Sandisk stock has already had the kind of move that makes normal valuation language feel inadequate. The easier story is that AI has created a NAND shortage and Sandisk is one of the biggest winners. That story is true enough, but it is no longer the most interesting part of the trade.

The sharper question is whether Sandisk is turning AI storage demand into a durable reservation business, or whether customers are pulling future demand into 2026 because they are scared of not having enough capacity.

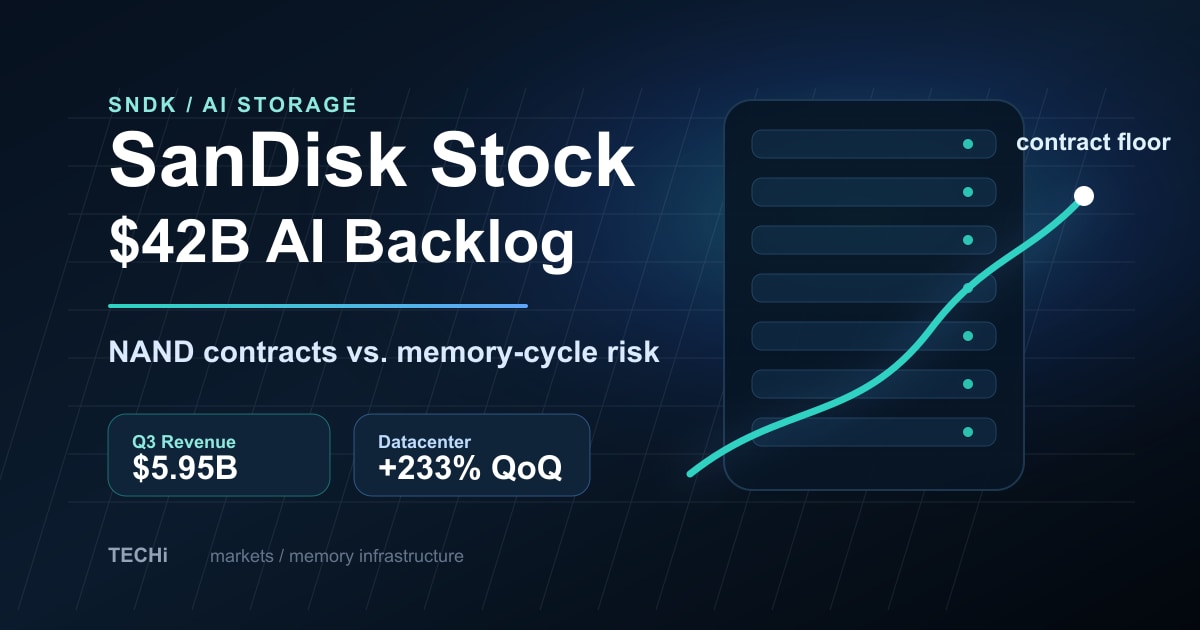

That distinction matters because Sandisk’s latest numbers look less like an ordinary memory-cycle rebound and more like scarcity economics. In its fiscal third-quarter results, Sandisk reported $5.95 billion of revenue, up 97% sequentially. Data center revenue rose 233% sequentially. GAAP gross margin reached 78.4%, and the company guided fiscal fourth-quarter revenue to $7.75 billion to $8.25 billion with non-GAAP EPS of $30 to $33.

Those numbers are extraordinary. The hidden issue is what sits underneath them.

Sandisk also disclosed multiple new multi-year customer agreements. In its latest Form 10-Q, the company describes long-term agreements and capacity arrangements that can include purchase commitments, customer advances and financial guarantees. The same filing shows $511 million of contract liabilities, mainly customer advances, and $41.6 billion of remaining performance obligations, most of them unbilled.

That is the real story for Sandisk stock now. This is not just an AI storage boom. It is a test of whether pre-committed AI storage demand is a moat or a pull-forward trap.

The bull case: AI customers are reserving scarce storage

The bullish interpretation is straightforward. Hyperscalers and AI infrastructure buyers are not treating NAND as a commodity they can casually buy later. They are trying to reserve supply.

That is a different business quality than a normal flash-memory upswing. If customers are signing long-term commitments because inference, model serving and AI data retention are becoming storage-heavy workloads, Sandisk’s earnings base could be structurally higher than investors expected when the company separated from Western Digital. TECHi’s earlier Sandisk 30x spin-off analysis covered the supercycle setup; this draft pushes into the accounting signal behind the demand.

This also explains the violence in margins. A 78.4% GAAP gross margin is not normal NAND-cycle behavior. It implies customers are paying for certainty, not simply shopping for the lowest-cost bit.

Reuters, via MarketScreener, reported that Sandisk’s long-term contracts are worth at least $42 billion. If that demand is real, recurring and tied to AI infrastructure budgets rather than temporary inventory building, Sandisk deserves to trade less like a boom-bust memory name and more like a strategic AI capacity supplier.

That is why the $511 million line is important. Customer advances are not just accounting noise. They are evidence that buyers may be willing to fund the queue.

The bear case: customers may be borrowing from 2027

The bearish interpretation is not that Sandisk’s quarter was weak. It was the opposite. The bearish risk is that the quarter was too strong.

