- New keyword laneThis piece targets Sandisk price target and pricing visibility, not the older Sandisk stock, AI data exhaust or NAND supercycle angles.

- Fresh catalystBarclays lifted Sandisk to Overweight with a $2,300 target, while the high target in current forecast data is $2,350.

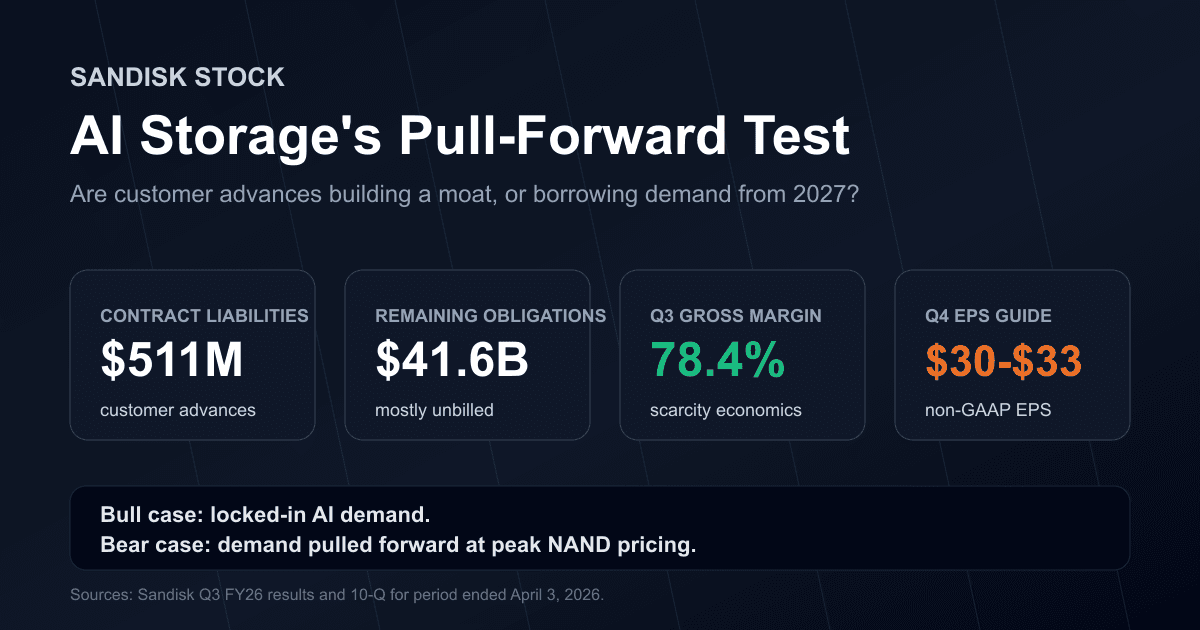

- Evidence baseSandisk's filings show $511 million of contract liabilities and $41.6 billion of remaining performance obligations tied mainly to long-term agreements.

- Volatility checkSNDK traded near $1,598 during the May 27 session, with a 52-week range stretching from $36.21 to $1,658.77.

- Core thesisThe stock's next test is whether pricing visibility lasts long enough to justify analyst models, not whether AI storage demand exists.

Sandisk's rally is now too large for the old question. Whether AI storage demand is real is no longer the hard part. At 2:45 p.m. Eastern on May 27, 2026, StockAnalysis showed SNDK at $1,598.21, up 0.54% intraday, with a $236.68 billion market value, a $1,528.28 to $1,658.77 day range and a 52-week range from $36.21 to $1,658.77. That is not a calm repricing. It is a market trying to decide how many years of tight memory supply can be capitalized into one ticker.

The fresh catalyst is Barclays. Tom O'Malley upgraded Sandisk to Overweight and lifted the target to $2,300, with Investing.com reporting that the call rests on long-term contracts, constrained supply and unusually strong pricing visibility. The phrase that matters is not "AI demand." Investors already know the demand story. The harder claim is that Sandisk now has enough contractual visibility to deserve a different kind of multiple.

That is why this piece is not a repeat of TECHi's prior Sandisk coverage. We already covered the Sandisk $511 million pull-forward question, the AI data exhaust thesis, the NAND supercycle story and the broader AI-stock risk basket. This analysis narrows the frame: the new Sandisk trade is a price-target stack pretending to be a supply-duration forecast.

What the authority sources are actually saying

Sandisk's own numbers explain why Wall Street is willing to stretch. In its fiscal third-quarter 2026 release, the company reported $5.95 billion of revenue, up 97% sequentially, GAAP net income of $3.615 billion, data-center revenue up 233% sequentially, GAAP gross margin of 78.4%, and fiscal fourth-quarter revenue guidance of $7.75 billion to $8.25 billion. Those figures are not normal flash-memory recovery numbers. They look like scarcity economics.

