- The BuyStrategy (MSTR) disclosed the purchase of 34,164 BTC for $2.54 billion between April 13 and April 19, 2026, at an average price of $74,395 per bitcoin. Third-largest single purchase on record.

- BlackRock PassedStrategy now holds 815,061 BTC — larger than BlackRock iShares Bitcoin Trust (IBIT) which held 802,823 BTC. First time a single corporate treasury has surpassed IBIT in the spot ETF era.

- Financing MixFunded with $2.176 billion STRC preferred + $366 million MSTR Class A common. ~86% STRC — no dilution to MSTR common. STRC printed a record $1.156B daily volume on April 13.

- BTC Yield9.5% YTD 2026 — each MSTR share today controls 9.5% more Bitcoin than on January 1, 2026, net of issuance. Compounds to roughly 37% annualised.

- Saylor's Call"Bitcoin has won." Four-year halving cycle is dead; price is now driven by capital flows. Biggest risk: iatrogenic protocol changes, not macro or regulation.

Strategy (NASDAQ: MSTR) bought 34,164 BTC for $2.54 billion between April 13 and April 19, 2026, at an average price of $74,395 per bitcoin. The acquisition is the firm's third-largest single purchase on record and the largest weekly accumulation since November 2024. Total holdings now stand at 815,061 BTC, worth approximately $61.5 billion at today's spot price of $75,420. That stack is now larger than BlackRock's iShares Bitcoin Trust (IBIT), which held 802,823 BTC as of its latest disclosure. For the first time in the ETF era, a single corporate treasury owns more Bitcoin than the world's largest spot Bitcoin fund. That is the headline. The deeper story is how Strategy got there without diluting a single MSTR share.

The Buy, the Math, and Why It's Different

The mechanical numbers are clean. $2.54 billion deployed. 34,164 coins added. Average cost $74,395. Stack average now $75,527. Total cost basis across 815,061 BTC approximately $61.6 billion. At today's spot of $75,420, the entire position sits roughly at breakeven on a cost-basis view, but that reading undersells what the treasury is actually doing. The marked value is $61.5 billion. The realized accretion to shareholders is measured in a different metric entirely, and that is where the story gets interesting.

According to CoinDesk's desk coverage, this buy vaulted Strategy past BlackRock's IBIT on a BTC-held basis for the first time. Bitcoin Magazine and news.bitcoin.com both confirmed the structural overtake. The total cost figures match across sources.

How Strategy Just Passed BlackRock

The IBIT comparison is the one most market commentators will miss. BlackRock's spot Bitcoin ETF is the institutional on-ramp of record, the product that changed how pension funds, endowments, and registered investment advisors access Bitcoin. As of the latest disclosure, IBIT held 802,823 BTC on behalf of a large and distributed investor base spanning retail accounts, advisors, and institutional allocators. A single corporation, Strategy, now holds more Bitcoin than all of IBIT combined, on a balance sheet answerable to its MSTR common shareholders and a handful of preferred-stock vehicles.

Strategy crossing the 815,000 BTC line puts the firm past another symbolic threshold as well. It now owns approximately 3.88% of all Bitcoin that will ever exist, compared with 3.82% for IBIT. The gap will widen if Strategy continues buying at its current pace and IBIT's flows stay uneven, and it will narrow or invert if IBIT returns to the net-inflow runs that defined mid-2024. Either way, the question "who owns Bitcoin" is now answered differently than it was twelve months ago: a single corporate treasury and a handful of spot ETFs control a combined share of the supply that no small group of institutions has ever controlled before.

STRC and the Satoshi Accretion Mechanic

The financing side of the story is what drove most sell-side models to refresh overnight. The $2.54 billion raise broke down as $2,176.3 million from the sale of 21,795,389 STRC preferred shares, plus $366 million from 2,165,000 MSTR Class A common shares sold through the firm's at-the-market program. Roughly 86% of the raise was STRC, not common stock.

That composition matters because STRC is a perpetual preferred security that pays a monthly dividend and trades near a $100 par. It is not a dilutive claim on the common. Every dollar raised through STRC and deployed into Bitcoin increases the BTC-per-share backing for MSTR holders without expanding the common count. That is the mechanic Bitcoin Twitter calls Satoshi (or SAT) Accretion. Strategy is converting preferred-stock demand into permanent Bitcoin balance-sheet growth, and the STRC vehicle itself just printed a record $1.156 billion daily trading volume on April 13. The liquidity is there; the issuance cadence has room to run. For the architecture behind this, TECHi's STRC-machine breakdown walks through the full capital-structure plumbing.

BTC Yield 9.5% — What It Actually Measures

Strategy has published a proprietary performance metric for years: BTC Yield. It is not a dividend yield and not an interest rate. It measures the percentage change in BTC-per-share held by the common, net of new common issuance. A BTC Yield of 9.5% year-to-date, as disclosed alongside this acquisition, means that every MSTR share today controls 9.5% more Bitcoin than it did on January 1, even after all issuance in the period.

