS-3 systems in AWS data centers and expose the solution through Amazon Bedrock.

- Main riskThe business has fast revenue growth, but customer concentration, operating losses, export controls and valuation still require caution.

Cerebras is no longer a vague "maybe IPO" story. As of May 6, 2026, the AI-chip company has a live roadshow, a fresh SEC filing, a proposed Nasdaq ticker and a real price range for public investors to evaluate.

The clean headline is this: Cerebras filed an amended S-1 on May 4, 2026 to sell 28 million Class A shares at an expected range of $115 to $125 per share, and the company says it has applied to list on the Nasdaq Global Select Market under the ticker CBRS. At the top of the range, the deal would raise about $3.5 billion before expenses and put Cerebras near a $26.6 billion market value, according to Reuters' May 4 report and TechCrunch's read of the same filing.

That makes Cerebras one of the most important AI infrastructure listings of 2026, but it also makes the due diligence harder. The company has real technology, real customers and real revenue growth. It also has customer concentration, unusual financing tied to OpenAI, export-control exposure and a profit line that looks better on the surface than the operating business underneath.

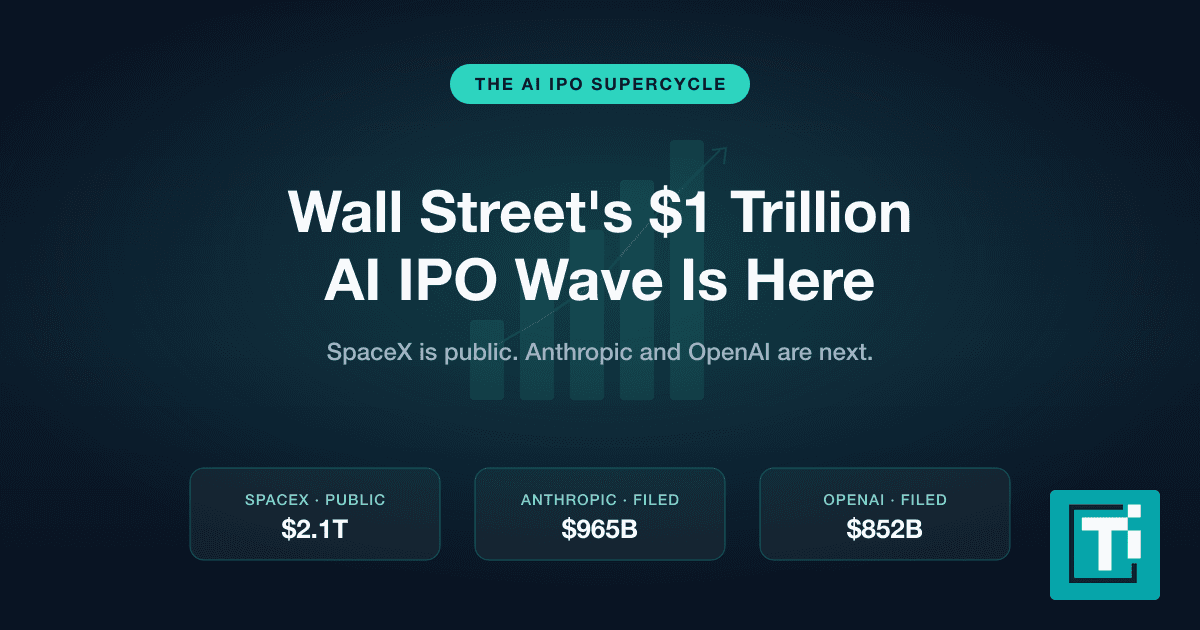

For TECHi readers already tracking the AI silicon race through AMD vs. Nvidia and the new AMD data-center earnings cycle, Cerebras is the public-market test of a different question: can a wafer-scale AI system become a serious investable platform, or is this IPO being priced like a perfect outcome before the proof is fully in?

