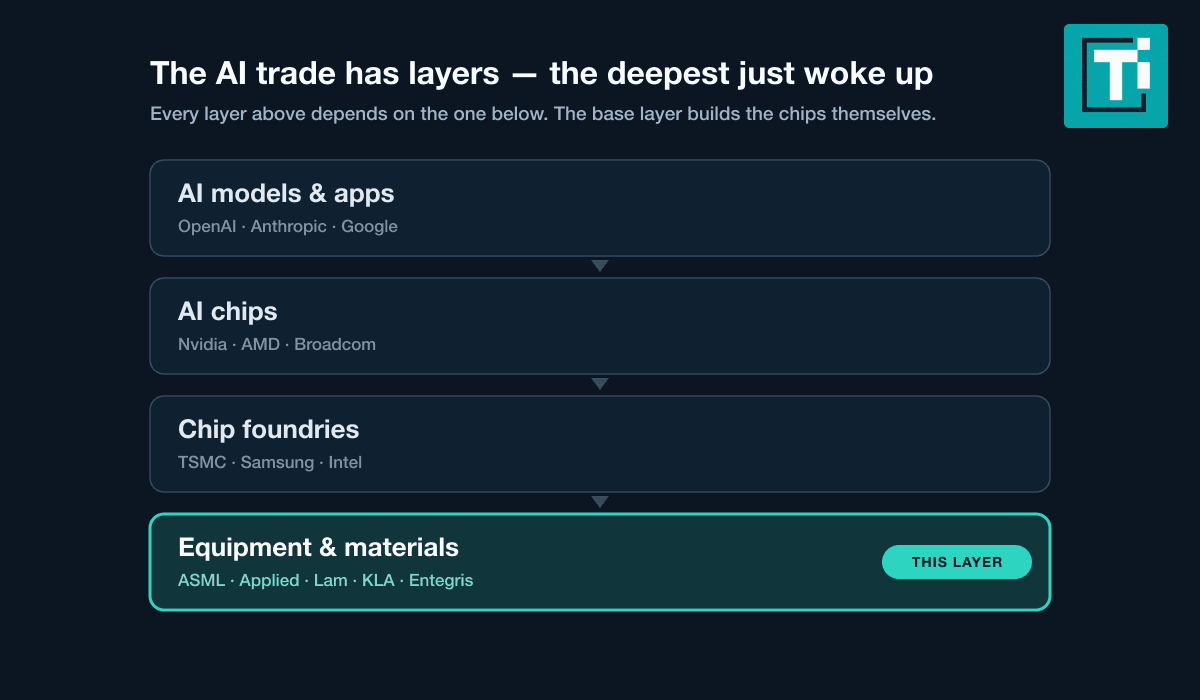

- The setupASML, Applied Materials, Lam Research and KLA cover four critical lanes in memory manufacturing: lithography, materials engineering, etch and deposition, and process control.

- The logicToolmakers get paid when fabs are built, not when chip prices hold. Order books follow capital-spending commitments, which run on next year's forecast.

- The AI kickerHBM adds equipment-intensive through-silicon-via and advanced-packaging steps on top of the DRAM process.

- The buyersSK Hynix, Samsung and Micron fund the capacity race; each expansion draws on the same core equipment categories, though vendor share differs by process and fab.

- The catchEquipment is among the first spending lines memory makers can defer in a downturn, so suppliers can suffer severe drawdowns when capacity plans change.

This article is for information only and is not investment advice. Equipment stocks are among the most cyclical in the market — verify live prices and current filings before making any investment decision.

Every gigabyte of AI memory starts life in a fab full of specialized machines. Before SK Hynix can stack a layer of HBM4, before Micron can ship high-bandwidth DRAM, manufacturers need etchers, deposition chambers, lithography scanners and inspection systems to do the physical work. This guide follows four listed leaders across those critical lanes. In a cycle where memory prices can whipsaw week to week, their orders and installed-base activity help show what the industry is actually preparing to build.

That gap between what chips cost and what chipmakers spend is the whole story. Memory equities fell into a bear market at the start of July while record-scale memory capex was being financed the same week — SK Hynix’s prospectus estimated roughly $28 billion in net proceeds and said the money would support general corporate purposes, including capital expenditures. Prices said fear. The filing said build. The toolmakers get paid on the second signal.

