- No public stock yetOpenAI has no ticker, no public S-1, and no confirmed IPO date. The filing is the starting gun.

- The latest catalystThe Microsoft amendment made OpenAI easier to value as a stand-alone business, but the relationship remains complex.

- The private mark is hugeOpenAI has already disclosed an $852 billion post-money valuation and $2 billion of monthly revenue.

- The S-1 will decide the debatePublic investors still need audited revenue, gross margin, loss profile, governance terms, contract obligations, and float.

- Retail access is limitedMost investors should treat indirect exposure and private-market funds as different products from owning OpenAI common stock.

OpenAI is not a public stock yet. There is no ticker, no public S-1, and no confirmed IPO date as of May 6, 2026. But the IPO story is no longer vague startup gossip. OpenAI has now disclosed a $122 billion funding round at an $852 billion post-money valuation, says it is generating $2 billion in revenue per month, and has revised the Microsoft partnership that used to be one of the biggest structural questions around a future listing, according to OpenAI's April partnership update and Microsoft's matching announcement.

The better investor question is not "when can investors buy OpenAI stock?" It is whether the business can grow into a valuation that private investors have already marked like a mega-cap platform. The answer depends on five things public investors still cannot see: audited revenue, gross margin after compute costs, contract obligations, governance rights, and the amount of stock that insiders and late private investors may sell when liquidity finally opens.

OpenAI IPO Status Today: No S-1, But The Setup Is Getting Clearer

OpenAI has not filed a public IPO registration statement with the SEC, and the SEC tells investors that IPO registration statements and amendments are made available through EDGAR when a company files them. Until OpenAI files an S-1, investors do not have the audited financial statements, risk factors, underwriter list, share count, lockup terms, or use-of-proceeds language that normally define a real IPO analysis.

That is why the April 27 Microsoft amendment matters. Microsoft said OpenAI products will still ship first on Azure when Azure can support the needed capabilities, but OpenAI can now serve all of its products to customers across any cloud provider. Microsoft also said its OpenAI IP license runs through 2032 and is now non-exclusive, while Microsoft will no longer pay a revenue share to OpenAI and OpenAI's revenue-share payments to Microsoft continue through 2030 subject to a cap.

OpenAI described the same agreement as a way to give both companies more flexibility. The company said Microsoft remains its primary cloud partner, OpenAI can serve products across any cloud provider, and Microsoft continues to participate directly in OpenAI's growth as a major shareholder.

The earlier Microsoft-OpenAI restructuring is still the foundation of the IPO case. In October 2025, OpenAI said Microsoft held an investment in OpenAI Group PBC valued at roughly $135 billion, representing about 27% on an as-converted diluted basis. OpenAI also said it had contracted to buy an incremental $250 billion of Azure services, while Microsoft no longer had a right of first refusal to be OpenAI's compute provider.

AP framed the April amendment as a meaningful step toward loosening the alliance. It reported that OpenAI is balancing Microsoft with other cloud partners including Amazon, Google and Oracle, and cited Wedbush analyst Dan Ives saying the deal puts OpenAI on a stronger path toward going public because it reduces barriers from the original Microsoft partnership.

The newest May data point is governance, not a ticker. AP reported on May 4 that OpenAI president Greg Brockman disclosed in court that his OpenAI stake is worth nearly $30 billion, during a trial focused on OpenAI's evolution from a nonprofit startup into a company valued at $852 billion. That does not make an IPO imminent, but it tells investors the public-market debate will include control, insider economics, and mission structure as much as revenue growth.

The Business Is Already IPO-Sized

OpenAI's March 31 funding update is the closest thing investors have to a draft S-1 narrative. The company said it closed $122 billion of committed capital at an $852 billion post-money valuation. That update also said OpenAI reached $1 billion of revenue within a year of launching ChatGPT, reached $1 billion per quarter by the end of 2024, and is now generating $2 billion per month.

