- New frameSandisk's sharper AI thesis is not generic SSD demand; it is the retained data trail created by AI agents, RAG systems and enterprise workflows.

- Live setupSNDK traded near $1,468 at 10:50 a.m. ET on May 8, 2026 in TECHi's Alpaca/IEX snapshot.

- Contract signalLong-term supply agreements with commitments and prepayments could make NAND look more like reserved AI infrastructure capacity.

- HBF optionHigh Bandwidth Flash gives Sandisk a potential path closer to AI inference memory, though it remains an option rather than a proven revenue engine.

- Investor riskThe bear case is peak-cycle NAND: margins, pricing and customer commitments have to hold after the first AI storage surge.

Sandisk is no longer trading like a normal NAND recovery. At 10:50 a.m. Eastern on Friday, May 8, 2026, TECHi's Alpaca/IEX market snapshot showed SNDK near $1,468, up sharply from the prior close. The price action matters because investors are no longer only asking whether NAND pricing has turned. They are asking whether Sandisk has found a structural role inside the AI infrastructure buildout.

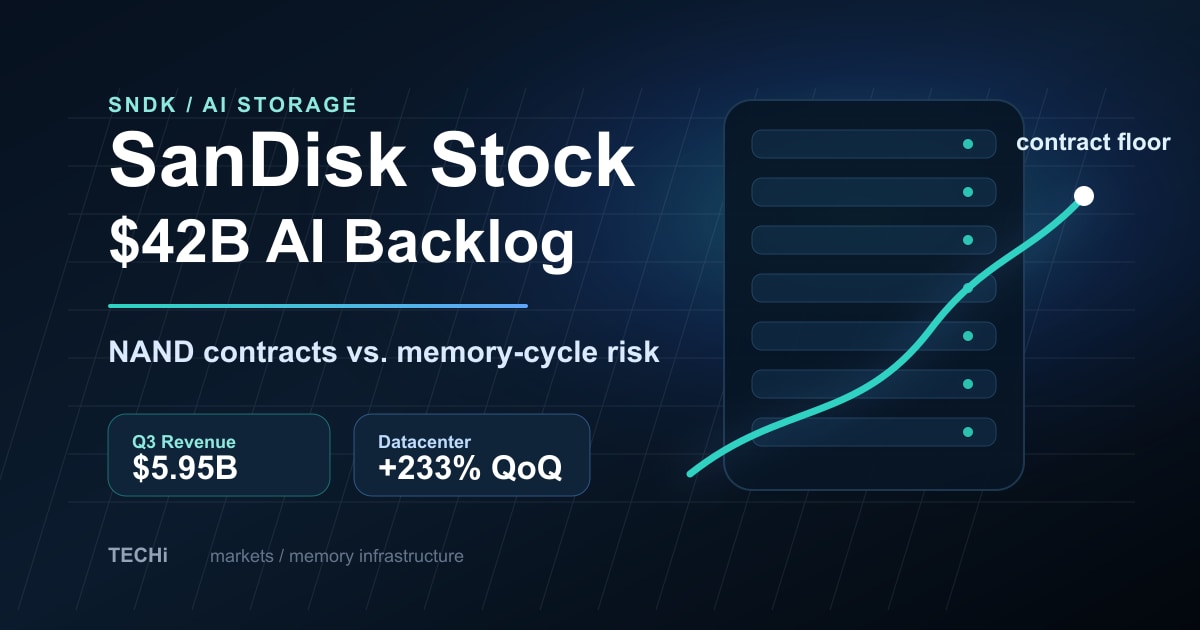

The usual read is straightforward: Sandisk reported fiscal third-quarter revenue of $5.95 billion, GAAP gross margin of 78.4%, data-center revenue up 233% sequentially, and Q4 revenue guidance of $7.75 billion to $8.25 billion. That is enough to explain why traders chased the stock. It is not enough to explain what could make the move durable.

A better frame is this: Sandisk is trying to become the storage toll booth for AI data exhaust.

