SanDisk ended the first half of 2026 as the best-performing stock in the S&P 500, up 858% — from a $237.38 close on December 31 to $2,273.73 on June 30. Two sessions later, $529 of that share price was gone. Thursday's 14.1% drop — the stock's biggest one-day fall since early February — capped a 23.3% two-session slide and sent SanDisk into the July 4th weekend at $1,745, with US markets shut until Monday, July 6.

What changed is the question being asked of the stock. For six months the SanDisk debate was about momentum: how far a NAND shortage could carry a company most investors did not own seventeen months ago. After Thursday it is an underwriting problem — what exactly do the contracts, the margins and the customer list support at a $258 billion valuation, and what has to stay true between now and the August report?

- The half-time scoreboardSanDisk's +858% first half was the best of any S&P 500 stock — and even after the 23.3% two-session crash, it enters the weekend up 635% for 2026 at $1,745.

- Perspective on the crashJuly 2's -14.1% was the seventh-worst day since the February 2025 spin-off and the biggest since early February 2026 — painful, but not unprecedented for this stock.

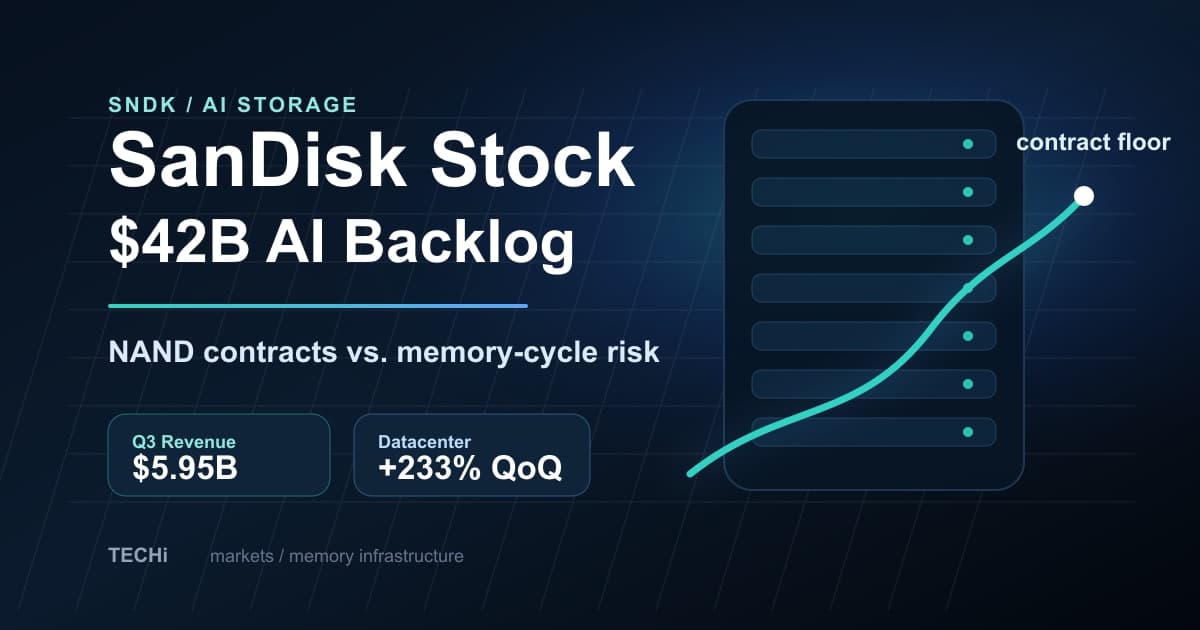

- The backlog is real but bandedThe 10-Q shows $41.6B in remaining performance obligations with over $11B in guarantees — but near-term prices are fixed while outer years float inside floor-and-ceiling bands.

- The named risk is YMTCBank of America calls fresh supply the one thing that could unwind NAND pricing early; YMTC's third Wuhan fab starts late 2026, with meaningful bits unlikely before 2028 per DigiTimes.

- Three checkpoints aheadMonday's July 6 reopen, the ~July 9-10 short-interest print, and the fiscal Q4 report expected August 13 — with two undisclosed contract minimums due in the next filing.

From castoff to index leader in seventeen months

The stock's origin story matters, because it explains both the size of the run and the violence of the unwind. Western Digital did not spin SanDisk off from strength: activist Elliott Management spent two years arguing that the flash business was worth more outside, and when the separation completed in February 2025, the market's first verdict was a 7% markdown — a $52.00 open on February 24, a $48.60 close. Six weeks later, in the April 2025 tariff panic, the shares traded below $28 intraday. From that low to the June 22 intraday record of $2,354.39 is roughly an 84-fold move; from the first-day close, about 36-fold.

Nor is SanDisk alone at the top of the index. MarketWatch's half-year leaderboard reads like a memory-industry org chart: Micron second at +304%, Intel third at +278%, Western Digital — the parent that let SanDisk go — fourth at +271%, Marvell fifth at +251%, Seagate sixth at +250%. The divorce made both sides rich, and the shortage TECHi has tracked since the spring made the whole supply chain the market's leadership group. That concentration cuts both ways: when the AI-memory trade wobbled last week, there was nowhere in the group to hide.