Annualised, 9.5% over roughly 15 weeks compounds to roughly 37%. That is a remarkable accretion rate for a company whose core business model is simply to hold an appreciating asset and fund additional purchases through preferred-security issuance. For context, most operating companies define shareholder value creation through share buybacks or EPS growth. Strategy is creating shareholder value through Bitcoin-per-share compounding, and the accounting scoreboard is BTC Yield rather than EPS. That reframing is part of why sell-side price targets for MSTR have historically underestimated the stock through each Bitcoin cycle.

Saylor's Four-Year-Cycle Obituary

On the call accompanying the disclosure, Michael Saylor pushed a framing that has been gathering momentum across institutional allocators for most of 2026: the traditional Bitcoin four-year cycle, anchored to the halving schedule, is no longer the dominant price mechanism. Price is now driven by capital flows. The halving is still a supply-side math fact, but the marginal buyer has shifted from retail speculation pre-2020 to corporate treasuries, ETF allocators, and sovereign-adjacent vehicles from 2024 onward. That changes the cyclical shape.

Saylor's sharpest line from the call: "Bitcoin has won." Not a trading call and not a price target; a structural observation that Bitcoin has passed the point where its role as digital capital needs to be defended at the institutional level. The implication for allocators is practical. If the four-year boom-bust cycle is dead, holding through the drawdowns becomes a lower-anxiety decision, and using preferred-stock financing to scale the position during drawdowns becomes the dominant capital-efficient strategy. That is exactly what Strategy did over the past week while BTC traded between $73,700 and $78,000.

Bitcoin as Digital Capital — and the Risk Most People Miss

The broader thesis coming out of this announcement is that Bitcoin is settling into a role as digital capital, which is different from both a payment system and a commodity. Digital capital compounds. It attracts financing structures built around it (STRC is one, IBIT-adjacent products will be more). Bank credit, custody infrastructure, and preferred-stock machinery are starting to wire around it the way they once wired around gold and equities. That is the capital-flows framing Saylor has been articulating for three years and that the tape is starting to vindicate.

The risk Saylor flags is the one most retail narratives ignore. In his framing, the biggest threat to Bitcoin's trajectory is iatrogenic protocol changes — the literal Greek-medical term for harm caused by well-intentioned treatment. Translated into Bitcoin: the risk is that a well-meaning developer proposal to "improve" the protocol accidentally weakens the monetary properties that make Bitcoin credible capital in the first place. This is not the usual retail fear (regulation, hackers, a flash crash) and not the usual macro fear (rate shocks, ETF flow reversal). It is a risk internal to Bitcoin's governance model. Long-term holders need to underwrite it.

What This Means for MSTR Stock

MSTR closed Friday at $166.52 and traded the Apr 20 pre-market roughly 2.5% lower despite the headline. That pattern is consistent with prior Strategy announcements: the stock often sells the news on the initial print, then re-rates higher once the market digests the financing mix and the BTC Yield contribution. The NAV premium (MSTR market cap versus implied Bitcoin NAV) is currently slightly positive after spending much of Q1 at a modest discount. A positive NAV premium allows Strategy to continue issuing STRC and Class A common at accretive levels, which feeds the BTC Yield flywheel described above.