AI agents do not just answer questions. They create memory. They keep logs. They write code, revise code, store context, index documents, generate synthetic datasets, preserve compliance trails and feed retrieval systems. The more enterprise AI shifts from chatbot demos to persistent workflows, the more storage becomes a recurring infrastructure requirement rather than a one-time hardware line item.

That is the part of the Sandisk story that still looks underpriced by the public debate. GPUs run the model. Power keeps the data center alive. Storage remembers what the AI system did.

The market already knows the quarter was huge

Sandisk's latest report gave bulls the easy evidence. The company did not merely beat a quarter; it showed operating leverage that looks extreme even by memory-cycle standards. The official release cited $5.95 billion of revenue, 78.4% GAAP gross margin and non-GAAP EPS of $14.15, while the Q4 outlook implied another step-up in revenue and earnings.

That is why the stock now sits inside the same AI-infrastructure conversation as Micron, Seagate, Western Digital and, at the far larger end of the stack, Nvidia. TECHi already covered the broader warning in Sandisk, Micron, AMD and AAOI showing the new risk in AI stocks: once investors pay extreme multiples for AI-adjacent capacity, the real question becomes whether demand is contractual, repeatable and hard to replace.

Sandisk's answer is not only price. It is commitment.

Reuters reported that Sandisk had signed five long-term supply agreements, including three worth $42 billion, with minimum purchase commitments and prepayments. That is the key difference between a commodity rally and a possible infrastructure re-rating. If customers are reserving NAND supply the way hyperscalers reserve power, GPUs and cloud capacity, Sandisk is no longer just selling flash into a cycle. It is selling certainty into an AI arms race.

The real product is memory for machine work

The phrase "data exhaust" can sound abstract, but it is practical. A single AI agent assigned to legal review, software maintenance or customer support can create a trail of prompts, intermediate steps, source documents, embeddings, tool calls, revised outputs and audit records. Multiply that by enterprise adoption and storage moves from background plumbing to cost center.

That is why the Sandisk setup is different from a classic PC or smartphone flash cycle. The old NAND question was mostly about unit shipments and pricing. The new AI question is about whether inference workloads create a long tail of retained data.

IDC's semiconductor outlook helps explain the size of the memory opportunity. The firm projected NAND market revenue of $174.1 billion in 2026 and tied semiconductor growth to AI infrastructure demand. Separately, IDC has argued that enterprise AI depends on fresh, connected data rather than static warehouses, warning that stale data can undermine AI outcomes in production systems.

That second point is where Sandisk becomes more than a cyclical NAND name. Retrieval-augmented generation, vector search and agent memory all require storage that is close enough, fast enough and cheap enough to support repeat lookups. IBM's new content-aware storage work for RAG is one sign of where the architecture is moving: StorageReview described IBM CAS as designed to let storage understand metadata and structure for retrieval-augmented generation workloads.

That does not mean Sandisk owns the entire RAG stack. It does not. Databases, file systems, storage software, networking and cloud orchestration all matter. The investable point is narrower: AI's memory layer is getting more valuable, and Sandisk sits in one of the hardware categories that can monetize the retained-data explosion.

Contracted NAND is the part investors should watch

The strongest Sandisk bull case is not simply that AI needs more flash. Everyone in the memory trade can make that argument. The stronger case is that customers may now be willing to sign capacity-style agreements because storage availability has become part of AI deployment planning.

That is exactly the question TECHi raised in its earlier Sandisk supercycle profile: has the spin-off turned a panic-priced NAND company into a capacity-rights business? The newest long-term agreements push that question from theory into the income statement.

If those commitments hold, Sandisk could smooth part of the boom-bust behavior that has historically punished memory stocks. The company would still be cyclical. NAND always has supply risk. But a backlog-like structure changes how investors think about downside, because it gives the market something closer to forward visibility.

