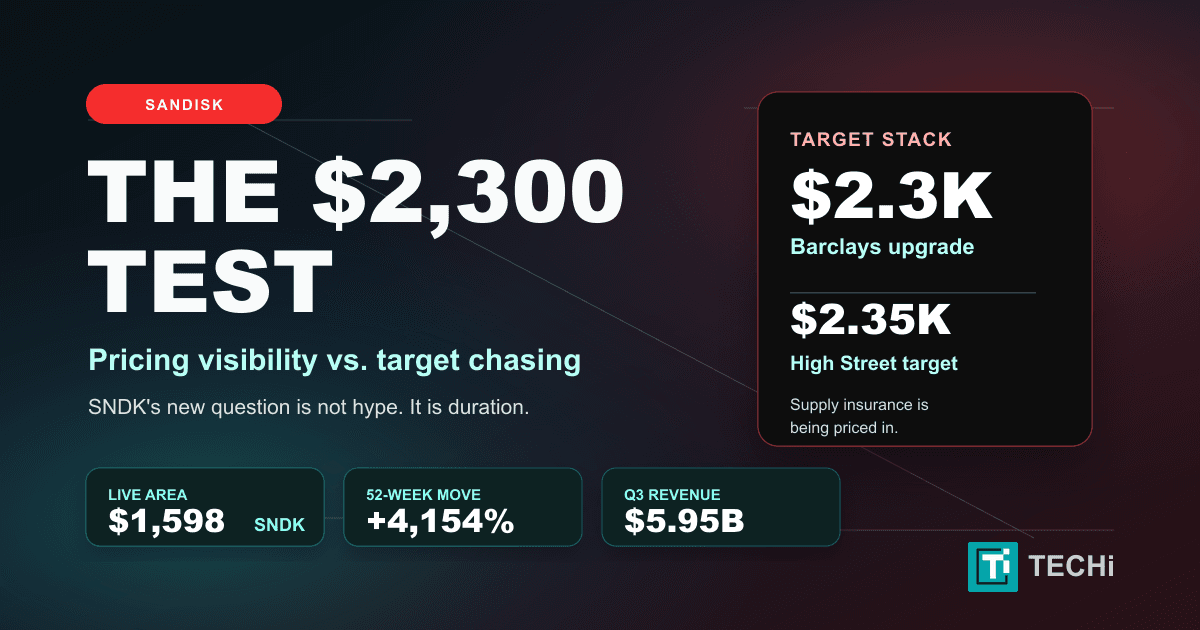

- 30.5x in twelve monthsSNDK has rallied from a $27.89 post-spin-off panic low on April 7, 2025 to an $851.77 close on April 10, 2026 — a 30.5x return on a $125.7 billion market cap.