The customer scale is just as important as the valuation. OpenAI said ChatGPT has more than 900 million weekly active users and over 50 million subscribers, while its API processes more than 15 billion tokens per minute. The company also said enterprise now represents more than 40% of revenue and is on track to reach parity with consumer revenue by the end of 2026.

OpenAI had already disclosed the first stage of the funding wave on February 27. In that announcement, the company said it secured $110 billion of new investment at a $730 billion pre-money valuation, including $50 billion from Amazon, $30 billion from NVIDIA, and $30 billion from SoftBank. OpenAI also said it had more than 9 million paying business users and more than 50 million consumer subscribers.

AP's funding report independently confirmed the same $110 billion round, the $730 billion pre-money valuation, the $50 billion Amazon commitment, and the $30 billion commitments from NVIDIA and SoftBank. That matters because OpenAI's IPO story is not built only on ChatGPT subscriptions. It is built on a capital stack where cloud providers, chip suppliers, venture firms, asset managers, and strategic partners all have reasons to keep OpenAI scaling.

The Microsoft Deal Makes OpenAI Easier To Value, Not Easy To Value

The post-amendment structure is cleaner than the old one, but it is still not simple. OpenAI remains tied to Microsoft through Azure, IP rights, revenue sharing, and equity ownership. Microsoft remains a major shareholder, and OpenAI still has a giant Azure purchase commitment from the October 2025 agreement.

For background on why that relationship matters to public-market investors, TECHi's Microsoft and OpenAI investment breakdown explains how Microsoft's early capital and Azure relationship turned OpenAI into one of the most important private assets in big tech.

For a public-market investor, that creates a mixed signal. The bullish read is that OpenAI now has more freedom to buy compute, distribute products, and work with other partners. The cautious read is that the company still has a complex commercial relationship with one of the most important public AI platforms in the world.

OpenAI's own March update shows why flexibility matters. The company said its infrastructure strategy now spans cloud relationships with Microsoft, Oracle, AWS, CoreWeave, and Google Cloud, while its silicon strategy includes NVIDIA, AMD, AWS Trainium, Cerebras, and an OpenAI chip partnership with Broadcom. That is the footprint of an AI infrastructure company, not only a chatbot company.

