- The real testAmazon's 2026 stock debate is now about cash conversion: can AWS, ads and external logistics fund the AI infrastructure bill?

- The capex pressureFree cash flow fell to $1.2 billion for the trailing twelve months even as operating cash flow rose, because property and equipment spending surged around AI.

- The logistics wedgeAmazon Supply Chain Services turns the company's freight, distribution, fulfillment and parcel network into a service for businesses beyond the Amazon marketplace.

- The bull caseIf logistics follows the AWS playbook, Amazon gets another infrastructure business with high utilization, better asset turns and more operating leverage.

- The riskIf outside logistics demand is slower than AI capex, AMZN remains dependent on AWS and advertising to carry the valuation.

Amazon stock is no longer getting valued on a clean cloud-plus-commerce story. The company is now asking investors to underwrite two infrastructure businesses at once: the AI data-center buildout inside AWS and a physical logistics network that Amazon has just opened to outside businesses.

That is the real 2026 test for AMZN. At 12:25 p.m. ET on May 8, 2026, TECHi's Alpaca IEX snapshot showed Amazon trading at $273.11, up about 0.75% from the prior IEX close while U.S. equities were open. The move is not the important part. The important part is whether the stock deserves to keep expanding while free cash flow is being absorbed by AI infrastructure.

The headline question is deliberately narrow: can logistics help pay for the AI capex boom? AWS and advertising are already proven cash engines. Logistics is the new variable. If Amazon can turn its delivery, fulfillment and freight infrastructure into a paid external platform, the company gets another way to raise utilization on assets it already had to build for retail. If not, the stock remains much more dependent on AWS growth and advertising margins to fund a spending cycle that is getting larger, not smaller.

Amazon's Q1 looked strong until free cash flow entered the room

Amazon's first-quarter headline numbers were hard to dismiss. In its Q1 2026 earnings release, the company reported net sales up 17% to $181.5 billion, AWS revenue up 28% to $37.6 billion, and operating income up to $23.9 billion from $18.4 billion a year earlier. North America operating income improved to $8.3 billion, international operating income reached $1.4 billion, and AWS operating income rose to $14.2 billion.

Those figures explain why investors still want to own the stock. Amazon has the rare mega-cap profile where retail scale, cloud growth, advertising monetization and custom silicon can all improve the same income statement. TECHi's broader Amazon stock analysis has covered that premium-multiple logic: investors are not paying for an online store; they are paying for operating leverage across a stack of infrastructure businesses.

The problem is that free cash flow told a different story. Amazon said trailing-twelve-month operating cash flow rose 30% to $148.5 billion, but free cash flow fell to $1.2 billion from $25.9 billion a year earlier. The company attributed that drop primarily to a $59.3 billion year-over-year increase in property and equipment purchases, net of sales and incentives, mainly reflecting investments in artificial intelligence.

That one line reframes the stock. Amazon is growing, margins are expanding, AWS is accelerating, and advertising is now above a $70 billion trailing-twelve-month revenue run rate. Yet almost all of the operating cash flow is being pulled back into infrastructure. For a company with Amazon's history, that is not automatically bad. It is, however, the number that decides whether the 2026 rally is built on cash returns or deferred cash returns.

AWS is funding the future, but also demanding the bill

AWS remains the strongest pillar in the AMZN thesis because it is both the source of AI demand and the place where AI capex shows up first. The Q1 release said AWS posted its fastest growth in 15 quarters, and Amazon highlighted a custom chips business that exceeded a $20 billion annual revenue run rate across Graviton, Trainium and Nitro.

The customer list also gives the spending credibility. Amazon said OpenAI committed to consume roughly two gigawatts of Trainium capacity beginning in 2027, Anthropic would secure up to five gigawatts of current and future Trainium chips, and AWS landed more than 2.1 million AI chips over the prior 12 months, more than half of them Trainium. The same release said Amazon plans to deploy more than one million NVIDIA GPUs starting in 2026.