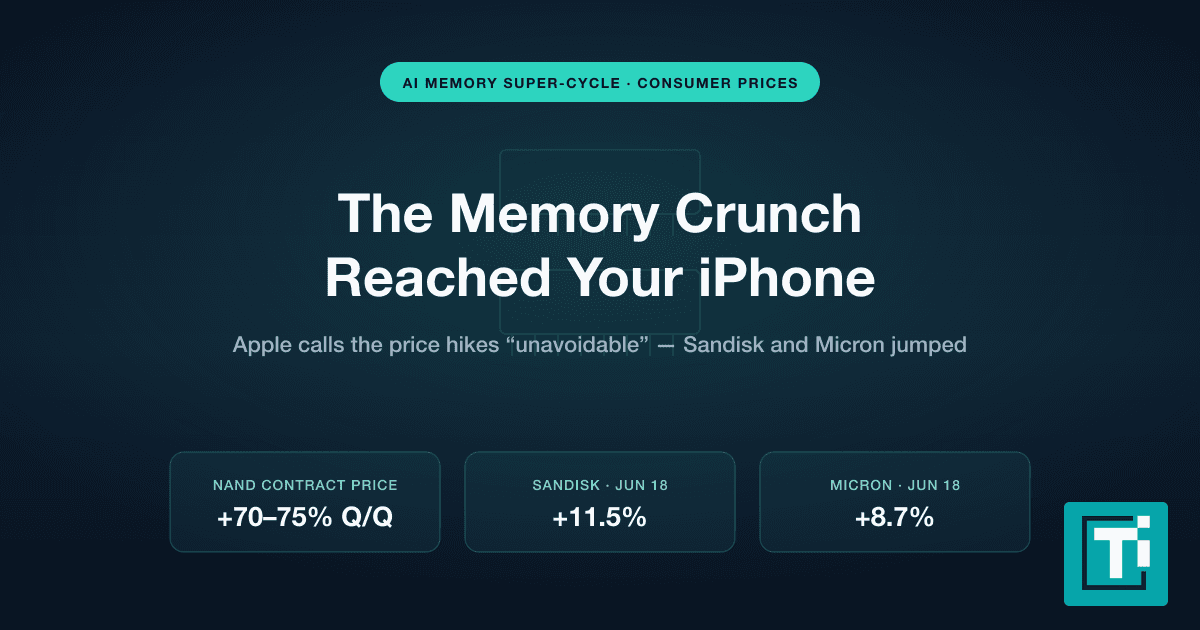

- NAND shortage through 20282026 NAND bit demand growth is tracking 20 to 22 percent against bit supply growth of just 15 to 17 percent. Multiple sell-side desks model the shortage persisting until 2028.

- Gross margin went from 26% to 67%Sandisk Q3 FY2026 gross margin guidance of 65 to 67 percent compares to 26 percent in the prior-year quarter — a 40-plus percentage point expansion in twelve months, driven entirely by NAND pricing.

- Q2 FY2026 validated the chartQ2 FY2026 revenue of $3.03 billion (up 61 percent YoY), non-GAAP EPS of $6.20 (up 404 percent), and datacenter revenue of $440 million (up 76 percent). Q3 guide: $4.4 to $4.8 billion revenue.

- HBF is the next legHigh Bandwidth Flash, co-developed with SK hynix and targeting 8 to 16 times HBM capacity at comparable bandwidth, is expected to sample in H2 2026 and could open a compute-memory product category that reprices the business again.

On April 7, 2025, Sandisk closed the day at roughly $31 but printed an intraday low of $27.89, a post-spin-off panic bottom that came six weeks after Western Digital released the NAND business as an independent company and right as the first round of Trump tariff turbulence hit the semiconductor tape. One year and three trading days later, on April 10, 2026, SNDK closed at $851.77. That is not a typo. That is a 30.5x return. A $10,000 position taken at the April 2025 low is worth roughly $305,500 today. A $100,000 position is worth $3.05 million. This is one of the most violent single-stock re-ratings the semiconductor sector has produced in modern history, and the fact that almost nobody saw it coming is half of what makes the story worth telling.

The 30x Math

The numbers are worth staring at for a moment. Sandisk's 52-week trading range runs from that April 7 low of $27.89 all the way to the $873.95 session high printed on April 10, 2026. The stock has held above $850 for two consecutive closes on rising volume, the float has effectively re-rated from a $4 billion market cap at the spring 2025 low to a $125.7 billion market cap at Friday's close on 147.6 million shares outstanding, and several sell-side shops now carry four-digit price targets (see Valuation). The year-to-date return for 2026 alone is roughly 240 to 260 percent, depending on the exact Dec. 31, 2025 closing print you use—still extraordinary in any normal market. The one-year figure is something else entirely.

To put the move in context: semiconductor investors who owned NVIDIA from the 2023 pre-ChatGPT lows into the early 2025 peak made roughly 9x. The best-performing S&P 500 component over the last five years, taken as a total return figure, is a little over 11x. Sandisk did 30x in twelve months. The only comparable single-stock moves in recent memory are the 2020 Tesla re-rating and the 2021 GameStop short squeeze, and those were not driven by fundamentals that matched the print. Sandisk is. That is the part that matters.

Why the NAND Supercycle Is Real

For most of 2023 and 2024, the memory story was HBM. High Bandwidth Memory is the stacked DRAM that sits next to AI accelerators and feeds them fast enough to keep the tensor cores busy, and the three companies that make it (SK hynix, Samsung, and Micron) captured almost all of the memory narrative and most of the equity performance. NAND flash was the forgotten sibling. Bit prices stayed depressed, oversupply persisted through the 2023 cycle trough, and the consensus view inside the industry was that any AI-driven memory lift would arrive in DRAM first and in flash only if hyperscalers ran out of SSD inventory.

Hyperscalers ran out of SSD inventory. The inflection started in late summer 2025, when the first generation of truly memory-intensive AI workloads (checkpoint storage for trillion-parameter training runs, KV-cache overflow for long-context inference, and the staging buffers for retrieval-augmented generation pipelines) collided with a NAND bit-supply base that had been under-invested for two years. Contract NAND prices rose 85 to 90 percent quarter-over-quarter in several recent quarters. Industry analysts now project 2026 NAND bit demand growth of 20 to 22 percent against bit supply growth of just 15 to 17 percent, which means the shortage is widening even as capex is ramping. TrendForce-track sources and several sell-side desks now model the shortage persisting until 2028.

