Intel's Apple spike is not really a nostalgia trade. It is not a simple bet that Apple is about to abandon TSMC. It is a market test of whether Intel Foundry is finally becoming investable as an external manufacturing platform. The trigger was a Wall Street Journal report that Apple and Intel have reached a preliminary chip-making agreement, following Bloomberg's earlier report that Apple had been exploring Intel and Samsung as possible U.S.-based manufacturers for main device processors.

At Friday's close, TECHi's quote endpoint showed INTC at $124.92, up 13.96%, with an intraday high of $130.57. Apple closed at $293.32, up 2.05%, while TSM's U.S.-listed ADR slipped 0.60%. The price action makes sense only if investors view Apple as a possible anchor customer, not merely another headline customer logo.

- The real catalystThe reported Apple agreement matters because Intel has explicitly said advanced-node economics need external foundry volume beyond its own products.

- What is not provenNo public disclosure yet gives product lines, wafer volumes, pricing, margins, or a shipment timetable.

- Investor lensThe rally prices Intel as a strategic U.S. foundry option, while analyst targets still lag the stock's new level.

- Apple angleApple gains supply-chain optionality without necessarily weakening TSMC as its main advanced-node partner.

- TECHi verdictConstructive on strategic validation, cautious on valuation until the agreement becomes disclosed economics.

What Actually Changed

The public record has two layers. First, Bloomberg reported that Apple had held exploratory discussions with Intel and Samsung about building main processors in the U.S. A Reuters recap of the Bloomberg report said Apple had concerns about non-TSMC technology, including reliability and scale, and that neither the Intel nor Samsung effort had resulted in orders at that stage.

The newer WSJ report is more important for the stock because it describes a preliminary agreement rather than only exploratory talks. That distinction changes the framing. Exploratory discussions are optionality. A preliminary agreement, if confirmed and converted into production commitments, is a signal that Apple is willing to spend real engineering time qualifying Intel's process technology for at least some part of its device silicon roadmap.

That still leaves the most important questions unanswered. The report trail does not establish which Apple chips Intel would manufacture, how much volume would move, whether the work involves 18A, 18A-P, 14A, packaging, or a lower-risk component, and whether any commercial product will ship before 2027 or 2028. Those details decide whether this is a symbolic supply-chain hedge or a material foundry win.

Why The Stock Reacted Like This

The market is reacting because Intel's foundry problem has never been only about fabs. It has been about trust, yield, customer confidence, and fixed-cost absorption. Intel's own filing language makes the issue unusually direct: the company said in its 2025 Form 10-K that leading-edge process technology requires substantial capital investment and that its cost structure needs manufacturing volumes beyond Intel's own products to reach economic efficiency.

That same filing warned that if Intel cannot secure a significant external foundry customer for Intel 14A and meet customer milestones, it may pause or discontinue 14A and successor leading-edge nodes. That is the line investors should keep in front of them. Apple is not valuable to Intel merely because Apple sells devices. Apple is valuable because Apple qualification would tell other large chip designers that Intel is not just asking the market to trust a turnaround story.

This is why the move is bigger than a normal customer rumor. A credible Apple track could lower perceived execution risk, improve Intel's negotiating posture with future foundry customers, and support a higher valuation multiple on assets that otherwise look heavy, expensive and underutilized. For context, TECHi's earlier Intel stock analysis framed the turnaround around foundry credibility, not only PC recovery.

Apple's Incentive Is Optionality, Not A TSMC Divorce

Apple already has a U.S. manufacturing narrative. In February, the company said it would expand Houston operations for Mac mini production and AI server assembly, and that it was on track in 2026 to buy well over 100 million advanced chips from TSMC's Arizona facility. That matters because the Intel story is not happening in isolation. It fits into a broader Apple push to localize more of its supply chain while keeping access to the best process technology available.

For Apple, a second foundry option can be valuable even if TSMC remains the main partner. TSMC capacity is pulled by iPhone, Mac, AI accelerator, networking and high-performance computing demand. If Apple can qualify Intel for selected chips, it may gain bargaining leverage, geographic resilience, and a U.S. political answer without taking unnecessary risk on the most sensitive flagship silicon.

For TSMC, the immediate read-through is more nuanced than negative. Apple is still deeply tied to TSMC's advanced manufacturing ecosystem, and TECHi's TSMC stock outlook has repeatedly centered on AI-era capacity scarcity. The Intel report suggests Apple wants another lane, not that the leading lane has stopped mattering.

The Valuation Problem After A 15% Move

The hard part for investors is that the stock has already moved faster than the disclosed economics. StockAnalysis lists a Hold consensus on Intel, an average price target of $65.44, and a high target of $118 among 32 covering analysts. Intel closed above that high target on Friday. That does not make the rally wrong, but it does mean the stock is trading on strategic optionality that many published models have not yet incorporated.