That is why the capex cannot be treated as a normal margin headwind. It is also booked demand, strategic positioning and competitive defense against Microsoft Azure, Google Cloud and specialized AI infrastructure providers. TECHi's coverage of OpenAI's AWS deal and DeepSeek-R1 on Amazon Bedrock shows how fast AWS has been trying to change the AI narrative from follower to full-stack provider.

The risk is sequencing. Customers may commit to compute before the capacity reaches mature utilization. Training clusters, power, data centers, chips and networking arrive before all revenue is recognized. That creates a cash-flow valley even if the strategic direction is right.

Investors should not ask whether AWS AI capex is useful. The better question is whether the returns arrive quickly enough to prevent the rest of Amazon from subsidizing an unusually heavy buildout for too long.

Logistics is the new cash-flow option

This is where Amazon Supply Chain Services changes the AMZN conversation. On May 4, Amazon launched Amazon Supply Chain Services, opening its freight, distribution, fulfillment and parcel shipping solutions to businesses of all sizes. The company said the offering gives outside businesses access to the same logistics capabilities that supported Amazon's own retail operations and independent sellers.

This is not a small feature launch. Amazon said Procter & Gamble, 3M, Lands' End and American Eagle Outfitters were among early customers using different pieces of the network. It also disclosed a freight network with more than 80,000 trailers, more than 24,000 intermodal containers and more than 100 aircraft. The parcel-shipping piece includes two-to-five-day delivery speeds, seven-day-a-week service and shipment visibility features such as photo-on-delivery.

TECHi already covered the market shock from Amazon opening its logistics empire. For the stock, the deeper question is not whether FedEx or UPS feel pressure. The deeper question is whether Amazon can use third-party volume to improve the economics of a network it already had to operate.

That is the AWS analogy, but with a caveat. AWS converted internal infrastructure into an external business with software-like margins and very high incremental economics. Logistics is more physical, more labor-intensive, more exposed to fuel, routing, claims, labor availability and peak-season volatility. The return profile will not look like cloud. But the utilization logic can rhyme: when fixed assets are already built, third-party demand can raise asset turns and reduce per-unit cost.

