- The tapeBitcoin was near $77.6K on May 20, 2026, while the Fear & Greed Index sat at 27, showing fear even without a classic crash.

- The real storyBitcoin fear is no longer contained inside crypto because ETFs, corporate treasuries and government reserve language have broadened the audience.

- The stress channelLiquidations turn belief into forced selling, making leverage the fastest way for crypto-native panic to spill into mainstream headlines.

- The institutional riskETF access made Bitcoin easier to own, but it also made Bitcoin easier to sell through ordinary brokerage and adviser systems.

- The TECHi angleBitcoin is becoming a trust volatility index: a live measure of confidence in institutions, money, policy and the digital-gold narrative.

On May 20, 2026, Bitcoin was not crashing. That is the strange part.

It was trading around $77,600 in fresh CoinGecko market data, up roughly 1% over 24 hours, with a market value near $1.55 trillion. By old crypto standards, that is not panic. It is a price level that would have sounded absurdly high in most of Bitcoin's history.

And yet the market felt frightened. The Crypto Fear & Greed Index sat at 27, in fear, one day after registering 25, or extreme fear. Bitcoin had just slipped below $77,000 after failing to hold the early-May return above $80,000. Bitcoin.com News reported that the drop triggered $657 million in crypto liquidations in 24 hours, including $584 million from long positions. In plain English: people who were betting on upside were not merely disappointed. They were forced out.

That is the story. Not that Bitcoin is dead. Not that Bitcoin is safe. The real story is that Bitcoin's fear is no longer contained inside crypto.

For more than a decade, Bitcoin fear belonged to a self-selected crowd: miners, exchanges, whales, developers, offshore leverage traders, libertarians, early adopters, Reddit believers and people who liked watching candles at 3 a.m. Now the fear moves through a much larger system. It moves through ETFs. It moves through brokerage accounts. It moves through corporate treasuries. It moves through government reserve language. It moves through retirees wondering why a supposedly small allocation feels louder than it looked in a model portfolio.

This is Bitcoin's universal phase. The asset is still volatile, but the ownership map has changed. The question is no longer only whether Bitcoin can go up. The question is what happens to a society when an asset designed to distrust institutions becomes packaged, distributed and defended by institutions.

TECHi's daily Bitcoin price page can track the tape. This essay is about the machine behind the tape.

The five numbers that explain the fear

The clean way to understand Bitcoin on May 20 is to ignore the culture war for one minute and look at the five numbers on the table.

Bitcoin was near $77,600, based on CoinGecko data updated late on May 20. It was still far below CoinGecko's listed all-time high of about $126,080 from October 2025. Sentiment was weak, with Alternative.me's Fear & Greed Index at 27. The recent liquidation shock was large enough to wipe out hundreds of millions of dollars in forced positions. And the ETF channel, which had helped Bitcoin reclaim $80,000 earlier in May, had started to cut both ways.

Cointelegraph reported that U.S. spot Bitcoin ETFs posted $635.2 million in outflows on May 13, the largest single-day withdrawal since late January at the time. Bitcoin Foundation later reported that spot Bitcoin ETFs saw $648.6 million in net outflows on May 18, citing SoSoValue data, as Bitcoin slipped back below $80,000.

That sequence matters. Earlier in May, the institutional story looked clean. IG noted that Bitcoin had pushed back above $80,000 as ETF inflows and institutional demand improved. HedgeCo framed the same move as evidence that ETF demand had become a central institutional bridge into the asset.

Then the bridge shook.

That is why the fear is powerful. The same wrapper that made Bitcoin feel more respectable also made the exit door more visible. A native Bitcoin holder can say, "I am not selling." An ETF holder can press one button in a brokerage account while rebalancing a retirement portfolio, responding to a model change, or trying to reduce risk before the next macro shock.

Bitcoin did not become less volatile when Wall Street arrived. It became easier for volatility to travel.

The ETF did not remove fear. It standardized fear.

