- Core thesisNvidia stock is increasingly tied to whether AI factory buyers can keep financing GPUs, power, land and upgrades.

- Primary-source clueNvidia’s 10-K explicitly names data center, energy and capital availability as crucial to future revenue.

- Public test caseCoreWeave disclosed $21.6B of debt at year-end 2025 and later entered an $8.5B facility tied to GPU infrastructure.

- Rubin paradoxVera Rubin can strengthen Nvidia’s lead while raising tougher residual-value questions for older GPU fleets.

- Investor watchThe May 20 earnings call should be read for partner financing, guarantees, customer mix and deployment timing, not only revenue growth.

Nvidia stock is still being debated as a chip-demand story. The sharper 2026 question is becoming a financing story: can the companies building AI factories keep borrowing enough money, securing enough power, and upgrading fast enough to turn Blackwell and Rubin demand into durable revenue?

Both things can be true at once. Nvidia can remain the strongest AI infrastructure company in the market, and NVDA stock can still carry a risk that does not show up in a simple GPU backlog chart.

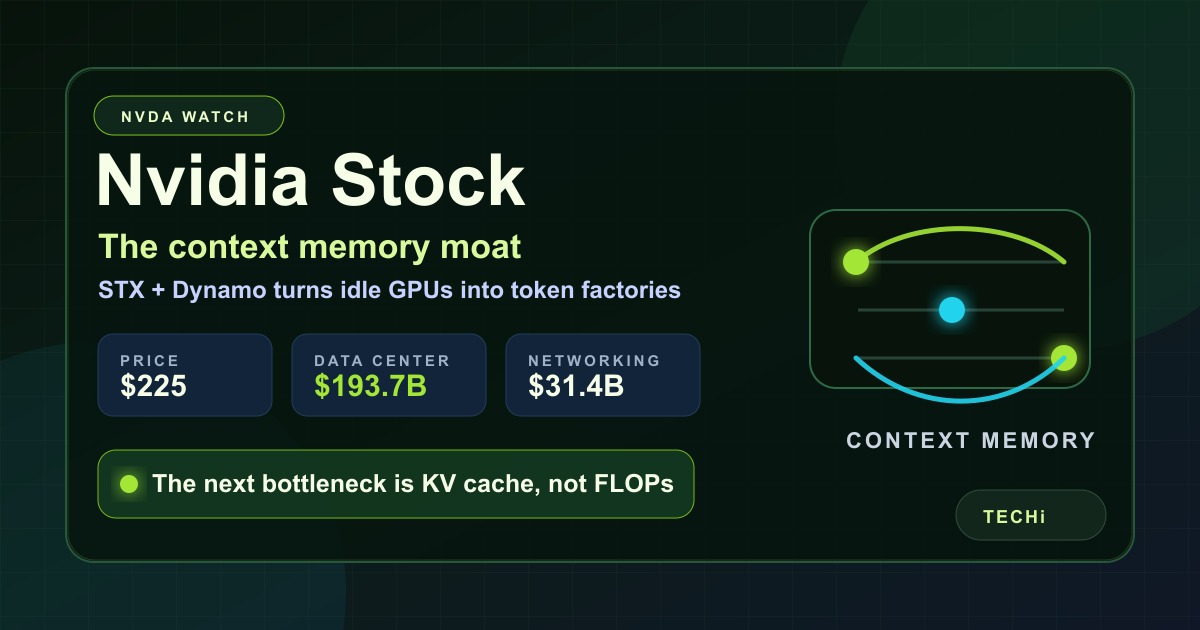

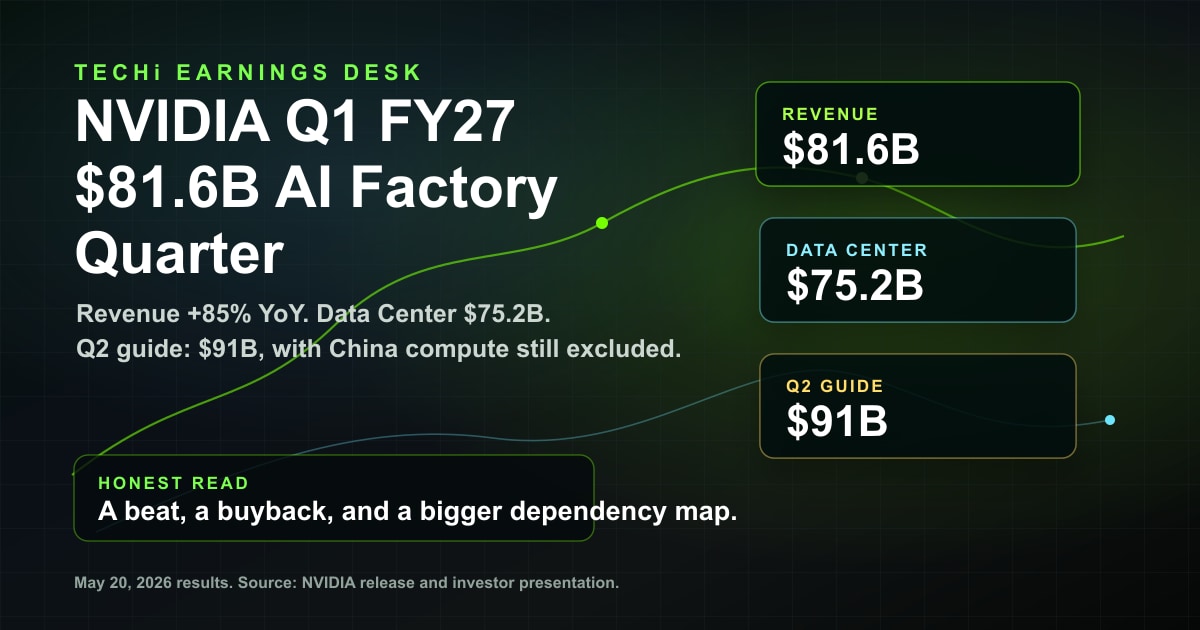

Nvidia reported record fiscal 2026 revenue of $215.9 billion, with full-year Data Center revenue of $193.7 billion and first-quarter fiscal 2027 guidance for $78 billion in revenue. The same release said Nvidia was not assuming any Data Center compute revenue from China in that outlook. That makes the current setup cleaner than the usual export-control debate: the biggest question for 2026 is not only whether customers want Nvidia chips. It is whether the AI factory buildout can stay financed.

The market is still asking the old Nvidia question

The old question is simple: how many Blackwell systems can Nvidia ship, and how quickly can Vera Rubin extend the cycle? That question still matters. TECHi’s broader Nvidia stock forecast covers the platform story, order visibility, and Rubin roadmap, while the live NVDA quote page gives the ticker context around this article’s market snapshot.