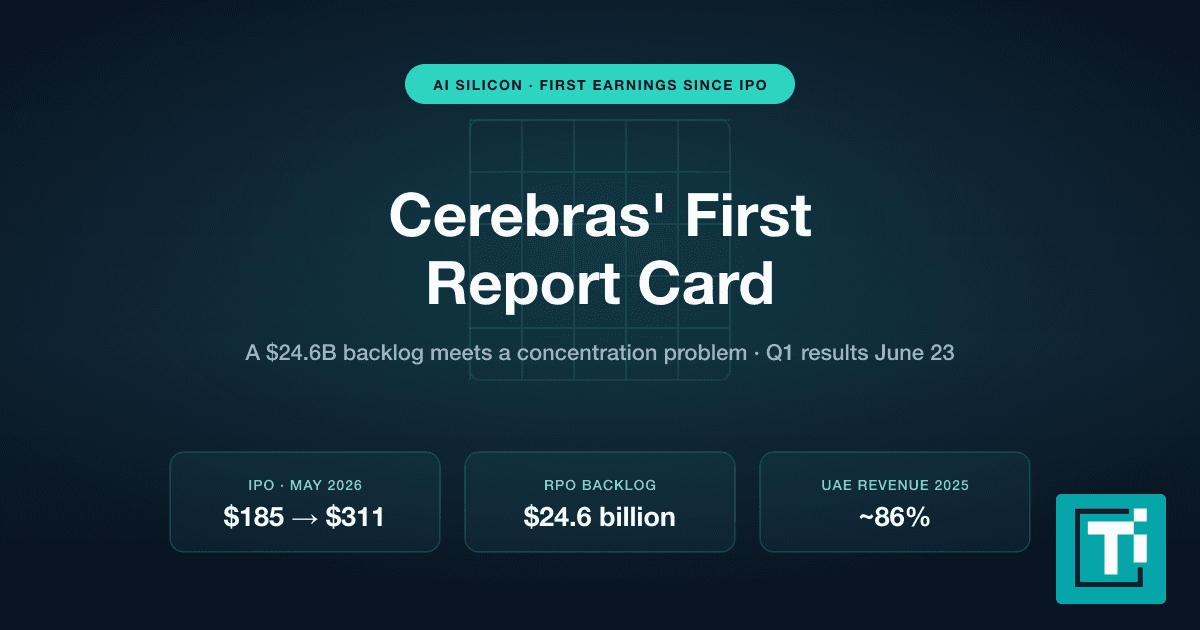

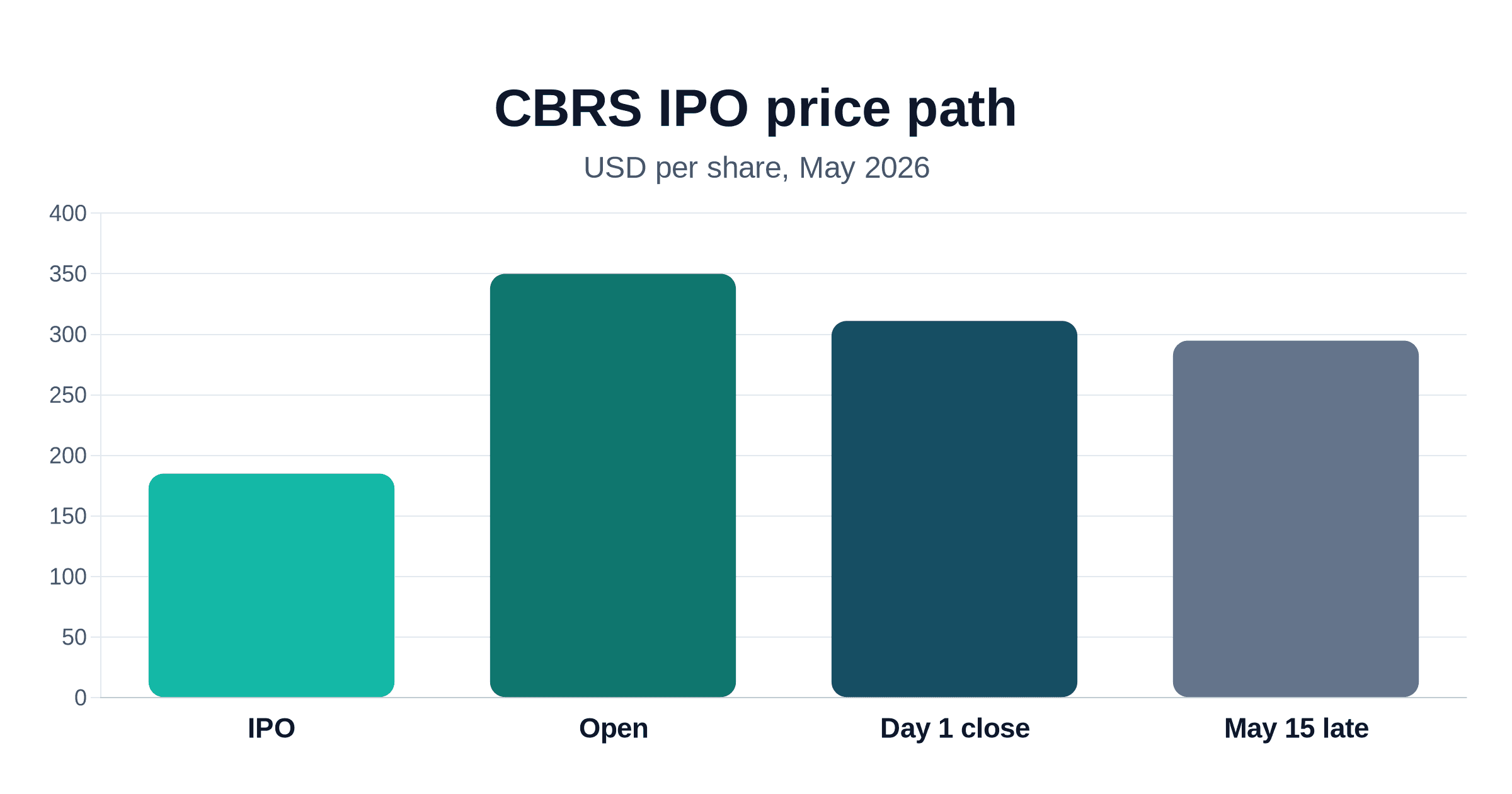

This is also why investors should read TECHi's Cerebras IPO analysis. Cerebras is a public-market test case for OpenAI's compute ecosystem because Cerebras has filed an S-1 for its own IPO and says it plans to offer 28 million Class A shares. The SEC filing includes OpenAI-related references, which means parts of the OpenAI infrastructure chain are already being tested by public investors before OpenAI itself lists.

The Valuation Is The Hard Part

An $852 billion private valuation is not a normal startup mark. It puts OpenAI in the zone where public investors will demand proof that the company can compound revenue while converting more of that revenue into durable margin.

The SEC's IPO investor bulletin tells investors to read the prospectus carefully, including risks, management discussion, financial statements, and offering terms. For OpenAI, that warning is not boilerplate. The prospectus will need to explain how the company recognizes revenue across ChatGPT, enterprise contracts, API usage, agents, ads, and cloud-linked partnerships. It will also need to explain how much of OpenAI's revenue is consumed by inference costs, training costs, chip commitments, data-center contracts, partner payments, and stock-based compensation.

The public-benefit structure is another valuation variable. OpenAI says the for-profit entity is now OpenAI Group PBC, the nonprofit is now the OpenAI Foundation, and the Foundation continues to control OpenAI Group through special voting and governance rights. OpenAI also says the Foundation holds a 26% equity stake worth about $130 billion, Microsoft holds roughly 27%, and the remaining 47% is held by current and former employees and investors.