The ETF was the great translation layer.

Before ETFs, Bitcoin demanded a ritual. A new buyer had to choose an exchange, understand custody, think about wallets, survive transfer anxiety and accept that mistakes could be final. That friction filtered the crowd. People who bought direct Bitcoin often had unusually strong conviction, unusually high risk tolerance, or both.

The ETF changed the emotional contract. It made Bitcoin look like any other allocation tile. It could sit beside the S&P 500, bonds, gold, commodities and cash. It could appear in an adviser conversation without forcing a long custody debate. It could be modeled at 1%, 2%, 5%, then passed through institutional language: alternative asset, digital gold, non-sovereign store of value, portfolio diversifier.

That language is softer than the asset.

Bitcoin remains Bitcoin. It trades all weekend. It reacts to liquidity, leverage, geopolitics, narratives, ETF flows and whale behavior. It can be a global macro asset in the morning, a tech beta trade by lunch and a liquidation engine overnight. The ETF did not tame that. It simply put the exposure into cleaner packaging.

That is not automatically bad. Cleaner access can reduce custody mistakes and make allocation more transparent. But society often confuses clean access with clean risk. Those are different things.

A knife in a drawer is still a knife. A Bitcoin ETF in a retirement account is still Bitcoin exposure.

The fear machine begins when the form looks conservative but the underlying asset remains emotionally violent.

Leverage turns belief into forced selling

Bitcoin has always attracted leverage because the story is so tempting. If someone believes Bitcoin is the future of money, a 5% move can feel insulting. Why own the asset when you can borrow against conviction and multiply the outcome?

The problem is that markets do not care how sincere a thesis is.

The May liquidation data is the brutal reminder. Bitcoin.com News reported $657 million in total crypto liquidations over a 24-hour window, with the bulk from long positions. That is not the same as ordinary selling. A liquidation is belief meeting a rulebook. The trader does not decide to exit calmly. The exchange decides for them.

This is why leverage creates social fear. It turns a price move into a cascade. One account gets closed. That forced sale pushes price lower. Lower price stresses the next account. The next liquidation becomes someone else's signal. Social media sees the red candle, fear spreads, and people who were not leveraged begin wondering what the leveraged crowd knows.

Nothing has to be fundamentally different for the mood to change. The structure can create the emotion.

This is the part ordinary investors often miss. Bitcoin's public narrative is philosophical, but its short-term price action is mechanical. It is about margin, collateral, ETF flows, liquidity, exchange order books and the exact places where crowded positions break.

In that sense, Bitcoin is not only an asset. It is a machine for discovering where conviction was borrowed.

Corporate treasuries make Bitcoin political inside companies

The second universal channel is the corporate treasury.

CoinGecko's Bitcoin treasury tracker showed 187 institutions holding about 1.87 million BTC, representing roughly 8.91% of Bitcoin's total supply. CorpStacking's Bitcoin treasury page showed a broader universe of public companies, governments and ETFs with meaningful balances, and listed Strategy, IBIT, governments and major funds among the largest holders.

Those numbers turn Bitcoin from a personal speculation into an organizational question.

When a person buys Bitcoin and loses money, the story is personal risk. When a public company buys Bitcoin, the story becomes governance. Who approved the treasury policy? Was debt used? Were shares issued? Are employees indirectly exposed? Are shareholders buying an operating business, a Bitcoin holding vehicle, or a hybrid they do not fully understand?