Seven sessions that changed the question

The sequence reads like a different market each morning. June 24: minus 2.5%. June 25: plus 22% after Micron reported a $41 billion quarter and Citi raised its SanDisk target from $2,025 to $2,500. June 26: minus 10.5% on profit-taking. June 29: minus 1.9% as Korea unveiled its ₩800 trillion fab program. June 30: plus 10.9% to the record close, after Bernstein's Mark Newman lifted his target from $1,700 to $3,000 — 11 times his fiscal-2028 earnings estimate of $272 a share. July 1: minus 10.6%, the day Michael Burry's semiconductor puts and a fresh $2,500 Bank of America target landed within hours of each other. July 2: minus 14.1%, as glut fears swept the entire memory complex — on 57% higher volume, with an intraday low of $1,693.

Keep the damage in perspective: July 2 was SanDisk's seventh-worst session as a public company, not its worst, and the biggest drop only since February 4. But one detail separates this week from every previous swing. SanDisk itself said nothing. Every one of those moves was someone else's headline — Micron's numbers, three banks' models, Burry's puts, Korea's fabs, Meta's cloud plans. When a stock's daily direction is set entirely by other people's news, the market is telling you it has not settled what the company is worth.

What $258 billion buys

Start with what the company last put on the record. Fiscal third-quarter results, reported April 30: revenue of $5.95 billion, up 251% year over year, against guidance of far less; non-GAAP gross margin of 78.4% versus the 65–67% guided; earnings of $23.41 a share against a $12–14 forecast. Datacenter revenue reached $1.47 billion — up 233% sequentially, a quarter of total revenue after being a tenth the quarter before, driven by enterprise SSDs for AI inference. For the June quarter, management guided to $7.75–8.25 billion in revenue at 79–81% gross margin and $30–33 in earnings per share.

Against those numbers, $1,745 is two different stocks depending on the denominator. On this fiscal year's consensus earnings of $65.48, per StockAnalysis.com, it trades at roughly 27 times — a premium multiple for a memory company by any historical standard. On Bank of America's calendar-2027 estimate of $252 — the same number the bank multiplies by ten to justify its $2,500 target — it trades at 6.9 times. Both statements are simultaneously true. The 27x says perfection is still priced in; the 6.9x says a full downturn already is. Which multiple is the real one depends entirely on whether next year's earnings survive contact with next year's supply — which is why the backlog deserves a closer read than it usually gets.

Read the backlog like a contract, not a headline

The headline number is $42 billion. The April 10-Q puts remaining performance obligations at $41.6 billion — $41.2 billion of it unbilled — and that covers only the three long-term agreements signed during the third quarter. Two more were signed early in the fourth quarter; their minimums have not been disclosed yet. Only about 15% of the obligation converts to revenue within twelve months. This is multi-year architecture, not next quarter's order book.

The protections are real but bounded. Financial guarantees across the five agreements exceed $11 billion — prepayments and instruments held with third-party financial institutions that trigger if a customer misses a quarterly purchase commitment. CFO Luis Visoso, describing the mechanics at a JPMorgan conference, put it plainly: "No lawsuits, no discussions. It's just a very simple procedure." The same filing is equally plain in the other direction: the guarantees "may not fully offset" lost revenue depending on when in the contract term a customer walks.

And the pricing is not what "locked in" implies. Near-term prices are largely fixed; outer years carry variable components inside floor-and-ceiling bands — "We know one of us is going to be unhappy if we fix the price," in Visoso's words. CEO David Goeckeler says the agreements cover more than a third of fiscal 2027 bit supply and "can get above 50%." Concentration comes with it: the top ten customers were 46% of third-quarter revenue, and one unnamed customer alone crossed 10%. The honest summary is that the backlog TECHi examined in June locks volume and price floors, not tomorrow's spot price. It converts NAND's classic bust mechanism from a revenue cliff into a margin negotiation. No prior NAND cycle had anything like it — and no downturn has tested it.

The bear case with names attached

The serious bear case is not the two-day headline scare. It has a name: YMTC. In the same note that raised his target, Bank of America's Wamsi Mohan called fresh supply "the one thing that could unwind NAND pricing faster than the bulls expect," and China's national flash champion is the source. YMTC runs two Wuhan fabs at roughly 200,000 wafers a month and plans three more toward a ~500,000 target, with the third fab starting production late this year; UBS pegs its 2025 share of the NAND market at 11.8%, per the same Reuters reporting. Washington's Entity List slows the ramp — but with more than half the new fab's tools sourced domestically, it no longer caps it. DigiTimes' assessment is that meaningful new bits are unlikely before 2028; Mohan's base case assumes YMTC stays focused on China's domestic market. Those two hedges are carrying a lot of weight at $258 billion.