The May 2026 IPO terms

Cerebras' May 4 preliminary prospectus says the company is offering 28 million Class A shares and expects the IPO price to land between $115 and $125 per share. The company also plans to grant underwriters a 30-day option to buy up to 4.2 million additional shares, a standard over-allotment structure that could increase the total number of shares sold if demand is strong.

The midpoint matters because it gives investors a cleaner way to size the deal. Cerebras estimates net proceeds of about $3.24 billion at a $120 midpoint after underwriting discounts, commissions and offering expenses, or about $3.73 billion if the underwriters exercise the option in full. The company says it plans to use the proceeds for general corporate purposes, including working capital, operating expenses and capital expenditures, with about $230 million earmarked for tax withholding and remittance obligations tied to RSU settlement.

The banking group is large enough to signal a serious institutional book. Cerebras named Morgan Stanley, Citigroup, Barclays and UBS Investment Bank as lead book-running managers, with Mizuho and TD Cowen as bookrunners and a longer list of co-managers. That does not make the deal low risk, but it does mean this is not a quiet niche listing.

The registration statement is still preliminary. Cerebras' own IPO release says the registration statement has been filed but is not yet effective, and the SEC's investor bulletin on IPOs reminds investors that SEC effectiveness is not an endorsement of the company or the investment merits. Until the offering is declared effective and priced, CBRS is not a normal public stock that retail investors can buy on the open market.

Why this is Cerebras' second attempt

Cerebras first filed to go public in 2024, but the IPO became tied up in national-security scrutiny around Abu Dhabi-based G42. In the original 2024 S-1, Cerebras disclosed that G42 represented $119.1 million of revenue in the first half of 2024, or 87% of total revenue for that period. That concentration made the IPO story about more than chips; it made it about customer dependency, export controls and geopolitical risk.

TechCrunch reported in April 2026 that Cerebras' earlier IPO plan was delayed by a federal review of the Abu Dhabi-based G42 investment and was ultimately withdrawn. The new May 2026 filing does not erase that history, but it changes the center of gravity by putting OpenAI and AWS at the front of the growth story.

The updated prospectus still shows that concentration risk is not gone. Cerebras says G42 accounted for 24% of 2025 revenue and 85% of 2024 revenue, while Mohamed bin Zayed University of Artificial Intelligence accounted for 62% of 2025 revenue. It also says OpenAI, G42, MBZUAI and AWS are significant customers or expected future customers whose negative demand changes could harm the business.

That is the first key point for investors: Cerebras has improved the story, but it has not turned into a diversified chip company overnight.

What Cerebras actually sells

Cerebras is not trying to build a slightly cheaper GPU. Its pitch is architectural. The company builds wafer-scale AI systems around the Wafer Scale Engine, a processor that keeps far more compute, memory and bandwidth on one very large piece of silicon instead of distributing work across many smaller chips.

The current flagship is WSE-3. Cerebras says WSE-3 has 4 trillion transistors, 900,000 AI-optimized cores, 44GB of on-chip SRAM and 125 petaflops of peak AI performance, and that the 5nm chip powers the CS-3 AI supercomputer. The same company release says CS-3 systems can be clustered up to 2,048 nodes and train models up to 24 trillion parameters.

That technical pitch matters because the AI market is splitting into workloads. Training frontier models is one market. Low-latency inference is another. Agentic coding, long reasoning, search and enterprise assistants often depend less on one benchmark score and more on how quickly a system can produce useful tokens back to the user. OpenAI makes that point directly in its Cerebras partnership announcement, saying low-latency compute can make AI responses faster and more natural across code, agents and other workloads.

Cerebras is therefore not just selling "anti-Nvidia" sentiment. It is selling a specialized system for customers that need speed, latency and token throughput. That is why the stock, if the IPO prices, should be analyzed beside Nvidia's broader AI platform rather than as a simple one-for-one replacement.