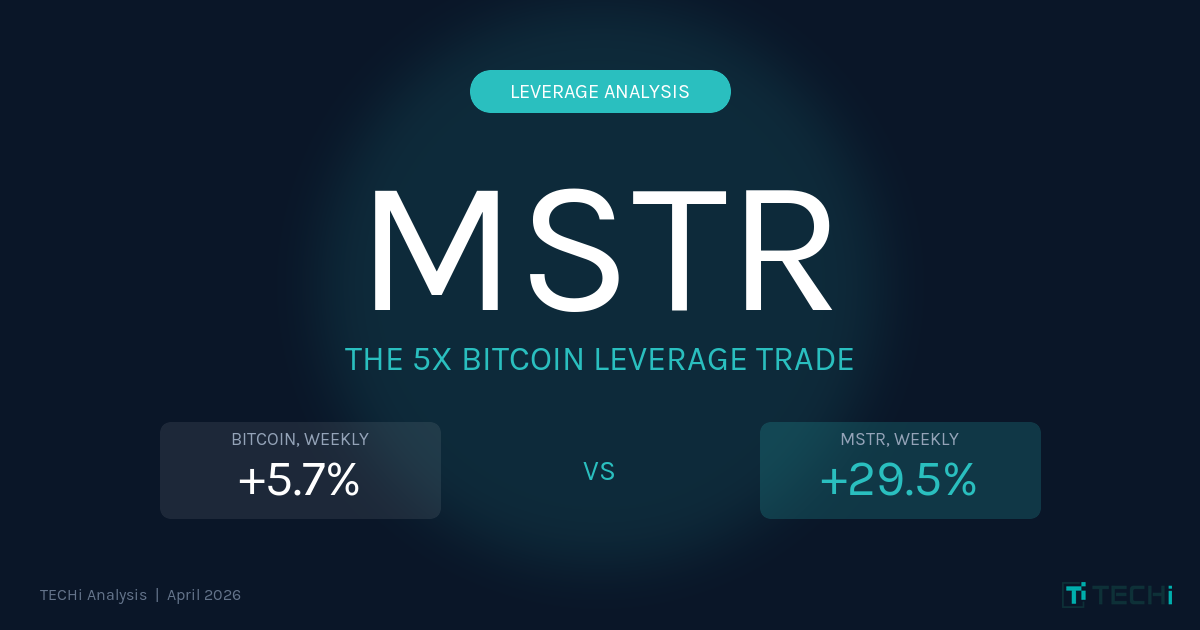

TECHi has already covered the two-sided nature of this mechanism in Bitcoin Moved 7%. MSTR Moved 30%. The equity wrapper can amplify the Bitcoin trade on the way up, but it can also make the drawdown feel larger than Bitcoin itself.

This is where fear becomes institutional. A CFO does not experience Bitcoin volatility like a trader. A CFO experiences it as balance-sheet scrutiny, audit questions, board pressure, financing cost, investor relations and headline risk. A worker may experience it indirectly as anxiety about whether management has turned the company into a proxy trade. A shareholder may experience it as confusion: did I buy business execution or monetary ideology?

The Bitcoin community often celebrates corporate adoption as validation. It is validation. But it is also social distribution of risk.

Every treasury that buys Bitcoin creates a new audience for Bitcoin fear.

Governments gave Bitcoin a new psychological status

The third channel is government language.

On March 6, 2025, the White House issued an executive order establishing a Strategic Bitcoin Reserve and United States Digital Asset Stockpile. The order described Bitcoin as capped at 21 million coins and often referred to as digital gold. A White House fact sheet said the reserve would treat Bitcoin as a reserve asset and would be capitalized with forfeited Bitcoin owned by the Treasury.

That did not make Bitcoin risk-free. It did something subtler. It changed the public imagination.

Once a government talks about Bitcoin as a reserve asset, the debate moves beyond traders. Citizens who never opened a wallet hear Bitcoin discussed beside national prosperity, global financial strategy and public stewardship. Supporters hear legitimacy. Critics hear political capture. Institutions hear policy momentum. Rival governments hear strategic competition.

That is how a volatile asset becomes a civic subject.

The old Bitcoin question was: should I buy it? The new Bitcoin question is: should our country, company, pension system, bank, endowment, adviser, school foundation, city treasury, or political movement be exposed to it?

That is a much heavier question. It carries identity, ideology and trust.