The filing matters even more than the press release. Sandisk's latest Form 10-Q shows $511 million of contract liabilities tied mainly to customer advances and $41.6 billion of transaction price allocated to remaining performance obligations, with $41.2 billion not yet billed and about 15% expected to be recognized over the next 12 months. That filing is the bridge between hype and evidence. It does not prove all future demand is safe. It does prove customers have moved beyond casual orders.

The analyst stack is split between excitement and caution. StockAnalysis' forecast page shows a Buy consensus across 22 analysts, an average target near $1,543 and a high target of $2,350. That is a strange setup: the highest targets are far above the tape, while the average target is slightly below the live share price. In plain English, Wall Street is chasing its own models upward but has not fully agreed on how long the current economics can last.

TipRanks' report on the Barclays move adds the contract detail behind that spread. It says Barclays moved Sandisk from Equal Weight to Overweight and raised the target from $1,200 to $2,300, while Melius Research's Ben Reitzes has a $2,350 target. TipRanks also describes Sandisk's newer agreements as a way to give customers supply assurance while giving Sandisk demand certainty, with the longest contract extending into 2031.

Why the $2,300 target is not just a bigger number

A price target usually looks like a simple valuation output. Revenue goes up, margin goes up, EPS goes up, the target follows. Sandisk is different because the target is really an argument about duration.

If Sandisk's current pricing is just a tight-cycle spike, then $2,300 is easy to attack. Memory stocks have a long history of looking cheapest near the top, because peak earnings make the multiple look reasonable right before pricing rolls over. A forward P/E can compress fast when the "E" starts falling.

If Sandisk's contracts turn NAND supply into reserved AI infrastructure capacity, the same target becomes easier to defend. Buyers are not only paying for bits. They are paying for availability, schedule certainty and protection against being second in line when AI infrastructure demand absorbs supply. That is why Barclays' language around pricing visibility matters more than the headline target.

The distinction is subtle, but it changes the whole article. The bullish Sandisk case is not "the stock went up, so targets went up." It is "targets went up because analysts are starting to model a longer window of protected pricing." That is the new angle.

The volatility is not noise

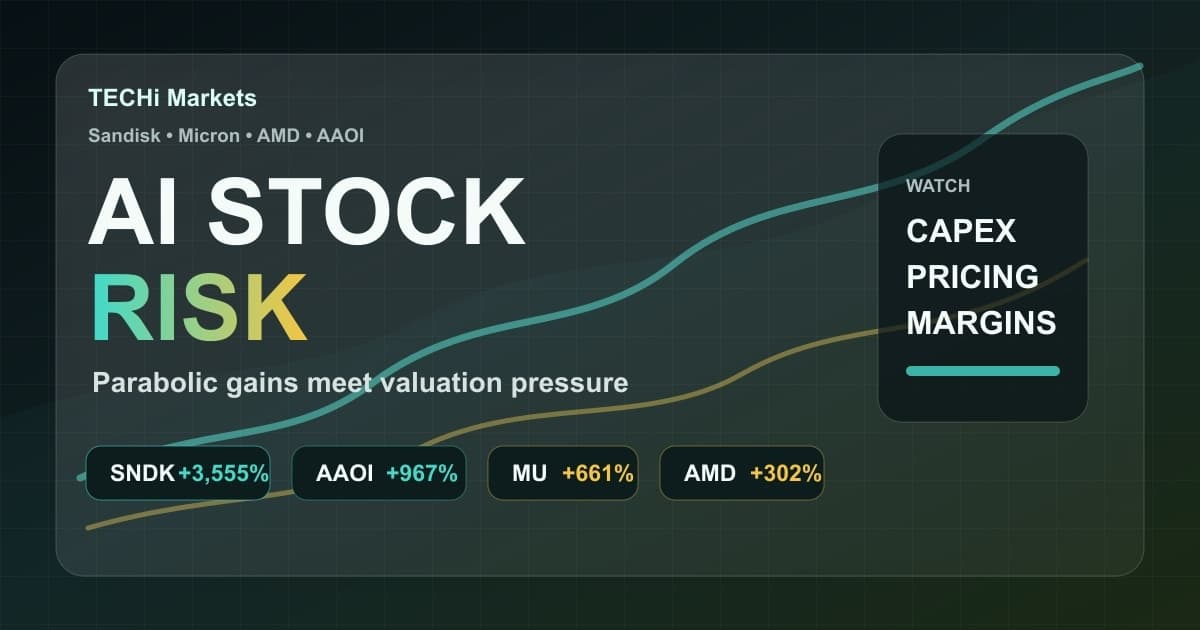

The stock's movement has become part of the evidence. StockAnalysis' statistics page shows a 52-week price gain of more than 4,154%, a trailing P/E of 53.8, a forward P/E of 9.85 and a forward price-to-sales ratio of 7.01. Those numbers can all be true at once because the market is pricing both a historic move and a huge expected earnings ramp.

That combination is unstable by design. The same stock can look expensive on trailing numbers, cheap on next-year EPS, and dangerous on chart behavior. That is not a contradiction. It is what happens when a cyclical company suddenly gets treated like a scarcity asset.