The new question is harder because it lives below the revenue line of the AI boom. AI labs, hyperscalers, neoclouds and infrastructure funds are not buying a small batch of chips. They are financing entire campuses: GPUs, networking, cooling, land, substations, power contracts, software layers and customer commitments. That is why TECHi’s AI data center power-stock story matters to the Nvidia thesis: the constraint is no longer just silicon supply.

That changes the quality of the NVDA debate. A normal semiconductor cycle breaks when demand fades. This cycle can also wobble if financing gets expensive, if collateral values change, or if the upgrade cadence makes last-generation GPU fleets depreciate faster than lenders expected.

That is the GPU debt cliff: not one maturity date, but a cluster of financing, depreciation and refinancing risks sitting underneath AI compute demand.

Nvidia’s own filing points to the pressure point

Nvidia is not hiding the issue. In its fiscal 2026 Form 10-K, the company says the availability of data centers, energy and capital to support customer and partner buildouts is crucial to future revenue and financial performance. It also warns that less-capitalized companies can face difficulty financing large-scale infrastructure projects, which could delay deployments or reduce the scale of AI adoption.

The same Nvidia 10-K gives the harder edge of the story. Nvidia disclosed $17.5 billion of investments in private companies and infrastructure funds in fiscal 2026, primarily to support early-stage startups. It also disclosed $3.5 billion in land, power and shell guarantees to early-stage companies, generally over multiyear periods.

That is not a bearish footnote by itself. It shows how valuable Nvidia’s ecosystem has become. But it also shows that Nvidia is not only selling into the AI buildout. It is helping make the buildout possible.

CoreWeave is the cleanest public window into the risk

CoreWeave is not a perfect proxy for all Nvidia demand. Hyperscalers still matter more, and Nvidia’s customer base is broader than one neocloud. But CoreWeave is one of the clearest public windows into the financing model behind AI compute.

CoreWeave disclosed in its 2025 Form 10-K that it had $21.6 billion of total indebtedness as of December 31, 2025, along with $3.7 billion of undrawn availability under several credit facilities. It also reported $10.3 billion of cash used in investing activities in 2025, driven by infrastructure investments including its GPU fleet, networking equipment, servers and switches.