OpenAI is the center of the story

The biggest reason the 2026 IPO looks different from the 2024 attempt is OpenAI. In January, OpenAI said it was partnering with Cerebras to add 750MW of ultra-low-latency AI compute to its platform, with capacity coming online in multiple tranches through 2028. Cerebras' prospectus goes further, describing a multi-year OpenAI deal valued at more than $20 billion and saying the companies agreed to co-design future models for future Cerebras hardware.

That is powerful validation, but it also creates real dependency. The May S-1 says the Master Relationship Agreement with OpenAI represents a substantial portion of projected revenue over the next several years. It also says Cerebras must deliver capacity tranches across specified numbers of data centers and minimum capacity thresholds, and that OpenAI can terminate part or all of the agreement if Cerebras misses certain delivery or service obligations.

The financing around OpenAI is just as important. Cerebras disclosed a $1.0 billion working-capital loan from OpenAI that is tied to accelerating services, technology, manufacturing and buildout under the MRA. The filing also describes an OpenAI warrant covering 33,445,026 shares of Class N common stock at a $0.00001 exercise price, subject to vesting conditions.

That setup gives public investors both upside and risk. If Cerebras delivers, OpenAI could be the anchor customer that turns wafer-scale inference into a large cloud business. If Cerebras misses delivery milestones, the same agreement can become a pressure point.

AWS gives Cerebras a second hyperscaler channel

The AWS relationship is the second reason the IPO is more credible than it looked a year ago. AWS announced in March 2026 that it would deploy a Trainium plus Cerebras CS-3 solution in AWS data centers and make it available through Amazon Bedrock. The system pairs Trainium for prompt processing, or prefill, with Cerebras CS-3 for output generation, or decode.

Cerebras' own AWS blog post says AWS is deploying CS-3 systems in AWS data centers and that the collaboration targets 5x more high-speed token capacity in the same hardware footprint. The post also says the service will support leading open-source LLMs and Amazon Nova models through Bedrock.

The S-1 adds the investment angle. Cerebras says the AWS term sheet is binding with respect to pricing, exclusivity, minimum capacity and certain protections, and that it includes a commitment to issue AWS a warrant to buy up to 2,696,678 shares of Class N common stock at $100 per share if vesting conditions are met.

For investors, AWS lowers one fear and raises another. It lowers the fear that Cerebras is only an OpenAI/G42 story. It raises the execution bar because hyperscaler deployment is unforgiving: uptime, security, networking, capacity planning and customer support all become part of the investment case.

The financials: fast growth, messy profit

Cerebras' growth is real. The May 2026 S-1 says revenue increased from $24.6 million in 2022 to $78.7 million in 2023, $290.3 million in 2024 and $510.0 million in 2025. For 2025, the filing breaks that $509.991 million of total revenue into $358.440 million of hardware revenue and $151.551 million of cloud and other services revenue.

The surface profitability number is also real, but it needs context. Cerebras reported GAAP net income of $237.827 million in 2025 versus a net loss of $481.602 million in 2024. However, the same filing shows a GAAP operating loss of $145.862 million in 2025 and a non-GAAP net loss of $75.7 million after excluding stock-based compensation and a change in fair value or extinguishment of a forward contract liability.

That is why the best read is not "Cerebras is cleanly profitable." The better read is that Cerebras has crossed into meaningful revenue scale, while the core operating model is still being built. Tom's Hardware made the same point in its April filing analysis, noting that much of the GAAP profit reflected a non-operating accounting gain rather than the underlying hardware and cloud business.

Gross profit improved, but the cost base is still heavy. The filing shows 2025 gross profit of $199.071 million on $509.991 million of revenue, while research and development expense alone was $243.319 million. That mix is normal for a company still scaling a hard semiconductor platform, but it means investors should watch gross margin, data-center costs and R&D intensity after the IPO rather than focusing only on headline revenue growth.