The market reaction shows why this is more than a side business

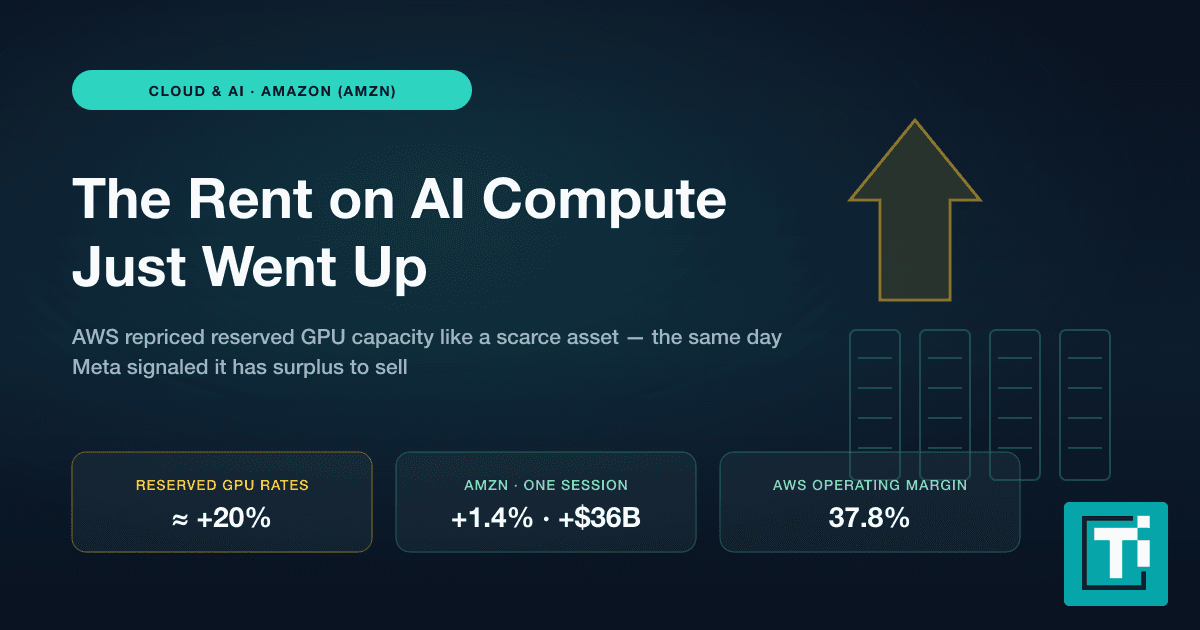

Axios described Amazon's logistics push as a move against the broader supply-chain market, noting that Amazon is offering distribution, parcel shipping and fulfillment services to outside businesses rather than only marketplace sellers. Axios also reported that FedEx, UPS and GXO shares fell after Amazon's announcement, while Amazon shares rose 1.4%.

The logistics incumbents did not move because investors suddenly believed Amazon would replace them overnight. They moved because Amazon has density, data and customer-demand visibility that few logistics companies can match. Axios cited Pitney Bowes data showing Amazon was just behind USPS in U.S. parcels handled in 2024 and projected to become No. 1 by 2028.

This matters for AMZN because logistics has historically been treated as a cost center inside retail. Amazon spent years building speed, fulfillment capacity, last-mile reach and inventory placement. Opening that capacity to outside businesses gives investors a different lens: the network can be viewed as a platform, not only an expense.

That platform lens does not guarantee margins. Third-party logistics is competitive, and pricing power may be limited in lanes where FedEx, UPS, regional carriers, freight brokers and third-party logistics providers already operate. But Amazon does not need to win the entire market for the thesis to matter. It needs enough profitable external volume to make the retail logistics base more efficient and less seasonal.

Advertising is the bridge investors should not ignore

AWS gets the AI headlines and logistics gets the May 2026 news hook, but advertising may be the cleaner near-term bridge. Amazon said advertising grew to more than $70 billion in trailing-twelve-month revenue. That business has a different capital profile than logistics and data centers: it monetizes demand already moving through Amazon's retail and media ecosystem.

For AMZN shareholders, ads are important because they help separate revenue growth from physical fulfillment costs. A sponsored product ad, streaming ad, or retail media placement does not require Amazon to build a new fulfillment center. It uses first-party commerce intent and placement inventory. That can help offset the cash pressure from the AI buildout even if logistics takes time to mature.

The strategic map is becoming clearer. AWS funds AI infrastructure because customers want compute. Advertising monetizes the customer and seller base. Logistics tries to monetize the physical network. Retail supplies the demand density that makes the whole system harder to replicate.

The stock gets interesting when all four work together. Retail creates volume. Logistics raises utilization. Ads monetize commerce attention. AWS monetizes compute and AI demand. The danger is that capex arrives faster than all four layers can compound.

Valuation now depends on proof, not just optionality

Amazon still has analyst support. S&P Global's pre-Q1 analysis, citing Visible Alpha consensus, put the 2027 consensus P/E at 26x and the target price at $285. That target is not wildly above the May 8 trading level, which matters because the stock has already absorbed a large amount of confidence in AWS, ads and AI infrastructure.

A 26x 2027 earnings multiple can be reasonable for Amazon if the company is converting capex into durable growth. It becomes less comfortable if free cash flow stays close to zero while the investment cycle keeps expanding. This is the same issue now running through the entire AI market: investors are willing to fund the buildout, but they increasingly want evidence that the spending is creating measurable returns. TECHi's broader analysis of AI capex carrying U.S. growth explains why this is no longer only an Amazon problem.

For Amazon specifically, valuation proof should come from four places.

First, AWS needs to keep growing without a margin collapse. The company can accept lower near-term cash conversion if revenue visibility and utilization improve.

Second, advertising needs to keep compounding because it is one of Amazon's least capital-hungry revenue streams.

Third, Supply Chain Services needs to show that external logistics demand is real, not just a press-release extension of internal capabilities.