Volatility also tells investors something about crowding. When a stock with a $236 billion market value can trade in a $130 intraday range, the tape is not just digesting fundamentals. It is digesting model revisions, short covering, momentum flows, options positioning and fear of missing the next target raise. Anyone reading the $2,300 target as a clean 12-month roadmap is ignoring the machine around the trade.

The hype question has the wrong edge

Calling Sandisk hype is too easy. The company did print the revenue, margin and guidance. It did disclose customer advances and remaining performance obligations. Analysts are not inventing the entire story from social-media momentum.

Calling the rally fully justified is also too easy. A stock can have real fundamentals and still be priced for too much certainty. The market is not paying only for Q3. It is paying for the belief that the Q3 economics are the beginning of a longer pricing regime.

That is where the debate should sit. The $2,300 to $2,350 target zone assumes that Sandisk's new contract model changes the downside profile of a business investors used to treat as cyclical. The average analyst target below the live price says the Street is not all the way there yet. The gap between those two numbers is the actual story.

What has to happen for the bull case to work

First, the remaining performance obligations need to convert without causing a later air pocket. A big RPO balance is useful only if customers keep taking product at economics that support the margin thesis. If the RPO grows while cash advances rise and revenue conversion stays orderly, the bull case gains credibility. If customers pulled forward demand during a shortage, the same accounting lines become warning signs.

Second, Sandisk's gross margin has to stay high enough to prove this is not a one-quarter shortage print. A 78.4% GAAP gross margin is extraordinary for this category. The market does not need that exact number forever, but it needs proof that the next normalized margin base is much higher than the old one.

Third, the analyst stack has to broaden. A $2,300 Barclays target and a $2,350 high target can move a stock, but durable support comes when more firms lift their base cases for 2027 and 2028 earnings. If the average target remains below the share price while the highest targets get the headlines, the market will keep trading Sandisk like a contested momentum name.

Fourth, the company needs to keep showing that its customer relationships are not only about shortage panic. Long-term supply agreements are powerful when they reflect strategic capacity planning. They are fragile when they reflect buyers scrambling for product near a pricing peak.

What can break the story

The first risk is supply. If competitors add capacity faster than expected or if customer ordering normalizes before the market expects it, pricing visibility becomes less valuable. Contracts can reduce volatility, but they cannot repeal semiconductor cyclicality.

The second risk is valuation psychology. When a stock has already moved thousands of percent in a year, the burden of proof shifts. Good news is not enough. The market needs better-than-good news, and it needs it repeatedly.

The third risk is the target-chase itself. Price targets are useful when they force investors to update assumptions. They are dangerous when they become the reason for the trade. A $2,300 target is not a floor. It is a model output that depends on high margins, tight supply, customer commitments and time.

What investors should watch next

The most important number is not the next analyst target. It is the next update on contract liabilities, RPO conversion and the margin range. Those three items will say more about Sandisk's durability than the daily share price.

The next earnings report also needs to answer a plain question: is pricing visibility improving because customers are planning years ahead, or because everyone is scared of being short in the current cycle? The first answer supports a higher multiple. The second answer supports caution, even if revenue keeps rising for another quarter or two.

Sandisk's stock is both hype and substance. The hype is in the speed of the move and the way each new target becomes a trading event. The substance is in the filings, the customer advances, the RPO balance and the earnings power already reported. Investors who treat it as only hype are missing the evidence. Investors who treat it as only evidence are missing the risk.

The cleanest read is this: Sandisk is no longer just a memory stock with a big AI tailwind. It is a market test of whether storage supply can be reserved like strategic infrastructure. If that answer is yes, the $2,300 target is not absurd. If the answer is no, the same target will look like a marker from the hottest part of the cycle.

FAQ

Frequently asked questions

Why did Barclays raise Sandisk's price target to $2,300?

Barclays raised Sandisk to Overweight and lifted its target to $2,300 because it sees long-term contracts, tight supply and stronger pricing visibility changing the company's earnings profile.

What is the new angle on Sandisk stock?

The new angle is that Sandisk's analyst targets are acting like supply-duration forecasts. The debate is whether contract visibility lasts long enough to support the $2,300 to $2,350 target range.

Is Sandisk's rally only hype?

No. Sandisk has reported strong revenue, margins and guidance, and its SEC filing shows contract liabilities and remaining performance obligations. The risk is that the stock may still be pricing too much certainty.

What should investors watch next for SNDK?

Investors should watch contract liabilities, remaining performance obligation conversion, gross margin durability, new long-term supply agreements and whether average analyst targets keep catching up to the high targets.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Hazel Kaya writes TECHi's long-form pillar coverage of the semiconductor industry — foundries, equipment makers, design houses, and the end-market demand reshaping them. Her pieces draw on SIA shipment data, export-control filings, and capex guidance from TSMC, Samsung, and Intel. Readers come to her work for the multi-year structural view: which categories are consolidating, which are commoditizing, and how AI compute demand is rewriting the old cyclical rules.