Valuation: big, but lower than the hype

At the high end of the $115 to $125 range, Reuters said Cerebras is seeking a valuation of about $26.6 billion. Using the 2025 revenue figure from the S-1, that headline value is roughly 52 times trailing sales before adjusting for IPO cash and share-class details.

That is expensive in any normal market. The defense is that Cerebras is not being valued like a normal chip supplier; it is being valued as scarce AI infrastructure. TechCrunch noted that the range would be above Cerebras' February $23 billion private valuation, while Cerebras' own Series H release says the company raised $1 billion at an approximately $23 billion post-money valuation.

There is also a moderation argument. The Next Web framed the May 4 range as more grounded than the roughly $40 billion valuation that had circulated before the updated terms. That does not make $26.6 billion cheap, but it does make the IPO less detached from the most recent private round.

The right comparison is not a single multiple. Cerebras is being priced against three things at once: Nvidia's AI dominance, AMD's renewed data-center momentum and the hyperscaler desire for alternative inference platforms. That is why TECHi's AMD Q1 2026 earnings analysis matters for this IPO: public investors are rewarding real AI data-center revenue, but they are also punishing any sign that future growth is already fully priced in.

The risks investors should not ignore

The first risk is customer concentration. Cerebras' S-1 says G42 and MBZUAI together drove a large majority of 2025 revenue, and OpenAI is expected to represent a substantial portion of projected revenue over the next several years. Concentration can be good when customers are growing fast, but it can punish a stock quickly if one customer pauses, renegotiates, misses payments or shifts workloads to a competitor.

The second risk is execution. Cerebras must expand manufacturing, supply chain, data-center capacity and cloud operations while meeting OpenAI and AWS obligations. The S-1 warns that failing to deliver capacity under the OpenAI MRA could give OpenAI termination rights and could create repayment pressure around the working-capital loan.

The third risk is export control. Cerebras says it has obtained export licenses for CS-2, CS-3 and future CS-4 systems for G42 and MBZUAI in the UAE, but the same risk section says those licenses carry rigorous security and compliance obligations and could be revoked if conditions are not met. That matters because the earlier IPO delay already showed how quickly national-security review can change the investment timeline.

The fourth risk is valuation. A $26.6 billion headline value gives Cerebras credit for becoming a durable AI infrastructure platform before public investors have seen quarterly reporting as a listed company. This is why the post-IPO setup should be judged against delivery milestones, not only first-day trading.

The fifth risk is governance and dilution. The S-1 describes multiple classes of common stock, large option and RSU pools, the OpenAI warrant, the AWS warrant and additional Class N common stock mechanics. The SEC's IPO investor bulletin specifically tells investors to review prospectus sections on share classes, market overhang and risk factors because new public companies can have structures that limit public-shareholder influence.

How investors can approach the Cerebras IPO

Retail investors have three practical paths. The first is to request an IPO allocation through a broker involved in the syndicate, but the SEC says IPO allocations often go to institutional and high-net-worth clients, especially for high-demand deals. The second is to wait until CBRS begins trading on Nasdaq and buy in the open market. The third is to avoid the first-day volatility and wait for the first earnings report as a public company.

For most investors, the third path may be the cleanest. The May filing gives enough information to build a watchlist thesis, but it does not yet give public-market evidence of how Cerebras behaves quarter to quarter. The company will need to show revenue conversion from OpenAI, a real AWS launch through Bedrock, improving gross margin, manageable capex and a broader customer base.

If the stock prices above range and opens far above the IPO price, the risk/reward changes immediately. If it prices inside the range and trades calmly, long-term investors may get more time to analyze the operating model. Either way, the right question is not "Is Cerebras exciting?" It is whether the public price already assumes too much of the OpenAI and AWS future.

What to watch next

The first item is the final IPO price. A price above $125 would signal heavy demand and a higher starting valuation; a price at or below the range would signal more discipline or weaker book strength.