Then the financing machine kept moving. On March 30, 2026, a CoreWeave subsidiary entered into an 8.5 billion delayed-draw term loan facility primarily to finance capital expenditures required for a customer contract, including GPU servers and related infrastructure. The filing says the facility is secured by substantially all assets of the borrowing subsidiary and includes a debt service coverage covenant.

That is the part NVDA investors should study. If GPU-backed financing stays liquid, Nvidia’s ecosystem can absorb more systems at speed. If lenders demand higher spreads, tighter covenants or more customer prepayments, deployments can stretch. Demand can remain real while revenue timing gets more fragile.

Nvidia is now helping finance the demand curve

Nvidia’s January 2026 CoreWeave announcement makes the relationship explicit. Nvidia said it invested $2 billion in CoreWeave Class A common stock at $87.20 per share and said the expanded relationship would help CoreWeave accelerate the buildout of more than 5 gigawatts of AI factories by 2030.

The same Nvidia-CoreWeave announcement says the companies intend to leverage Nvidia’s financial strength to accelerate CoreWeave’s procurement of land, power and shell for AI factories. That sentence is the story.

Nvidia is not merely waiting for demand. It is shaping the financing, infrastructure and partner architecture that converts demand into deployed capacity. For bulls, that is strategic control. For skeptics, it starts to look like circularity: the supplier helps strengthen the customer that buys the supplier’s systems.

The truth is more useful than either slogan. Nvidia’s ecosystem support can be rational, accretive and strategically necessary. It can also make the stock more sensitive to credit conditions than traditional chip-stock analysis suggests.

Rubin makes the debt question sharper

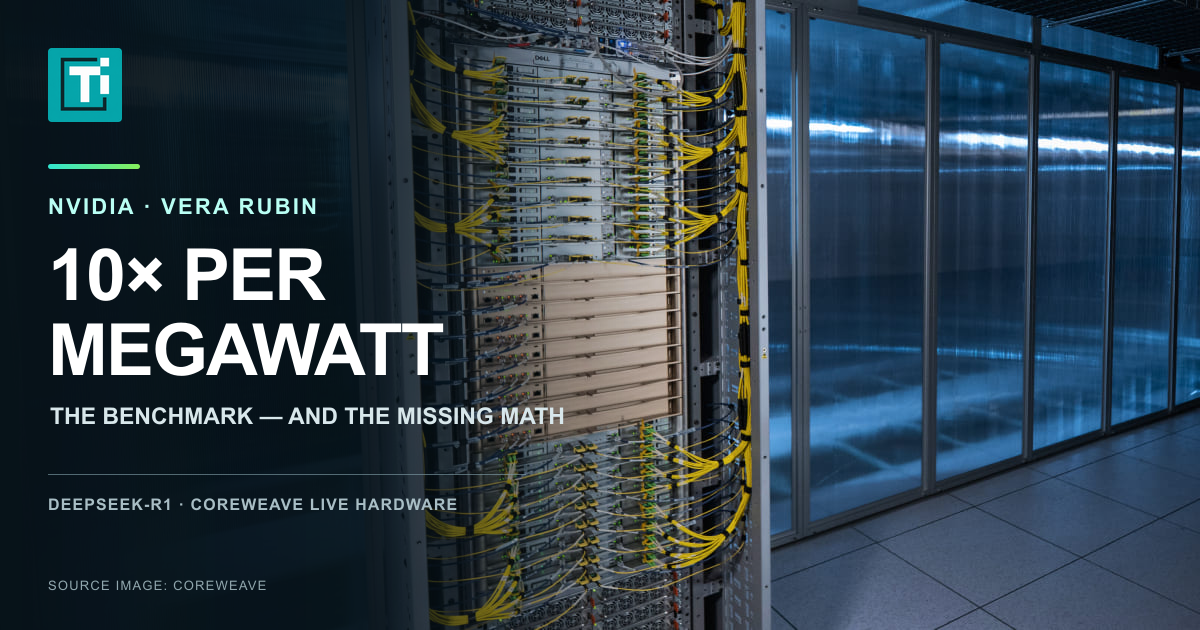

Vera Rubin is bullish for Nvidia’s technology lead. Nvidia says the Vera Rubin NVL72 rack integrates 72 Rubin GPUs and 36 Vera CPUs and can train large mixture-of-experts models with one-fourth the number of GPUs compared with Blackwell. Nvidia also says the platform can reach up to 10 times higher inference throughput per watt at one-tenth the cost per token.