That visibility also matters beside the power trade. TECHi's AI data-center power stock analysis focused on the grid bottleneck. Sandisk adds the next layer: after power and compute, the data center needs a memory architecture that can handle machine-generated work product at scale. It is a different bottleneck, but it points to the same market behavior. AI buyers are reserving scarce infrastructure before the shortage becomes obvious.

High Bandwidth Flash is the option inside the story

Sandisk's High Bandwidth Flash work is the speculative part, but it is not random. The company and SK hynix announced a collaboration to standardize HBF, describing it as a NAND-based memory technology aimed at meeting AI inference memory needs at scale. Sandisk later said it had formed an HBF technical advisory board to guide the technology's development and strategy.

The reason HBF matters is simple. HBM is the prestige memory product in the AI accelerator market, but capacity limits and cost can constrain inference economics. HBF is not guaranteed to displace HBM, and investors should not price it as if it already has. The relevant point is optionality: if AI inference needs larger pools of accessible memory, Sandisk has a path to move NAND closer to the accelerator discussion instead of staying in bulk storage alone.

That optionality connects Sandisk to the broader AI infrastructure chain. TECHi's AMD Q1 2026 earnings analysis showed how quickly data-center demand can change the story for a chipmaker. TECHi's Nvidia/OpenAI network catalyst piece showed that even the most valuable AI stack depends on less glamorous bottlenecks. Sandisk is the same idea from the storage side.

The bear case is not weak

The risk is that investors are confusing peak-cycle NAND economics with a permanently better business. A 78.4% GAAP gross margin is extraordinary. If supply expands too quickly, customers digest inventory, or AI storage demand proves lumpier than expected, margins can move the other way fast.

There is also ownership overhang. Western Digital's separation left residual stake dynamics, and Sandisk announced a secondary offering of 17 million shares by Western Digital in February 2026, noting that Sandisk would not receive proceeds. That does not break the AI thesis. It does remind investors that stock supply and fundamental demand can move on different clocks.

Competition is another real issue. Micron is the obvious memory peer, Seagate and Western Digital have their own AI storage narratives, and cloud providers can influence how much of the economics goes to device makers versus integrated storage systems. Sandisk needs the AI storage cycle to remain capacity-constrained long enough for contracts, pricing and HBF development to matter.

What would make the Sandisk thesis real

Three signals matter more than one-day price action.

First, new long-term agreements need to keep appearing with real purchase commitments, not only vague AI demand commentary. Second, data-center revenue needs to hold up even if consumer electronics and PC storage soften. Third, HBF needs credible technical milestones, ecosystem support or customer validation before the market treats it as more than a call option.

If those pieces line up, Sandisk becomes a different kind of AI stock. It will not look like Nvidia. It will not have the software optionality of a cloud platform. It may instead look like a scarce capacity vendor for the part of AI that investors usually ignore: the stored memory of machine work.

That is the cleaner way to read SNDK now. The earnings beat explains the rally. The data-exhaust thesis explains why the rally has a chance to become something larger.

FAQ

Frequently asked questions

Why is Sandisk stock moving with AI infrastructure?

Sandisk is tied to AI infrastructure because AI data centers need high-capacity storage, and Sandisk reported strong data-center revenue growth along with long-term supply agreements.

What is the AI data exhaust trade?

The AI data exhaust trade is the idea that AI agents, retrieval systems and enterprise AI workflows create persistent logs, embeddings, documents, context stores and audit trails that require more storage capacity.

What is High Bandwidth Flash?

High Bandwidth Flash is a NAND-based memory technology Sandisk and SK hynix are working to standardize for AI inference memory needs.

Is Sandisk still a cyclical NAND stock?

Yes. Sandisk remains exposed to NAND pricing, supply growth and customer inventory cycles, even if AI demand and long-term contracts improve visibility.

What should investors watch next for SNDK?

Investors should watch additional long-term supply agreements, data-center revenue durability, NAND pricing, gross margin normalization and progress on High Bandwidth Flash.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

CEO of TECHi. Building the operating system for serious tech investors. Previously led engineering at scale. Focus: AI capex thesis, semiconductor supply chain, and the equity tape.