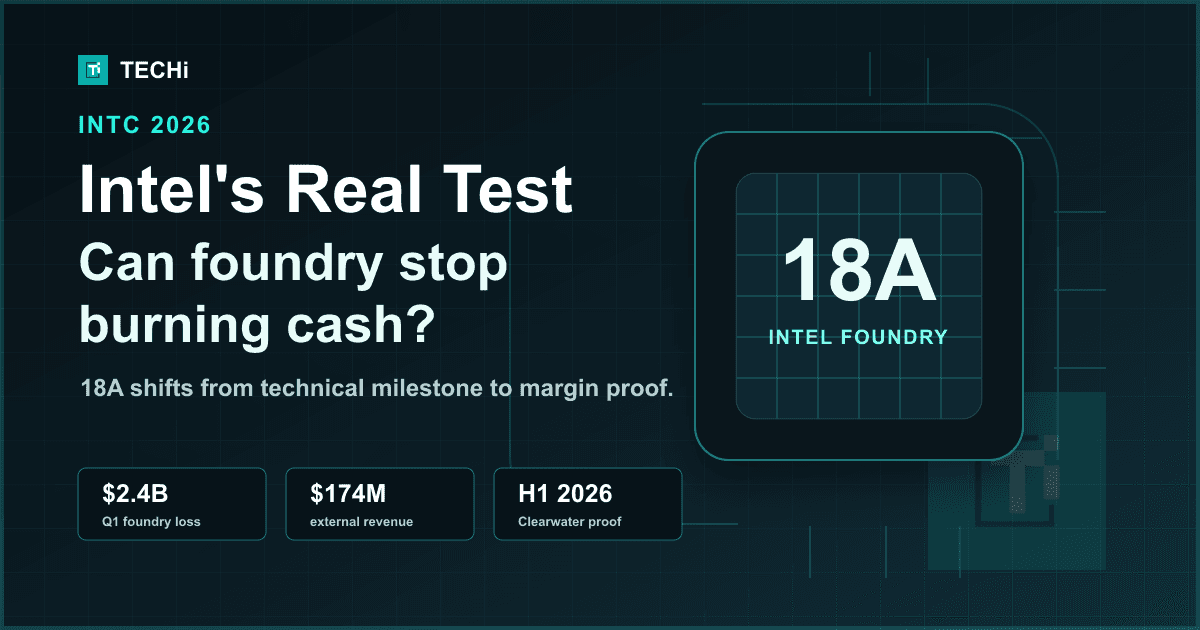

Intel's first-quarter results show both sides of the case. The company reported Q1 2026 revenue of $13.6 billion, up 7% year over year, with Intel Foundry revenue of $5.4 billion, up 16%. But the foundry segment still posted a $2.437 billion operating loss in the quarter. A major customer helps the narrative, but it has to become volume, pricing discipline and yield improvement before it solves the income statement.

That is the line between a good trade and a good investment. The Apple report can justify a higher probability that Intel's foundry survives as a strategic platform. It cannot, by itself, justify treating every future wafer as profitable revenue.

The Risks Still Matter

Risk one is confirmation risk. Apple and Intel have not issued a detailed public announcement with product scope, volume, node, or timing. Until they do, investors are still underwriting a report-driven thesis.

Risk two is execution risk. Apple can qualify a second supplier and still keep the most performance-sensitive silicon at TSMC. Qualification work is not the same as margin-accretive production.

Risk three is valuation risk. Intel's stock has been rewarded as if a strategic customer changes the probability tree. That may be correct, but the current price demands evidence that foundry losses can narrow and that future external customers will not require uneconomic pricing.

Risk four is TSMC comparison risk. Intel is being judged against the world's most trusted foundry at a time when AI-chip demand keeps TSMC capacity scarce. Even a strong Intel win may start with non-flagship or lower-volume chips, not the most valuable Apple processors.

TECHi Verdict

The right read is cautiously constructive. Intel's rally is not irrational if Apple becomes the first customer that proves Intel Foundry can compete for serious external work. It is also not fully de-risked. A preliminary agreement is not the same as disclosed wafer economics, and a 15% stock move compresses the margin of safety for investors who are arriving after the headline.

For existing Intel bulls, the Apple report strengthens the thesis that the foundry turnaround is moving from story to customer validation. For new buyers, the cleaner entry point may depend on the next disclosures: product line, node, first shipment window, gross-margin impact and whether other large chip designers follow. Until then, this is an option premium on Intel's U.S. foundry future.

The bigger market implication is that Apple may have just turned Intel into the test case for a new U.S. semiconductor supply chain. If Intel can convert that test into profitable production, the May 8 rally will look less like a spike and more like the first repricing of a foundry asset the market had nearly written off.

FAQ

Frequently asked questions

Why did Intel stock surge after the Apple report?

Intel rallied because investors read the reported Apple agreement as potential validation for Intel Foundry, especially after Intel said external customers are needed to justify advanced-node economics.

Has Apple confirmed that Intel will make iPhone chips?

As of this draft, Apple and Intel had not publicly disclosed detailed product scope, wafer volumes, node selection or shipment timing. The report should be treated as preliminary until formal details emerge.

Does this mean Apple is leaving TSMC?

No. Apple already plans to buy well over 100 million chips from TSMC's Arizona facility in 2026, and TSMC remains central to Apple's advanced silicon supply chain.

What is the biggest risk for Intel investors after the rally?

The biggest risk is that the stock has moved ahead of disclosed economics. Investors still need evidence on yields, pricing, margins and actual production volume.

Is the Intel Apple chip deal good for AAPL stock?

For Apple, the potential benefit is supply-chain optionality and U.S. manufacturing leverage, not necessarily near-term earnings accretion. The financial impact depends on product scope and execution.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Muhammad Zeshan Sarwar covers mobile technology, consumer electronics, and the intersection of crypto with mainstream products. He reviews phones and wearables against their shipping firmware rather than launch-day marketing, and tracks the crypto-in-app integrations Apple and Google actually allow on their platforms. His reporting spans hardware launches, iOS and Android ecosystem shifts, and the wallet and payments layer bridging both.