The four companies that build the machines

Wafer-fab equipment is a concentrated market, but it is not a four-company monopoly. ASML, Applied Materials, Lam Research and KLA have different strengths across lithography, materials engineering, etch and deposition, and process control; their portfolios overlap at the edges and other suppliers matter. The useful comparison is not who owns every tool. It is which part of a memory expansion each company can monetize, and what evidence would show that spending lane accelerating or stalling.

ASML (ASML)

Everything begins with lithography — projecting the circuit pattern onto the wafer — and ASML is the only company on Earth that ships the extreme-ultraviolet machines advanced chips require. Memory has historically leaned on EUV less than logic, but that changes with every DRAM generation: the tighter the pitch, the fewer tricks remain besides better optics. ASML's backlog is the industry's longest-dated commitment to the future, which is why its earnings reports get read like macro data for the whole chip complex.

Applied Materials (AMAT)

Applied Materials has the broadest catalog in the business — deposition, ion implant, polishing, and an expanding advanced-packaging line. Breadth makes it the diversified bet: no single process step can sink it, and its management commentary tends to describe the whole spending environment rather than one niche. When Applied's chief executive talks up a multi-year boom, as he did during Lam's July repricing week, he is describing the tide, not one boat.

Lam Research (LRCX)

Lam Research is the memory pure-play of the group. Etch and deposition — carving structures and layering films — are the two steps that dominate a memory fab's tool budget, and Lam leads both. High-bandwidth memory adds a third: the thousands of through-silicon vias drilled through each HBM stack are an etch problem, squarely in Lam's toolbox. That concentration is why Lam gained 154% in the first half of 2026 without selling a single chip — TECHi's breakdown of the repricing argument now running in the stock covers the $348 consensus versus the $475 fresh marks — and why it falls hardest when a memory maker so much as hints at deferring a fab.

KLA (KLAC)

KLA gets paid to find mistakes. Its metrology and inspection systems measure whether the other three companies' machines did their jobs, and its economics improve as processes get harder — more layers and tighter tolerances mean more measurement per wafer, not less. Yield is the difference between a profitable memory fab and an expensive science project, which makes KLA the closest thing the group has to a recurring-revenue story.

Why memory is the tool-hungry end of the business

Memory scaling stopped being about shrinking a flat design years ago. NAND now goes up instead of out — flagship parts stack well over 200 layers of storage cells, and every added layer is another deposition pass and another high-aspect-ratio etch, like drilling an oil well the width of a virus. DRAM keeps shrinking, but each node needs more patterning steps to get there. And HBM, the stacked DRAM feeding every AI accelerator, bolts an entire packaging flow on top: drill the vias, fill them with copper, thin the wafer, stack the dies, test the tower.

The structural point is that advanced memory adds process steps and tighter tolerances even as manufacturers work to lower cost per bit. AI has accelerated that workload: Samsung says its commercial HBM4 runs at 11.7 Gbps, 1.22 times the maximum pin speed it cites for HBM3E, and the company is expanding HBM4 production capacity. That is a performance and capacity signal, not a promise that every equipment order arrives on schedule.

The buyers: three companies, one arms race

The customer list is as concentrated as the supplier market. SK Hynix financed its next capacity leg at record scale. Samsung has begun mass production and commercial shipments of HBM4. And Micron’s May 2026 quarterly filing says the company will need new DRAM wafer capacity to support projected demand in the second half of the decade. These manufacturers compete for memory share, but each expansion still requires lithography, materials processing, etch, deposition and yield control.

That common process stack is the toll-booth logic. A share fight among the large memory producers can redirect which fab receives the next machine, but it does not remove the need for the machine categories themselves. The four companies in this guide are not interchangeable and do not capture every dollar; they offer four different windows into the same capacity race.

How the cycle pays — and how it ends

The honest version of this story includes the ending. Equipment orders lead memory prices in both directions: fabs are financed on next year’s demand forecast, so the order book can turn before the spot market does. When a memory maker facing softer prices defers a fab, the supplier loses that expected revenue rather than merely accepting a lower chip price. That is why equipment stocks can suffer severe drawdowns even when the long-run technology roadmap remains intact.