For a vertically integrated pure-play NAND operator with fixed production cost and a commodity pricing model, that setup is the most leveraged possible expression of the shortage. Every dollar of price appreciation flows straight to gross margin. Every quarter of undersupply compounds the earnings lift. Sandisk's financials did not do anything clever. They just let the commodity math work.

The Q2 FY2026 Print That Validated the Chart

This is the earnings print that turned the skeptics. Q2 FY2026 revenue came in at $3.03 billion, up 61 percent year-over-year. Non-GAAP EPS hit $6.20, up 404 percent year-over-year. Datacenter revenue alone was $440 million on 76 percent year-over-year growth, and every line of the income statement compounded in the same direction. The Q3 FY2026 revenue guide is $4.4 to $4.8 billion with gross margin guidance of 65 to 67 percent, up from 26 percent in the prior-year quarter. That is a 40-plus percentage point gross margin expansion inside twelve months, which is the kind of operating leverage that only shows up in a genuine commodity supercycle and only in the vertically integrated names that control their own fab.

Contrast this with the equity performance of Sandisk's peer group. Micron is up meaningfully on the same thesis but nowhere near the same multiple, because Micron's NAND exposure is diluted by its DRAM business. Samsung carries the weight of its consumer electronics arm. SK hynix is the cleanest DRAM HBM play but does not have Sandisk's flash purity. Sandisk, after the Western Digital separation, is the only pure-play NAND operator listed in the US, which means when the NAND narrative finally turned, there was exactly one vehicle for the trade and a relatively small float to absorb the flow.

High Bandwidth Flash: The Trillion-Dollar Side Bet

The current rally is a commodity NAND shortage story. The forward thesis is something much bigger. Sandisk and SK hynix are jointly developing a new memory architecture called High Bandwidth Flash (HBF), and the specification target is aggressive: 8 to 16 times the capacity of HBM at comparable bandwidth. First engineering samples are expected in the second half of 2026. If HBF ships on schedule and performs near spec, it opens a new product category that sits between bulk NAND storage and premium HBM DRAM — and the addressable market for a memory product that can feed AI accelerators with HBM-class bandwidth at NAND-class cost per gigabyte is effectively every training and inference server shipping after 2027.

This is the part of the Sandisk story that does not show up in the current P&L and that most of the buy side has not yet modeled. If HBF becomes a standard component in next-generation AI accelerators (a real possibility given the capacity math), Sandisk goes from a vertically integrated NAND commodity play to a dual-revenue business with a differentiated, high-margin compute-memory product on top. The analyst community is not pricing that scenario yet. The tape is starting to.

Valuation, the Bear Case, and What Can Kill This

At $851.77, Sandisk trades at a forward revenue multiple that looks aggressive on the surface and defensible if you believe the Q3 FY2026 guide is a floor rather than a peak. The Q3 guidance midpoint of $4.6 billion annualizes to roughly $18.4 billion in run-rate revenue at peak margins, which on a $125.7 billion market cap implies a forward price-to-sales ratio in the 7x range, which is elevated for a memory name in a normal cycle but not absurd for a cyclical peak operator with 65-plus percent gross margins and an HBF option on top.

More recently, Bernstein raised its target to $1,250 and outlined a $3,000 bull scenario, while Cantor Fitzgerald and Jefferies both published $1,000 targets, making a path to $1,000 a mainstream Street view rather than a fringe call. Bank of America's $900 target reflects an earlier note cycle—verify timestamps on any broker PDF before trading off a single number.

The path-to-$1,000 narrative that dominated sell-side notes after the Q2 FY2026 print is essentially a bet that the shortage runs another eighteen months and that HBF comes in on schedule. The bear case is three distinct risks. First, a supply response: if Samsung, Micron, and the Kioxia joint venture simultaneously accelerate bit growth into 2027, the shortage compresses faster than consensus and contract prices come down. Second, an AI capex pause: NAND prices are leveraged to hyperscaler storage orders, and any material deceleration in Big Tech capex would reprice the forward curve sharply downward. Third, geopolitical risk around the Kioxia JV, which produces substantially all of Sandisk's flash chips at manufacturing sites in Japan. A tightening of US semiconductor export controls on advanced NAND, or any disruption to the Japan supply chain, would hit Sandisk directly and disproportionately.