That structure may help preserve OpenAI's mission, but it also means public investors will have to understand who controls board appointments, how mission obligations interact with shareholder returns, and what rights new IPO buyers actually receive. OpenAI's charter says its mission is to ensure that AGI benefits all of humanity, which is an unusual mandate for a company that may ask public investors to value it near the top of global equity markets.

Can Regular Investors Buy OpenAI Before The IPO?

Most investors still cannot buy OpenAI common stock directly. OpenAI did say it raised more than $3 billion from individual investors through bank channels, and Axios reported that those allocations were tied to clients of three large banks as part of the broader $122 billion round. OpenAI also said its shares will be included in several exchange-traded funds managed by ARK Invest.

ARK's own Venture Fund portfolio page listed OpenAI as a private startup in the portfolio as of April 30, 2026, and ARK's first-quarter update said the fund added to existing OpenAI positions during the quarter. For investors who want the mechanics, TECHi's guide to investing in OpenAI before its IPO explains the ARK route, the limits of private-market access, and the difference between direct ownership and fund-level exposure.

Private access is not the same thing as public liquidity. The SEC says many private-market exemptions are limited to accredited investors or restrict non-accredited participation, and it defines individual accredited investor thresholds around net worth, income, or financial sophistication. That means secondary-market pitches around OpenAI stock should be treated carefully. The more exciting the company becomes, the more important it is to verify the vehicle, fees, liquidity, valuation mark, and whether the investor actually owns OpenAI exposure or only a fund that owns it.