When AI infrastructure buyers fear capacity shortages, they can over-order, prepay and sign long-term supply agreements to avoid being last in line. That behavior can make current demand look cleaner than it really is.

The 10-Q is explicit that these arrangements create risk. Sandisk says failure by the company or customers to perform under these agreements could lead to consequences involving gross margins, inventory and capacity utilization. In plain English, a demand reservation cycle cuts both ways. It can stabilize the business while orders are rising, but it can also expose the company if customers later have too much inventory or if AI storage consumption does not match the pace of commitments.

This is the new risk in Sandisk stock: 2026 earnings may be real, but still partly pulled forward. It also fits the broader warning TECHi raised in its Sandisk, Micron, AMD and AAOI AI-stock risk piece: the AI supply chain can produce huge winners while hiding timing risk inside customer behavior.

That makes the stock more complicated than a simple “AI winner” label. If customers are ordering ahead of need, the current margin structure may be closer to peak-scarcity pricing than a sustainable baseline. If customers are prepaying because AI workloads permanently changed storage intensity, the market may still be underestimating Sandisk.

HBF and UltraQLC are optionality, not proof

The technology story strengthens the bull case, but it does not settle the debate.

Sandisk and SK hynix have begun global standardization work for High Bandwidth Flash, a next-generation memory approach aimed at AI workloads. Sandisk has also showcased its UltraQLC platform, including a 128TB enterprise SSD and a path toward 256TB.

Those are real AI-storage signals. They give Sandisk a credible story beyond ordinary NAND pricing.

But investors should separate product optionality from earnings proof. HBF and UltraQLC can support the idea that AI inference and data-center storage are becoming bigger opportunities. They do not prove that 78%-plus gross margin is the new normal, or that customers will keep accepting the same economics after capacity catches up.

That is why this story is better than the basic AI-storage thesis. The technology is the upside. The commitments and advances are the stress test.

Why this is different from the earlier Sandisk AI trade

TECHi’s earlier Sandisk AI data-exhaust analysis focused on the idea that AI creates more storage demand because models, embeddings, logs and inference outputs generate huge data exhaust. That is still the demand-side argument.

This new angle is about the financing and accounting of that demand.

The market has moved from asking whether AI needs more storage to asking how desperate customers are to lock that storage down. That shift changes what investors should watch. Revenue growth is no longer enough. The important variables are customer advances, backlog conversion, gross-margin durability and whether multi-year agreements become a stabilizing base or a future air pocket.

It also connects Sandisk to the wider AI capex cycle. TECHi’s S&P 500 concentration analysis showed how much recent market strength has depended on AI infrastructure leaders. Sandisk is now one of the purer storage-side expressions of the same trade.

What investors should watch next

The next earnings report should be judged on more than revenue and EPS.

First, watch whether customer advances continue rising. A steady increase could support the reservation-moat thesis. A sudden reversal would be a warning that customers are less willing to fund the queue.

Second, watch remaining performance obligations. A $41.6 billion figure gives Sandisk visibility, but the quality of that visibility depends on timing, pricing and cancellation or performance risk.

Third, watch gross margin. A fall from 78.4% would not automatically be bad. The question is whether margins normalize to still-excellent levels or collapse toward old-cycle NAND behavior.

Fourth, watch inventory commentary. If customers have over-reserved, the first hints may appear in channel inventory, shipment timing or softer language around data-center storage demand.

Fifth, watch capex discipline. Sandisk announced a $6 billion share-repurchase authorization alongside the Q3 results. Buybacks can be powerful when earnings are durable. They are riskier if earnings are at a cycle peak.

Bottom line

Sandisk stock is no longer just a NAND recovery trade. It is a bet on whether AI customers are willing to reserve storage capacity for years.

That can be a moat. Customer advances, long-term commitments and huge remaining obligations can make Sandisk look less cyclical than memory investors expected.

It can also be a trap. If customers are front-loading orders because the AI storage market is temporarily tight, 2026 could become the earnings peak investors mistake for a new base.

The best way to frame Sandisk now is not “AI storage winner or loser.” It is more precise: Sandisk is testing whether AI infrastructure demand can turn NAND from a commodity cycle into a reservation market. The answer will decide whether the stock’s explosive rerating still has support, or whether the strongest numbers already pulled tomorrow into today.

FAQ

Frequently asked questions

Why is Sandisk stock tied to AI?

Sandisk is tied to AI because AI infrastructure creates heavy demand for data-center storage, NAND flash, high-capacity SSDs and future memory products such as High Bandwidth Flash.

What is the $511 million warning for Sandisk stock?

Sandisk disclosed $511 million of contract liabilities, mainly customer advances, in its 10-Q. That can signal strong demand, but it also raises the question of whether customers are pulling future purchases forward.

Is Sandisk’s AI storage demand a moat?

It can be a moat if long-term agreements lock in durable customer demand and capacity utilization. It becomes a risk if customers over-reserve supply during a shortage and future orders slow.

What should investors watch next for SNDK?

Investors should watch customer advances, remaining performance obligations, gross margin durability, inventory commentary and whether AI storage demand converts into recurring revenue rather than one-time scarcity pricing.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Aj Liptak is a full-time student at Bradley University majoring in computer information systems and pre-law.