The glut question is therefore the equipment question. TECHi’s July capacity analysis works through whether AI demand can absorb the fabs being financed. The mid-July tape showed how quickly expectations can move: memory and equipment shares sold off together even while official filings still pointed to large capital programs. One synchronized move does not prove a shared cause, but it does show investors marking down future purchase-order confidence rather than current factory shipments. That asymmetry — first paid, first cut — is the price of the toll booth.

A four-signal scorecard for the next order cycle

ASML provides the longest-dated signal. Its 2025 annual report said memory momentum was being fueled by HBM and DDR5 investment, while management expected EUV revenue to rise significantly in 2026 because of advanced logic and DRAM demand. Read that combination carefully: system sales show customers committing to new process capacity, while service and field-option growth shows how hard the installed base is being run. A healthy memory build should eventually show up in both. If HBM headlines stay loud but DRAM-related EUV demand or utilization weakens, the spending cycle is less broad than the narrative suggests.

Applied Materials and Lam reveal where the process becomes more equipment-intensive. Applied’s June 2026 product release added DRAM epitaxy, packaging deposition and polishing, plus e-beam defect review aimed at HBM and 3D stacking. Lam’s own process roadmap says the move toward 3D NAND, DRAM and packaging demands deeper etch and more precise deposition, with HBM already demonstrating the shift. Those are separate revenue lanes, not interchangeable buzzwords. Applied is the broader basket; Lam is the sharper exposure to etch and deposition intensity. Investors should watch whether customer commentary turns those announced tools into sustained production ramps, because a technically important process does not guarantee a purchase order on the expected timetable.

KLA supplies the yield check. In its December 2025 quarterly filing, the company tied higher semiconductor-process-control revenue to memory customers, especially DRAM, advanced packaging and a larger installed base. Inspection spending matters because a taller stack is valuable only if enough good die survive each added process step. That makes KLA’s mix a useful confirmation signal: rising memory and packaging revenue supports a real factory ramp; service growth without comparable product demand can point to customers sweating tools they already own. The field-guide thesis weakens if official reports show DRAM and packaging orders flattening together, customer capex slipping, or new process launches failing to convert into volume production.

What would break the toolmaker thesis

- WFE guidance, not EPS. At equipment earnings, the number that moves the group is the industry-wide wafer-fab-equipment spending forecast, and each management's memory-versus-logic mix commentary.

- HBM supply contracts. Multi-year supply deals between memory makers and AI chip designers are the demand signal that de-risks fab construction — and triggers tool orders.

- Capex announcements from the big three. SK Hynix, Samsung and Micron publish capital-spending plans; revisions in either direction hit the toolmakers before they hit memory prices.

- China and export rules. A meaningful slice of every toolmaker's revenue depends on what Washington allows to ship east; rule changes reprice the group overnight.

- The packaging line item. Advanced packaging is the fastest-growing tool category of the AI era — it is where HBM demand shows up first in equipment revenue.

FAQ

Frequently asked questions

What is AI memory equipment?

AI memory equipment includes the wafer-fab and packaging systems used to manufacture DRAM, NAND and high-bandwidth memory (HBM): lithography scanners, deposition and etch tools, and metrology and inspection systems. This guide focuses on four listed leaders across those lanes: ASML, Applied Materials, Lam Research and KLA.

Which company is the purest play on AI memory equipment?

Lam Research is one of the sharpest listed exposures to memory process intensity because its etch and deposition tools are heavily used in advanced DRAM, NAND and packaging flows. That concentration also raises the downside if customers defer memory capex.

Why do equipment stocks move more than memory stocks?

Because equipment orders run on future capacity plans, not current chip prices. Fabs are financed on next year's forecast, so the order book turns before the spot market in both directions — equipment makers get paid first in a boom and cut first in a downturn.

Who buys AI memory equipment?

The largest DRAM buyers are SK Hynix, Samsung and Micron, alongside NAND producers. Their fabs rely on the same core equipment categories and frequently on the four suppliers covered here, although vendor share differs by process and facility.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

CEO of TECHi. Building the operating system for serious tech investors. Previously led engineering at scale. Focus: AI capex thesis, semiconductor supply chain, and the equity tape.