Why this could shake society

The phrase "shake society" sounds dramatic until you map the exposure honestly.

The first shock is retirement anxiety. ETFs make Bitcoin easier to include in ordinary portfolios. That means people who never wanted to join crypto culture can still end up exposed through products, advisers or model portfolios. A small allocation can be financially reasonable and emotionally loud at the same time. A retiree does not need a 20% Bitcoin allocation to feel stress. A 2% allocation can dominate attention if it is the only thing moving 24/7.

The second shock is resentment. Bitcoin creates visible winners and visible losers. When prices rise, believers can sound morally superior. When prices fall, skeptics can sound vindicated. That emotional rhythm is socially corrosive because it turns portfolio outcomes into identity contests. People do not merely disagree about valuation. They accuse each other of being blind, corrupt, naive or cowardly.

The third shock is institutional blame. If Bitcoin appears in company treasuries, ETF portfolios or government language, future drawdowns will not be treated as private speculation. They will produce accountability fights. Who normalized this? Who sold it as digital gold? Who collected fees? Who approved the exposure? Who failed to explain that a mainstream wrapper does not erase a volatile core?

The fourth shock is liquidity illusion. Bitcoin trades constantly, but not all holders are equally prepared to hold constantly. ETFs trade during market hours. Crypto trades all weekend. News moves at all hours. Liquidations can happen while traditional investors are asleep. That mismatch between always-on price discovery and human emotional capacity is one of Bitcoin's least appreciated social risks.

The fifth shock is political symbolism. Bitcoin is not just a technology or an asset. It is a referendum for many people on fiat money, state power, inflation, surveillance, banking access and the credibility of elites. When an asset carries that much meaning, every price move becomes easier to weaponize.

This is why Bitcoin's universal phase is dangerous even if Bitcoin succeeds.

A successful Bitcoin does not remove fear. A successful Bitcoin distributes fear into more institutions.

The digital gold problem

Gold has fear built into its brand. People buy it because they distrust something: currency, governments, banks, inflation, geopolitics or the future. Bitcoin borrowed that emotional territory and made it faster.

The White House order leaned directly into the digital gold analogy. Many investors use it too. The phrase is useful, but incomplete.

Gold does not have Bitcoin's weekend leverage culture. Gold does not have the same social-media-native reflexivity. Gold does not have a fixed supply schedule enforced by open-source software, public wallets, mining economics and global exchange infrastructure. Gold is heavy, old and slow. Bitcoin is scarce, liquid and online.

That speed is the difference.

Digital gold can move like a risk asset. It can be held as a reserve idea and traded as a momentum instrument. It can sit in a corporate treasury while also being used by leveraged traders as a battlefield. It can be praised by governments while being sold by ETF holders into macro stress.

Bitcoin's contradiction is not that it is fake. The contradiction is that it may be real enough to matter and unstable enough to scare everyone who touches it casually.

The new research angle: Bitcoin is a trust volatility index

The best way to read Bitcoin in 2026 is not only as money, technology, commodity, equity beta or digital gold. It is becoming a trust volatility index.

When people trust central banks, real yields, fiscal policy, banking stability and geopolitical order, Bitcoin can still rise, but it has to compete for attention. When trust weakens, Bitcoin becomes more emotionally charged. It becomes a vote, a hedge, a rebellion, a speculation and a social signal at once.

That makes the asset hard to value in traditional terms. A discounted cash flow model cannot capture distrust. A supply chart cannot capture humiliation. A four-year cycle chart cannot capture what happens when ETFs, governments and corporate treasuries all change the audience at the same time.

This is why Bitcoin can fall while becoming more important. Price is one signal. Relevance is another.

At $77,600, Bitcoin is still enormous. At a fear reading of 27, it is also emotionally fragile. Those two facts can coexist. In fact, that coexistence is the point.

The world has built a bigger Bitcoin door. Now more people can walk through it. The harder question is whether they know what kind of room they are entering.