That is exactly why lenders and investors should care about depreciation. If Rubin lowers the cost per token fast enough, the economic life of older GPU fleets becomes a live question. H100, H200, Blackwell and Blackwell Ultra systems can still be useful, but utilization, rental rates and refinancing value matter more when the next platform promises a step-change in efficiency. TECHi’s Micron and Nvidia memory analysis shows the same system-level shift from another angle: the rack is now the economic unit, not just the GPU die.

A faster product cadence is good for Nvidia’s sales engine. It is less comfortable for anyone financing GPU fleets with assumptions about residual value.

This is where the debt cliff becomes a stock-market story. The risk is not that AI demand vanishes overnight. The risk is that the economics of yesterday’s capacity change faster than the financing attached to that capacity.

The China debate may be distracting investors

China still matters. Export rules, H20 write-downs and H200 licensing can move Nvidia’s reported numbers and margins. Nvidia disclosed a $4.5 billion H20 charge in fiscal 2026 and said it had not generated H200 licensing revenue as of the 10-K filing.

But Nvidia’s own guidance already excluded China Data Center compute revenue. That means a clean beat in the next report may say less about China than about whether non-China AI infrastructure demand is still converting into shipped, installed and financed systems.

Nvidia will host its first-quarter fiscal 2027 results call on May 20, 2026. Investors should listen for language around customer categories, partner financing, purchase commitments, deployment timing, power availability and any further expansion of ecosystem investments or guarantees.

The question is not simply, "Did Nvidia beat?" The better question is, "Who is carrying the capital cost of the next leg?"

What would make the risk matter for NVDA stock

This risk becomes material if several things happen together.

First, AI cloud providers need more debt or equity to keep pace with contracted capacity. Second, lenders start marking GPU collateral more conservatively because Rubin improves performance-per-watt and token economics. Third, large customers push for cheaper inference pricing just as neoclouds are still digesting expensive earlier fleets. Fourth, Nvidia has to keep using investments, guarantees or partner support to make the ecosystem grow at the speed Wall Street expects.

None of those conditions proves the bull case is broken. But they change the multiple investors should pay for it.

A pure software platform gets a premium multiple because revenue scales without the same capital intensity. A hardware supplier with a dominant platform can also deserve a premium. A hardware supplier that increasingly helps finance the infrastructure layer deserves a more careful risk model.

That is the new angle on Nvidia stock in 2026. The company may still have the best AI hardware roadmap in the world. The market now has to decide how much credit risk is embedded in the path from GPU order to AI factory cash flow.

Investor takeaway

NVDA does not need a demand collapse to disappoint investors. It only needs a gap between the market’s clean demand narrative and the messier financing reality underneath it.

The bullish case is still strong: Blackwell remains central to the current buildout, Rubin extends Nvidia’s performance lead, and hyperscaler demand can keep absorbing capacity. The more cautious read is that Nvidia’s next risk is migrating from chips to balance sheets.

For long-term investors, the right question is not whether Nvidia is a great company. It is. The question is whether the stock is priced for a world where AI compute financing stays easy, GPU residual values hold, and every partner can keep building through a faster upgrade cycle.

That is a narrower and more dangerous bet than the headline AI boom makes it sound.

FAQ

Frequently asked questions

What is the GPU debt cliff for Nvidia stock?

The GPU debt cliff is the risk that AI cloud providers and infrastructure partners finance large GPU fleets with debt, then face refinancing, depreciation or utilization pressure as newer Nvidia platforms arrive.

Why does CoreWeave matter to Nvidia investors?

CoreWeave is not Nvidia's whole demand base, but its public filings show how capital-intensive AI cloud capacity has become, including large debt facilities tied to GPU servers and infrastructure.

Is this bearish for NVDA stock?

Not automatically. The article's point is that Nvidia's demand story is still strong, but investors should model financing risk, partner balance sheets and upgrade-cycle pressure alongside revenue growth.

What should investors watch in Nvidia's May 2026 earnings call?

Watch for commentary on Data Center customer categories, partner financing, deployment timing, ecosystem investments, guarantees, China assumptions and the Rubin ramp.

How can Rubin be both bullish and risky?

Rubin is bullish because it can improve Nvidia's performance lead, but faster efficiency gains can pressure the economics and residual values of older financed GPU fleets.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Hazel Kaya writes TECHi's long-form pillar coverage of the semiconductor industry — foundries, equipment makers, design houses, and the end-market demand reshaping them. Her pieces draw on SIA shipment data, export-control filings, and capex guidance from TSMC, Samsung, and Intel. Readers come to her work for the multi-year structural view: which categories are consolidating, which are commoditizing, and how AI compute demand is rewriting the old cyclical rules.