None of those three risks is visible in the current order book or in the tape. All three are plausible inside the next twelve months. Position sizing matters more than directional conviction at a 30x multi-year chart. The investors who made the most money on Sandisk over the last year were the ones willing to buy a $4 billion market cap company at a post-spin-off panic low with no visible catalyst, and that is almost never the same cohort that feels comfortable buying a $125 billion one after it has already run.

What Happens From Here

The near-term setup is straightforward. Q3 FY2026 earnings will print against a guide the market believes is conservative, which means a beat and raise is the base case and anything short of that will force a re-rating. The HBF engineering sample announcement, expected in the second half of 2026, is the next hard catalyst. Any credible demonstration against spec will move the name on the day. Beyond that, the macro tape matters: every rate decision, every hyperscaler capex update, and every NAND price print from TrendForce is now a direct input into the Sandisk equity.

The longer-term question is whether Sandisk can convert a commodity shortage windfall into a durable franchise. The Kioxia joint venture was extended to 2034, which secures supply. The $1 billion Nanya Technology investment secures DRAM adjacency. The HBF roadmap with SK hynix is the attempt to build a structurally differentiated product on top of the commodity base. If even one of those three bets compounds correctly, Sandisk settles into a new multiple regime at a valuation that makes the current price look reasonable in hindsight. If none of them does, the commodity cycle eventually rolls and the stock gives back meaningful ground.

The one thing worth saying without hedging is that the 30x year is done. The only remaining question is what the next year looks like from here, and that question, for the first time in a decade, has the entire semiconductor buy side paying attention to a flash memory stock. For reference, that same community had written off NAND as a commodity dead-end as recently as the 2024 cycle trough. The tape has a way of changing minds.

FAQ

Frequently asked questions

How much has SNDK actually gained in one year?

From its post-spin-off panic low of $27.89 on April 7, 2025, Sandisk closed at $851.77 on April 10, 2026. That is a 30.5x return in twelve months and three trading days. A $10,000 position taken at the April 2025 low would be worth roughly $305,500 today. The gain since the February 2025 Western Digital spin-off debut at approximately $48 is more modest but still extraordinary: roughly 17x.

What drove the rally?

A structural NAND flash shortage. AI data center buildout pushed NAND bit demand to 20 to 22 percent growth in 2026 against only 15 to 17 percent bit supply growth, and contract NAND prices have risen 85 to 90 percent quarter-over-quarter across several recent quarters. Sandisk is one of the five largest NAND producers globally and the only pure-play of the group after the Western Digital separation, which made its earnings leverage to the shortage the cleanest in the industry.

What do the Q2 FY2026 earnings show?

Revenue of $3.03 billion, up 61 percent year-over-year. Non-GAAP EPS of $6.20, up 404 percent year-over-year. Datacenter revenue of $440 million on 76 percent year-over-year growth. The Q3 FY2026 revenue guide is $4.4 to $4.8 billion with gross margin of 65 to 67 percent, which compares to a 26 percent gross margin in the prior-year quarter. That is a 40-plus percentage point gross margin expansion inside twelve months, which is the kind of operating leverage the market rarely sees outside of a genuine commodity supercycle.

What is High Bandwidth Flash and why does it matter?

High Bandwidth Flash (HBF) is a next-generation memory architecture Sandisk is co-developing with SK hynix, targeting 8 to 16 times the capacity of HBM at comparable bandwidth. If it ships on schedule in the second half of 2026, HBF could compete directly with HBM for AI accelerator memory sockets at a fraction of the cost per gigabyte. That is a structurally different product from commodity NAND and would give Sandisk a margin mix no other pure-play flash vendor can match.

What could derail the rally?

Three things, in order of probability. First, a NAND bit-supply response: if Micron, Samsung, SK hynix, and Kioxia all push capacity harder into 2027, the shortage compresses faster than the current analyst consensus. Second, an AI capex pause: if hyperscaler spending growth decelerates into 2027 earnings, NAND prices reprice down hard. Third, China export controls on advanced NAND, which would disrupt the Kioxia JV that produces substantially all of Sandisk's chips. None of the three is visible in current earnings or order books, but all three are plausible inside the next twelve months.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Hazel Kaya writes TECHi's long-form pillar coverage of the semiconductor industry — foundries, equipment makers, design houses, and the end-market demand reshaping them. Her pieces draw on SIA shipment data, export-control filings, and capex guidance from TSMC, Samsung, and Intel. Readers come to her work for the multi-year structural view: which categories are consolidating, which are commoditizing, and how AI compute demand is rewriting the old cyclical rules.