- The setupAI infrastructure demand is real, but the biggest stock gains now require near-perfect execution.

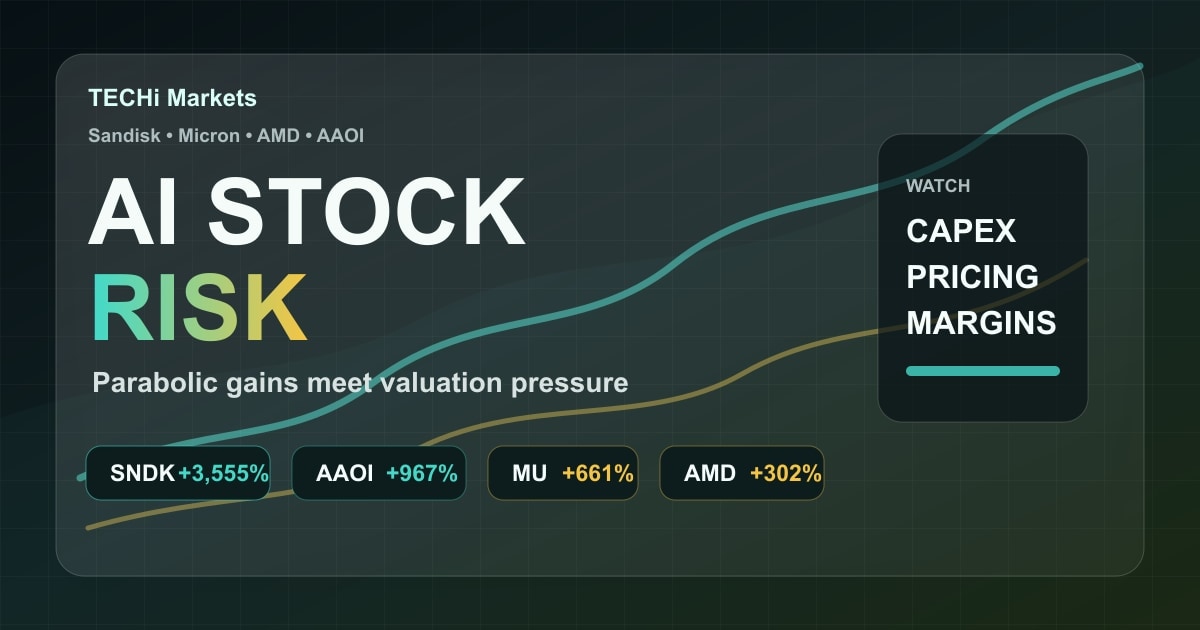

- The returnsSNDK, AAOI, MU and AMD rose roughly 3,555%, 967%, 661% and 302% over the measured 12-month close-to-close window.

- The riskA strong business can still become a dangerous entry when the valuation already assumes supply shortages and margin expansion continue.

- The splitSandisk and Micron are memory-cycle trades, AMD is a higher-quality AI chip platform, and AAOI is a more fragile optical-networking ramp.

- The watchlistInvestors should track hyperscaler capex, pricing, backlog quality, margins and customer concentration before chasing the next move.

The risk in AI stocks is no longer whether AI infrastructure demand exists. It does. The harder question is whether investors have already paid for perfect execution in the companies supplying memory, optical links, accelerators and data-center capacity.

The move has been extreme enough to change the investor job. TECHi calculations from Yahoo Finance adjusted-close data show Sandisk up roughly 3,555% from May 8, 2025 to the May 7, 2026 close, based on SNDK history. Applied Optoelectronics rose about 967% on the same basis using AAOI history, while Micron gained about 661% from MU history and AMD gained about 302% from AMD history.

Those are not normal one-year returns. They are the kind of moves that turn a good thesis into a valuation test. The issue for investors is not that the AI buildout is fake. The issue is that stocks can fall hard even when the theme remains intact.

This is the next chapter of TECHi's AI stocks coverage. The first phase was about identifying the infrastructure winners. The current phase is about deciding how much future growth is already inside the price.

The Money Flow Is Real

The buying pressure has a real foundation. Microsoft told investors that fiscal Q3 capital expenditures were $31.9 billion and said calendar-year 2026 capex should be roughly $190 billion, including about $25 billion from higher component pricing, according to its Q3 call. Meta said in its 10-Q that it expects $125 billion to $145 billion of 2026 capex to support AI efforts and the core business. Amazon said it landed more than 2.1 million AI chips over the past 12 months and plans to deploy more than one million NVIDIA GPUs starting in 2026, according to its Q1 release. Alphabet reported $35.7 billion of Q1 purchases of property and equipment in its earnings release.

That spending explains why the market has chased suppliers instead of only software apps. Memory, storage, optics, accelerators and server components are where the cash hits first. Sandisk, Micron, AMD and AAOI sit in different parts of that chain, but all four are tied to the same investor assumption: hyperscaler AI spending keeps rising and supply stays tight enough to protect pricing.

The New Risk Is Expectations

A stock can be cheap before it triples and expensive after it triples. That sounds obvious, but it is easy to forget during a vertical tape. After a 300%, 600% or 900% move, investors are no longer buying only current earnings. They are buying a future path where demand keeps accelerating, supply does not catch up, margins stay high, customers do not pause orders, and competitors fail to spoil pricing.

That is a lot to ask from any company. It is especially demanding in semiconductors and optical hardware, where cycles can turn quickly when capacity arrives or customers digest inventory.

The better question is not whether AI demand is real. It is whether the next surprise is still positive enough to justify the new market cap.