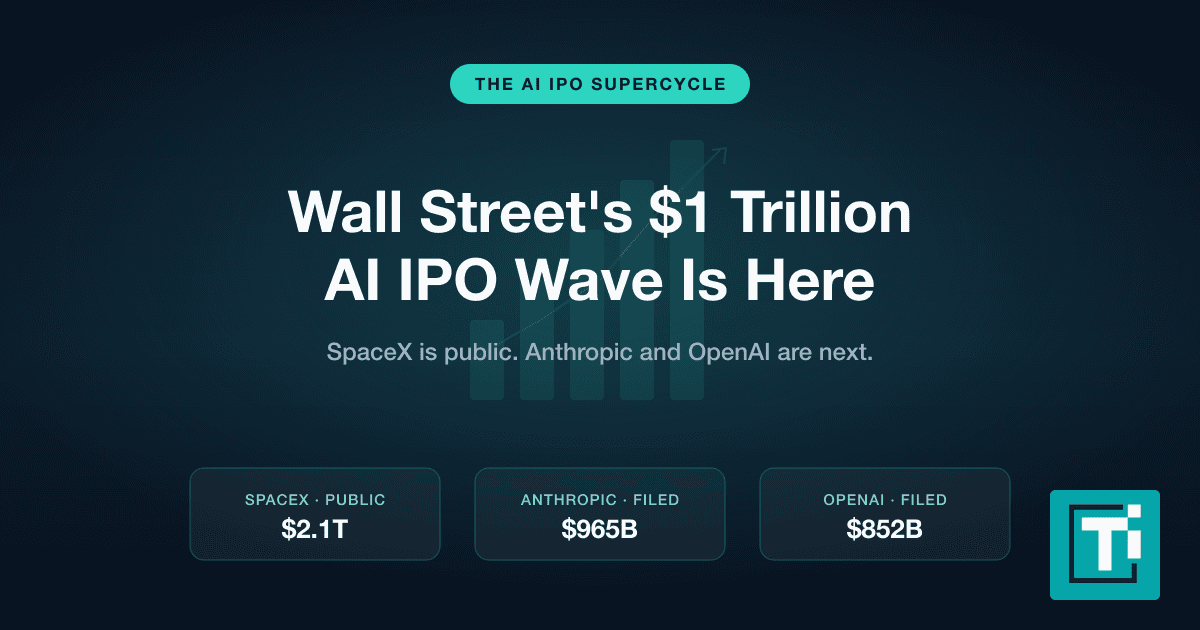

How OpenAI Compares With Anthropic, SpaceX And Cerebras

OpenAI is not the only private company pulling public-market gravity toward 2026. Anthropic said it raised $30 billion at a $380 billion post-money valuation in February, and TECHi's Anthropic IPO analysis covers why Claude's enterprise momentum could make it OpenAI's cleanest public-market comparison. The key difference is that OpenAI has consumer scale first and enterprise growth second, while Anthropic's investor case is more tightly tied to enterprise AI and coding.

SpaceX is a different kind of comparison. TECHi's SpaceX IPO guide is useful because SpaceX shows what happens when a private company becomes too important for public investors to ignore before it lists. OpenAI is moving toward the same problem, but through AI infrastructure, enterprise software, consumer subscriptions, and developer APIs rather than rockets and satellite broadband.

Cerebras is the near-term market signal to watch. Cerebras announced that it plans to start the roadshow for an IPO after filing a registration statement, and its deal flow is tied directly to AI compute demand. If public investors reward Cerebras at a rich multiple, that helps the OpenAI ecosystem narrative. If they punish concentration risk, unproven margins, or customer complexity, OpenAI's own IPO bankers will notice.

What Investors Should Watch Next

The first real milestone is the S-1. Do not treat a rumored ticker, a banker leak, or a private valuation screenshot as a filing. The S-1 available through SEC EDGAR is where OpenAI will have to show audited financial statements, revenue mix, risk factors, related-party transactions, material contracts, and the exact capital structure being sold to public investors.

The second milestone is gross margin. OpenAI's revenue number is now large, but AI inference economics are not classic SaaS economics. OpenAI says durable access to compute is a strategic advantage, yet the same compute footprint can also suppress margin if usage grows faster than efficiency gains.