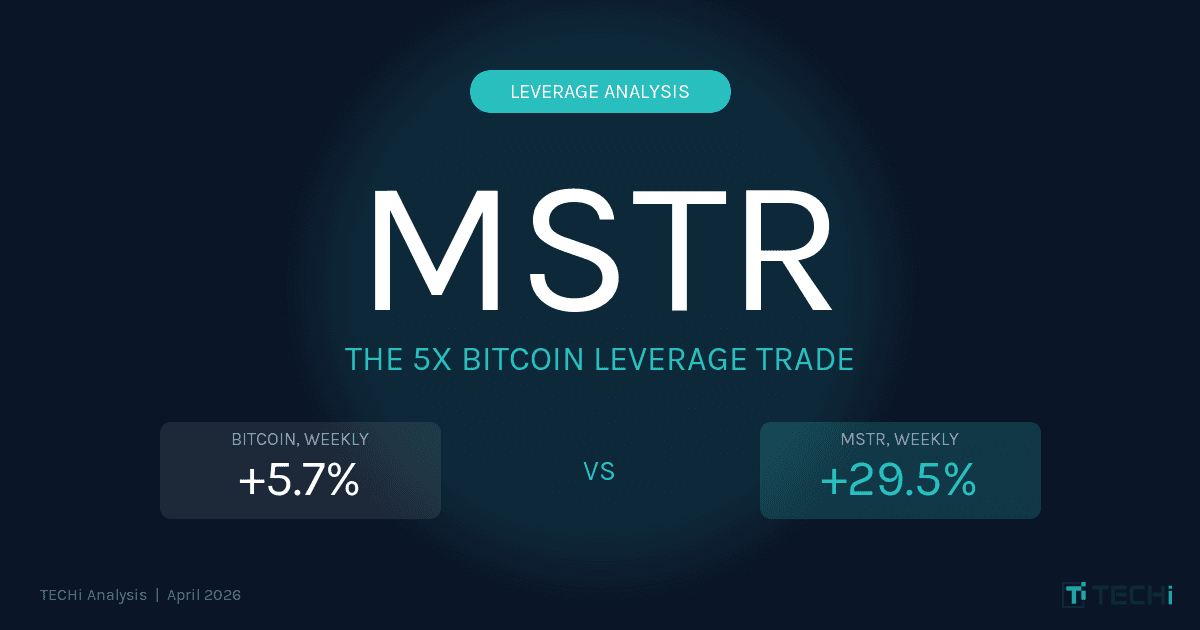

The trade to watch is the MSTR/BTC correlation tightness in the next two weeks. Historically, MSTR has amplified BTC moves by roughly 1.5x to 2.5x in both directions, with the STRC era potentially moderating downside beta. If BTC holds above $74,000 into April close and Strategy signals another large STRC raise, MSTR has the setup for a single-session 8% to 12% re-rate. If BTC breaks $72,000, the re-rate moves lower by a similar magnitude. For the mechanics of how the leverage actually works, TECHi's MSTR-Bitcoin leverage trade analysis is the cleanest walkthrough.

For the broader Bitcoin price context into Q2, see TECHi's live Bitcoin price page, and for long-horizon targets the 2026-2030 price prediction analysis. For the corporate-treasury leaderboard that Strategy now leads, the top Bitcoin holders database is updated monthly.

For macro context this week, see TECHi's Hormuz shutdown and tech stocks piece.

FAQ

Frequently asked questions

How much Bitcoin did Strategy buy on April 20, 2026?

Strategy (NASDAQ: MSTR) disclosed the purchase of 34,164 BTC for approximately $2.54 billion between April 13 and April 19, 2026, at an average price of $74,395 per bitcoin. This is the firm's third-largest single purchase on record and the largest weekly accumulation since November 2024. Total holdings now stand at 815,061 BTC.

Does Strategy now hold more Bitcoin than BlackRock?

Yes. Following the April 20, 2026 disclosure, Strategy holds 815,061 BTC against BlackRock's iShares Bitcoin Trust (IBIT) holding of 802,823 BTC. This is the first time in the spot ETF era that a single corporate treasury owns more Bitcoin than IBIT. Strategy now controls approximately 3.88% of all Bitcoin that will ever be mined.

How did Strategy fund the $2.54 billion Bitcoin purchase?

Approximately $2.18 billion came from the sale of 21,795,389 STRC preferred shares and about $366 million came from the sale of 2,165,000 MSTR Class A common shares through the firm's at-the-market program. Roughly 86% of the raise was STRC, which does not dilute the MSTR common share count. That structure is what produces the Satoshi Accretion effect on the common shareholders.

What is BTC Yield and why does it matter?

BTC Yield is Strategy's proprietary performance metric measuring the percentage change in Bitcoin-per-share held by MSTR common, net of new share issuance. A BTC Yield of 9.5% year-to-date 2026 means each MSTR share today controls 9.5% more Bitcoin than on January 1, 2026, after adjusting for any dilution. Annualised that pace compounds to roughly 37%.

What is Strategy's average cost basis per Bitcoin?

After the April 20, 2026 disclosure, Strategy's average cost across the full 815,061 BTC position is approximately $75,527 per Bitcoin, with a total cost basis near $61.6 billion. At a spot price of $75,420, the position sits roughly at breakeven on a cost basis, but the BTC-per-share accretion to common shareholders continues to compound via the STRC financing channel.

Why did MSTR stock fall after the announcement?

MSTR traded roughly 2.5% lower in the pre-market session on April 20 despite the large purchase. The pattern is consistent with prior Strategy announcements: the stock often sells the initial print, then re-rates higher once the market digests the financing mix and the BTC Yield contribution. The NAV premium is currently slightly positive, which supports continued accretive STRC issuance.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Omer Sheikh covers Elon Musk-led and Musk-adjacent companies for TECHi, with a focus on Tesla, xAI, SpaceX, X, Neuralink, The Boring Company, and the public-market read-throughs from their product cycles, capital needs, AI infrastructure plans, supply chains, and regulatory risk. He also follows MicroStrategy/Strategy and its Bitcoin treasury strategy, using his finance background to connect balance-sheet decisions, capital markets, valuation, catalysts, and downside risk. His work is built for readers who want the investment case behind the headline: what changed, what it means for cash flow or market value, and what would prove the thesis wrong.