Sandisk Is the Cleanest Warning

Sandisk is the most dramatic example because the company has become a pure read on NAND pricing and AI storage demand. In its April 30 fiscal Q3 release, Sandisk reported revenue of $5.95 billion, up 97% sequentially, with datacenter revenue up 233% from the prior quarter and 645% year over year. It also guided fiscal Q4 revenue to $7.75 billion to $8.25 billion.

Those numbers explain why the stock went vertical. They do not remove the risk. NAND flash has historically been cyclical, and Sandisk's own filing language points to risks around demand volatility, pricing trends, customer relationships and supply-chain disruption. That does not make Sandisk a bad company. It means the stock has moved from recovery story to perfection story.

That is why the old Sandisk supercycle thesis needs a new filter. The business may still be improving, but a buyer after a 3,500% gain is underwriting a very different risk than a buyer before the market recognized the NAND squeeze.

Micron Has Better Scale, But Not Immunity

Micron looks stronger because its numbers are broader and its AI memory exposure is direct. In fiscal Q2, Micron reported revenue of $23.86 billion, up from $13.64 billion in the prior quarter and $8.05 billion a year earlier. Management said the company set records across revenue, gross margin, EPS and free cash flow, and guided fiscal Q3 revenue to $33.5 billion plus or minus $750 million.

That is exceptional operating momentum. It also raises the hurdle. Micron's stock no longer needs good memory demand to work; it needs demand and margins to keep beating expectations that have already moved sharply higher. Investors who read TECHi's recent Micron warning will recognize the setup: the cycle is strong, but the stock is now sensitive to any sign that the tight-supply story is peaking.

AMD Is Stronger, But Still Exposed to the Same Psychology

AMD is not a small speculative infrastructure stock. It is a large chip designer with CPUs, accelerators and a data-center business that is now central to the company's story. In its Q1 2026 report, AMD said revenue rose 38% year over year to $10.253 billion, data-center revenue rose 57% to $5.8 billion, and Q2 revenue is expected to be about $11.2 billion plus or minus $300 million.

Those figures justify AMD's place in the AI trade. They do not make the stock immune to multiple compression. If the market starts paying less for future AI revenue, AMD can have a good product cycle and still trade lower. The question after the latest AMD AI test is not whether AMD has momentum; it is how much of that momentum investors have already capitalized.

AAOI Shows the Small-Cap Version of the Same Problem

Applied Optoelectronics is where the upside and fragility sit closer together. The company said in its Q1 results that revenue rose to $151.1 million from $99.9 million a year earlier, that datacenter revenue reached $81.4 million, and that it completed its first volume shipment of 800G products to a large hyperscale customer. Management also said Q1 was its fourth consecutive quarter of record revenue.

The risk is in the rest of the same release. AAOI still reported a GAAP net loss of $14.3 million, and it is ramping manufacturing capacity while demand is hot. That can work very well when orders keep coming. It can also punish shareholders if capacity, pricing, customer timing or funding conditions move against the company.

This is why smaller AI infrastructure stocks should not be treated as safer just because they are closer to a bottleneck. They often have more operating leverage, more customer concentration and less room for a forecast mistake.

What Investors Should Watch Now

The first watch item is capex guidance from the buyers. If Microsoft, Meta, Amazon or Alphabet slow the pace, the supplier stocks will feel it before the AI theme disappears.

The second is pricing. Sandisk and Micron have been rewarded because memory and storage economics improved dramatically. If supply catches up or customers push back, margins can reset faster than narratives.

The third is backlog quality. For AAOI and other optics names, investors should separate firm orders from broad demand commentary. Capacity expansion is bullish only if utilization stays high.

The fourth is valuation discipline. AMD, Micron and Sandisk can be real AI winners and still become poor entries after a parabolic run. Good businesses do not protect investors from paying the wrong price.

The Bottom Line

AI infrastructure remains one of the strongest themes in the market. The problem is that the stocks have started to behave as if the supply squeeze, customer urgency and margin expansion will continue almost uninterrupted.

That may happen for longer than skeptics expect. But after the moves in Sandisk, Micron, AMD and AAOI, investors should stop asking only which companies benefit from AI. The more useful question is which stocks still offer enough margin of safety if the next data point is merely good instead of perfect.

FAQ

Frequently asked questions

Are AI stocks in a bubble after the 2026 infrastructure rally?

AI infrastructure demand is real, but some supplier stocks now price in years of strong capex, tight supply and high margins, which raises correction risk.

Why are Sandisk and Micron tied to AI demand?

Sandisk sells NAND flash storage and Micron sells memory and storage products used across data-center and AI workloads, making both sensitive to AI infrastructure demand and memory pricing.

Why is AAOI riskier than larger AI chip stocks?

Applied Optoelectronics has strong exposure to AI data-center optics, but it is smaller, still reported a GAAP net loss in Q1 2026 and is ramping capacity into a fast-moving demand cycle.

Is AMD safer than Sandisk, Micron or AAOI?

AMD is larger and more diversified than many smaller AI infrastructure names, but its stock can still fall if investors reduce the multiple they are willing to pay for future AI revenue.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Naba Fatima reviews consumer technology for TECHi — phones, laptops, wearables, and the streaming and smart-home ecosystems built around them. She tests devices on daily-driver cycles rather than spec-sheet skims, cross-references durability and repairability data from iFixit and JerryRigEverything, and prioritizes what actually matters after the unboxing weekend: battery longevity, software-update cadence, repair cost, and resale value. Her reviews stay skeptical of launch-day marketing.