Structure compounds the risk. NAND is a six-supplier market where DRAM is effectively three, and its supply has historically been elastic — layer stacking adds bits without proportional capex — which is why NAND booms have died faster and uglier than DRAM ones. The counterpoint from the same analysis: stacking economics are eroding, so the classic overshoot mechanism is weaker this cycle than in any prior one.

Someone is betting on the bust in size. Short interest reached 10.9 million shares — 7.38% of the float, about $23 billion worth — at the June 15 settlement, up 18.5% in two weeks. That position was built before the crash, not after it. What the bears no longer have are the mechanical overhangs: the "billionaires are dumping" story from the spring — the one TECHi covered in April — ended with Stanley Druckenmiller buying back in during the first quarter after his celebrated exit at far lower prices, and Western Digital's retained stake — the one genuine supply overhang — was sold in February at $545 a share, absorbed by the market a thousand dollars ago. Insider filings this year show routine, plan-based sales in the hundreds of shares, not an exit. If you want to be bearish here, it has to be about 2027 supply. The easy arguments are used up.

The checkpoints between here and August 13

Where does the Street actually stand after the crash? The three most recent target changes — Citi to $2,500 on June 25, Bernstein to $3,000 on June 30, Bank of America to $2,500 on July 1 — all landed within six sessions of the top, and as of Friday morning no post-crash note, defense or downgrade had been published. Consensus depends on who is counting after a vertical rally: StockAnalysis.com's 22-analyst average sits near $1,864 with a $1,701 median, zero Sells and one lone Strong Sell. The most recent targets say the crash is noise; the trailing consensus says the crash was overdue. Nobody has updated for it yet.

Monday's reopen starts the clock on three checkpoints. First, whether US memory names follow the Korean rebound that played out while Wall Street was closed, or extend Thursday's break. Second, the next FINRA short-interest settlement, published around July 9–10, which will show whether the $23 billion short position pressed into the crash or covered into it. Third — the one that actually matters — the fiscal fourth-quarter report, expected August 13 per earnings calendars: the $7.75–8.25 billion guidance test, the first margin print of the new contract era, and the promised disclosure of the two newest supply agreements' minimums, which would put a number on how much bigger than $42 billion the committed book really is.

The first half was a momentum story that nobody fully modeled. The second half is an underwriting story that everyone now has to. At 6.9 times Bank of America's 2027 estimate, Thursday priced in a downturn; at 27 times this year's consensus, it still prices in something close to perfection. Both are true at once — and that contradiction, not the glut headlines, is why the tape has turned this violent.

Investment Disclaimer: This article is for informational and educational purposes only. It is not financial advice and should not be construed as a recommendation to buy, sell, or hold any security. Figures reflect company disclosures, SEC filings, TECHi market data, and public sources available at the time of drafting. Market data may be delayed, cached, or revised. Always conduct your own due diligence and consult a licensed financial advisor before making investment decisions.

FAQ

Frequently asked questions

Why did SanDisk stock fall 14% on July 2, 2026?

SanDisk fell 14.1% to $1,745 as glut fears swept the AI memory complex — triggered by South Korea's 800 trillion won fab program, Michael Burry's semiconductor shorts, and Bloomberg's report that Meta plans to sell excess AI compute. It was SanDisk's seventh-worst session since its February 2025 spin-off and its biggest one-day drop since early February 2026. The company itself reported no news.

Is SanDisk still the best-performing S&P 500 stock of 2026?

Through the official first half it was: +858% from December 31 to June 30, ahead of Micron at +304%, Intel at +278%, and Western Digital at +271%, per MarketWatch's leaderboard based on June 30 closes. Even after the two-day crash, SanDisk entered the July 4th weekend up 635% for the year.

How solid is SanDisk's $42 billion backlog?

The April 10-Q shows $41.6 billion in remaining performance obligations from three long-term agreements, with over $11 billion in financial guarantees that trigger if customers miss quarterly commitments; two additional agreements' minimums have not yet been disclosed. Volume is locked, but pricing is only fixed near term — outer years carry variable components within floor-and-ceiling bands, so committed revenue can reprice in later years.

What are analyst price targets for SanDisk after the crash?

No analyst had published a post-crash update as of Friday morning, July 3. The three most recent actions were Citi at $2,500 (June 25), Bernstein at $3,000 (June 30), and Bank of America at $2,500 (July 1). StockAnalysis.com's broader 22-analyst average sits near $1,864 with a median of $1,701, reflecting targets set before the vertical rally.

When does SanDisk report earnings next?

The fiscal fourth-quarter report is expected around August 13, 2026, per earnings calendars. Guidance to beat: $7.75–8.25 billion in revenue, 79–81% non-GAAP gross margin, and $30–33 in earnings per share — plus the promised disclosure of minimum revenue from the two newest supply agreements.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

CEO of TECHi. Building the operating system for serious tech investors. Previously led engineering at scale. Focus: AI capex thesis, semiconductor supply chain, and the equity tape.