What would make the fear worse

The fear machine accelerates if three things happen together.

First, ETF outflows need to continue. One day of selling can be absorbed. A streak changes behavior. If advisers and model portfolios start reducing exposure at the same time, Bitcoin's institutional bid can become an institutional ask.

Second, leverage needs to rebuild too quickly. After a liquidation event, traders often try to win back losses. That is exactly what makes the next liquidation event possible. If open interest rises while spot demand weakens, the market becomes more brittle.

Third, the corporate treasury story needs to crack. If companies that bought Bitcoin above current prices face financing pressure, shareholder lawsuits, dilution concerns or credit scrutiny, the narrative can shift from visionary treasury management to reckless balance-sheet engineering.

None of these outcomes is guaranteed. Bitcoin has survived worse. But the point of research is not to worship survival. It is to identify where the next stress travels.

What would calm the market

The calming path is also clear.

Bitcoin needs to hold its current range without depending on leverage. ETF flows need to stabilize, even if they do not immediately return to the strongest April levels. Fear needs to improve without becoming euphoria. Corporate treasury buyers need to show discipline rather than desperation. And the public conversation needs to become more honest about sizing.

A 1% Bitcoin allocation is not the same as a 20% allocation. Direct Bitcoin custody is not the same as an ETF. A treasury reserve policy is not the same as a leveraged equity proxy. A long-term belief is not the same as a margin position.

Most Bitcoin arguments fail because they flatten all exposure into one moral category. Either you believe or you do not. That is childish. The mature question is: who owns it, through what wrapper, with what time horizon, financed how, and with what pain tolerance?

That is the question society has to learn quickly.

The bottom line

Bitcoin's most important May 2026 signal is not the move from $80,000 to $77,000. It is the fact that a move like that now speaks to so many audiences at once.

The trader sees a setup. The ETF holder sees a red line in a brokerage app. The corporate CFO sees a treasury debate. The policymaker sees a reserve-asset argument. The retiree sees a headline. The skeptic sees proof. The believer sees a discount. The leveraged trader sees a chance to get even.

That is a fear machine.

Bitcoin may still become a larger reserve asset. It may still make new highs. It may still prove that fixed digital scarcity has a permanent place in global portfolios. But its social risk is rising with its legitimacy. The more mainstream Bitcoin becomes, the less its volatility belongs only to crypto.

This article is research and commentary, not investment advice. Bitcoin can move sharply in either direction, and ETF access does not remove crypto-market risk.

That is the extraordinary angle. Bitcoin does not have to collapse to shake society. It only has to become normal before society understands what normal Bitcoin fear feels like.

FAQ

Frequently asked questions

Why is Bitcoin fear spreading beyond crypto traders?

Bitcoin exposure now reaches ETFs, brokerage accounts, corporate treasuries and government reserve discussions, so volatility affects a wider group than native crypto traders.

What was Bitcoin trading at on May 20, 2026?

CoinGecko market data checked on May 20, 2026 showed Bitcoin near $77,600, with the Fear & Greed Index at 27.

Why do ETF flows matter for Bitcoin?

Spot Bitcoin ETFs give institutions and ordinary brokerage users easier access to Bitcoin, but the same channel can amplify selling when investors reduce risk.

What makes leverage dangerous in Bitcoin markets?

Leverage can force traders out automatically when price falls, creating liquidation cascades that accelerate moves and spread fear across the market.

Is this article saying Bitcoin will collapse?

No. The argument is that Bitcoin can become more legitimate and still become more socially disruptive because its volatility now reaches mainstream institutions.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Muhammad Zeshan Sarwar covers mobile technology, consumer electronics, and the intersection of crypto with mainstream products. He reviews phones and wearables against their shipping firmware rather than launch-day marketing, and tracks the crypto-in-app integrations Apple and Google actually allow on their platforms. His reporting spans hardware launches, iOS and Android ecosystem shifts, and the wallet and payments layer bridging both.