The second item is OpenAI capacity delivery. OpenAI said 750MW of low-latency capacity will come online through 2028, while Cerebras' filing ties the MRA to delivery tranches and service obligations. Watch for any disclosure about data-center readiness, capacity acceptance and the pace at which OpenAI workloads move onto Cerebras.

The third item is AWS availability. AWS said the Cerebras solution would be deployed in AWS data centers and accessed through Amazon Bedrock, and Cerebras said AWS will be its channel to a larger enterprise customer base. Investors should look for commercial availability, model coverage, pricing and customer adoption.

The fourth item is gross margin. Cerebras' 2025 revenue growth is impressive, but the business still showed a GAAP operating loss. A durable IPO story needs revenue growth that improves unit economics, not revenue growth that requires permanently heavy losses.

The fifth item is customer mix. If G42, MBZUAI and OpenAI remain overwhelmingly dominant, the stock deserves a concentration discount. If AWS and a broader enterprise base become visible, Cerebras can argue for a stronger platform multiple.

Bottom line

Cerebras is one of the rare AI IPOs with substance behind the hype. It has a differentiated wafer-scale architecture, 2025 revenue of about $510 million, an OpenAI partnership tied to 750MW of low-latency compute, an AWS Bedrock path to enterprise distribution and a May 2026 IPO range that could raise roughly $3.5 billion at the high end.

But the risks are just as real. The company is still concentrated in a few giant customers, its GAAP profit was helped by non-operating accounting effects, its core business had an operating loss in 2025, and the valuation already prices in a large share of future success. Cerebras may be the most interesting AI infrastructure IPO on the board, but interesting is not the same as automatically attractive at any price.

The right investor stance is disciplined curiosity. Read the prospectus, respect the OpenAI and AWS validation, watch the final pricing, and wait for evidence that Cerebras can turn its enormous backlog and technical speed into repeatable public-company earnings.

Investment disclaimer: This article is for informational and educational purposes only. It is not financial advice or a recommendation to buy, sell or hold any security. IPOs can be speculative, volatile and difficult to allocate fairly; investors should read the latest prospectus, verify offering terms and consult a licensed financial advisor before making investment decisions.

FAQ

Frequently asked questions

When is the Cerebras IPO?

As of May 6, 2026, Cerebras has launched its IPO roadshow and filed an amended S-1/A, but CBRS will not trade publicly until the registration statement becomes effective and the offering is priced.

What is the Cerebras IPO price range?

The May 2026 filing sets an expected range of $115 to $125 per Class A share for 28 million shares, with an additional 4.2 million-share underwriter option.

What ticker will Cerebras use?

Cerebras has applied to list on the Nasdaq Global Select Market under the ticker symbol CBRS.

What valuation is Cerebras targeting?

At the high end of the marketed range, Reuters and other market reports put the implied valuation near $26.6 billion.

How much revenue did Cerebras report in 2025?

Cerebras reported about $510 million of 2025 revenue in its May 2026 S-1/A, up from about $290 million in 2024.

Is Cerebras profitable?

Cerebras reported GAAP net income in 2025, but the filing also shows a GAAP operating loss and a non-GAAP net loss after excluding stock-based compensation and a forward-contract liability effect.

Should retail investors buy Cerebras IPO stock?

This article does not make buy or sell recommendations. Investors should read the latest prospectus, watch final pricing, and weigh OpenAI/AWS upside against customer concentration, valuation and execution risk.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Omer Sheikh covers Elon Musk-led and Musk-adjacent companies for TECHi, with a focus on Tesla, xAI, SpaceX, X, Neuralink, The Boring Company, and the public-market read-throughs from their product cycles, capital needs, AI infrastructure plans, supply chains, and regulatory risk. He also follows MicroStrategy/Strategy and its Bitcoin treasury strategy, using his finance background to connect balance-sheet decisions, capital markets, valuation, catalysts, and downside risk. His work is built for readers who want the investment case behind the headline: what changed, what it means for cash flow or market value, and what would prove the thesis wrong.