The third milestone is partner concentration. OpenAI is spreading across Microsoft, Oracle, AWS, CoreWeave, Google Cloud, NVIDIA, AMD, AWS Trainium, Cerebras, and Broadcom, according to OpenAI's March update. That breadth reduces single-vendor dependency, but it also creates execution complexity that will be much easier to judge once public investors see contract terms.

The fourth milestone is governance. OpenAI's nonprofit control model is part of its identity, and the company says the OpenAI Foundation appoints all OpenAI Group board members and can replace directors at any time. IPO buyers will need to know whether they are buying economic exposure, governance influence, or a mostly economic claim under mission-first control.

The fifth milestone is float. A company this heavily owned by strategic partners, employees, private funds, and late-stage investors can trade very differently depending on how much stock is sold in the IPO and how much becomes available after lockups expire.

The Bottom Line On The OpenAI IPO

OpenAI is closer to IPO-ready than it was two months ago, but it is not investable as a public stock yet. The Microsoft amendment reduced a major structural overhang. The March funding round put an $852 billion valuation marker in the market. The user and revenue numbers are already enormous. Those are the bull-case facts.

The caution case is just as real. Public investors still do not have audited financials, gross margins, net losses, contract obligations, voting terms, lockup details, or a final share count. OpenAI may become one of the most important IPOs of the decade, but buying the first available exposure without understanding the structure would be speculation, not analysis.

The practical move is simple: follow the S-1, not the hype cycle. Investors who want indirect exposure can study ARK's OpenAI holdings, Microsoft as a partner and shareholder, and the surrounding AI infrastructure names. Investors waiting for the actual IPO should build a checklist now: revenue quality, compute cost trend, governance rights, partner concentration, insider selling, and valuation versus public AI leaders.

FAQ

Frequently asked questions

Is OpenAI publicly traded?

No. As of May 6, 2026, OpenAI has no public ticker and no public S-1 registration statement. The real IPO analysis starts when a filing appears on SEC EDGAR.

What is OpenAI valued at now?

OpenAI disclosed a $122 billion committed funding round at an $852 billion post-money valuation in its March 31, 2026 funding update.

When will OpenAI IPO?

OpenAI has not announced an IPO date. The April 2026 Microsoft amendment makes the structure cleaner, but no public filing, ticker, exchange or listing date has been confirmed.

What changed in the Microsoft-OpenAI deal?

Microsoft says OpenAI products can now be served across any cloud, the IP license runs through 2032 and is non-exclusive, and the revenue-share mechanics changed. OpenAI says Microsoft remains its primary cloud partner and a major shareholder.

Can retail investors buy OpenAI before the IPO?

Direct common-stock access is still limited. Some investors can get indirect exposure through private funds or bank allocations, but those vehicles are not the same as owning public OpenAI shares.

Is ARK Venture Fund a direct OpenAI stock substitute?

No. ARK Venture Fund can provide fund-level exposure to OpenAI if OpenAI is held in the portfolio, but investors own fund shares, not OpenAI common stock.

What are the biggest risks before the OpenAI IPO?

The main risks are unknown gross margin, compute obligations, partner concentration, nonprofit control, insider selling, and the valuation gap between private enthusiasm and public-market discipline.

Should investors buy OpenAI stock on IPO day?

There is no OpenAI stock to buy yet. When the IPO arrives, investors should read the S-1 first and compare valuation against revenue quality, margin trend, governance rights and lockup supply.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Hafsa Rizwan is a seasoned writer and proofreading editor at TECHi, where she leads a team of writers to deliver impactful technology coverage. She reports on the stories behind the tech headlines, providing deep analysis on all tech product-related news, industry giants, new product ecosystems, and app innovations. As an Architect and technology journalist, her expertise is uniquely focused on the critical shifts transforming how we connect, create, and build, a focus exemplified by her coverage of the fascinating intersection of architecture and technology.