Fourth, management needs to show that property and equipment spending is peaking or at least becoming more predictable. The market can handle heavy capex when the return path is visible. It struggles when the spending curve keeps moving higher without equally clear cash-flow timing.

What would make the logistics thesis real

The first proof point is customer breadth. Early logos are useful, especially Procter & Gamble, 3M, Lands' End and American Eagle. But AMZN investors should look for evidence that the customer base expands beyond headline brands into recurring, multi-year logistics relationships.

The second proof point is utilization. Amazon does not need to disclose every lane-level metric, but investors need signs that third-party freight, distribution and parcel volume are raising network efficiency rather than adding complexity.

The third proof point is gross-margin behavior inside retail and services. If logistics externalization is working, Amazon should eventually show better fulfillment cost absorption, even if management does not isolate Supply Chain Services as a segment.

The fourth proof point is competitive reaction. FedEx and UPS can respond on price, service tiers, merchant relationships and bundled offerings. If Amazon wins share only by underpricing incumbents, the cash-flow benefit is weaker. If it wins because it offers better speed, integrated inventory placement and demand forecasting, the economics get more attractive.

The fifth proof point is whether Amazon can package logistics like software. The press release describes a centralized console for businesses to discover, select and sign up for ASCS solutions. That matters. The more self-serve and integrated the product becomes, the more it starts to look like a platform rather than a customized logistics contract.

The bottom line for AMZN

Amazon's 2026 setup is not a simple buy-or-avoid story. The operating business is strong. AWS is accelerating. Advertising is now a massive revenue stream. The balance sheet and cash generation remain large. The company has enough strategic assets to justify a premium multiple.

The issue is cash timing. Free cash flow is thin because Amazon is spending aggressively on AI infrastructure. Logistics may become the missing offset, but it is not proven yet. It needs time, utilization, pricing discipline and third-party demand beyond early adopters.

That is why the best AMZN question for the rest of 2026 is not whether Amazon is an AI winner. It probably is. The sharper question is whether Amazon can fund that AI win with enough cash from AWS, advertising and logistics to keep investors from treating the spending cycle as a drag on valuation.

If Supply Chain Services becomes an AWS-style externalization of internal infrastructure, the stock gets a new story: Amazon as cloud AI platform and physical supply-chain platform at the same time. If it stays small, Amazon still has AWS and ads, but the AI capex boom will keep eating the free-cash-flow narrative.

For now, Amazon stock deserves attention for the right reason. It is not just a retail comeback, not just an AWS acceleration story, and not just an AI capex story. It is a test of whether one of the world's largest infrastructure owners can turn more of its infrastructure into customer-facing revenue before the capex bill changes the way investors value the company.

FAQ

Frequently asked questions

What is Amazon stock's real 2026 test?

Amazon stock's real 2026 test is whether AWS, advertising and newly opened logistics services can generate enough cash to support the company's AI infrastructure spending cycle.

Why does AI capex matter for Amazon stock?

Amazon reported that free cash flow fell to $1.2 billion for the trailing twelve months as property and equipment purchases rose, primarily reflecting AI investments.

How big was AWS in Amazon's Q1 2026 results?

AWS segment sales increased 28% year over year to $37.6 billion in Q1 2026, according to Amazon's earnings release.

What is Amazon Supply Chain Services?

Amazon Supply Chain Services opens Amazon's freight, distribution, fulfillment and parcel shipping capabilities to outside businesses beyond the Amazon marketplace.

What should AMZN investors watch next?

Investors should watch AWS growth, advertising margin, free cash flow, AI infrastructure spending, and whether external logistics demand becomes material enough to support Amazon's capex cycle.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Muhammad Zeshan Sarwar covers mobile technology, consumer electronics, and the intersection of crypto with mainstream products. He reviews phones and wearables against their shipping firmware rather than launch-day marketing, and tracks the crypto-in-app integrations Apple and Google actually allow on their platforms. His reporting spans hardware launches, iOS and Android ecosystem shifts, and the wallet and payments layer bridging both.