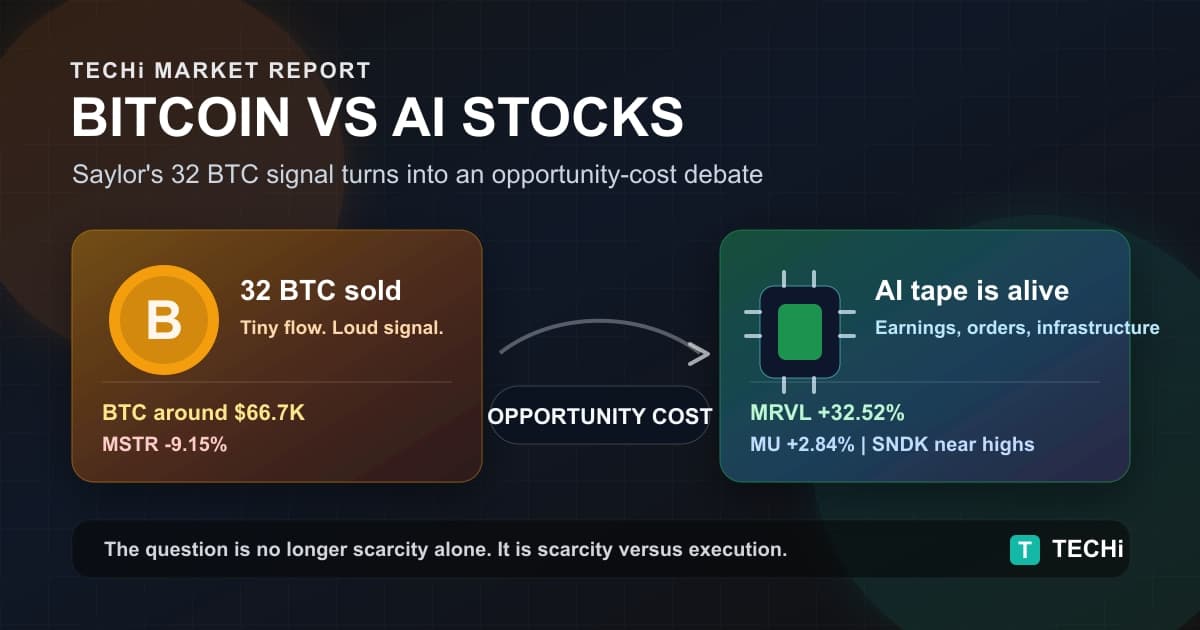

- Live TapeMRVL closed Monday April 20, 2026 at $147.84, up 5.8% on the Google AI chip talks. Year-to-date return of roughly 84% from the $80.46 YE-2025 close, and approximately 170% trailing twelve months.

- The Google DealGoogle is in talks with Marvell to co-develop two AI chips: a memory processing unit pairing with TPU accelerators, and a next-generation inference-optimised TPU. Makes Marvell Google's third custom silicon partner alongside Broadcom and MediaTek.

- Nvidia $2B HandshakeMarch 31, 2026: Nvidia announced a $2 billion strategic investment + NVLink Fusion technical partnership with Marvell, wiring custom XPUs and networking silicon into the Nvidia AI stack.

- 30-Day Analyst ParadeMarch 7 BofA Buy upgrade PT $110. April 1 BofA PT raised to $125. April 9 Barclays Overweight PT $150 + Citigroup Overweight. April 10 another upgrade triggered +7.1% session. Craig-Hallum PT $164.

- Market Share MapCounterpoint projects Broadcom 60% of custom AI accelerator market by 2027, Marvell ~25%. Marvell's data center revenue grew 46% YoY fiscal 2026, crossed $6B run-rate, with $9-$11B AI ASIC revenue projected for 2026.

Marvell Technology (NASDAQ: MRVL) closed Monday, April 20, 2026 at $147.84, up 5.8% from Friday's $139.69 close after Yahoo Finance reported that Google is in talks to co-develop two new AI chips with Marvell: a memory processing unit paired with Google's TPU accelerators and an inference-optimized next-generation TPU. That Monday pop caps one of the fastest re-rates in the semiconductor tape: MRVL is up roughly 84% year-to-date from its $80.46 close on December 31, 2025, and now trades meaningfully above the average sell-side price target of $131. The question for anyone buying today is whether this still has room, or whether the $147.84 print has fully absorbed the Google headline, the Nvidia $2 billion tie-up from March, and the seven analyst upgrades of the last thirty days. The answer depends on which side of Marvell's business model you are underwriting.

The Google Deal: What Marvell Actually Gains

The reporting is specific. Google is exploring two distinct chips with Marvell. The first is a memory processing unit, an on-package or near-package component that sits alongside Google's existing TPU accelerators and speeds up data movement during training and inference workloads. Memory-bandwidth bottlenecks are the single largest performance drag on modern AI training runs, which is why Nvidia's Grace Hopper architecture and Broadcom's custom accelerator lineup both prioritise the memory path. The second chip is a next-generation TPU specifically tuned for AI inference, the lower-latency, higher-volume workload that now accounts for the majority of hyperscaler GPU spend.

If both chips progress, Marvell joins Broadcom and MediaTek as the third named design partner inside Google's custom silicon supply chain. That is a structurally different story than "Marvell won a single SKU." Google has been the most vocal hyperscaler about reducing reliance on Nvidia GPUs and building out its in-house TPU program. Adding a second US-based custom partner (Broadcom has held that relationship largely solo) signals that Google now wants parallel suppliers for its most strategic accelerator roadmap. Marvell picks up the option value on that strategic split.

NVIDIA's $2 Billion Handshake

The Google talks are the second major validation event for Marvell in three weeks. On March 31, 2026, Nvidia announced a $2 billion strategic investment and technical partnership with Marvell, wiring Marvell's custom XPUs and networking silicon into the NVLink Fusion ecosystem. The deal covers custom XPUs, scale-up networking, silicon photonics collaboration, and access to Nvidia's Vera CPU, ConnectX NICs, Bluefield DPUs, and Spectrum-X switches. Marvell's own investor-relations release mirrors the announcement.

The Nvidia deal matters more for what it signals than for the dollar figure. $2 billion is a rounding error relative to Nvidia's cash position. What is not a rounding error is the strategic admission embedded in NVLink Fusion: Nvidia now wants its interconnect fabric to remain standard even when hyperscalers are buying custom chips from Marvell. In other words, Marvell's custom silicon wins become Nvidia wins on the network layer. For Marvell, the partnership gives its customers a compatibility path back to Nvidia's full stack, which lowers the switching cost of choosing a Marvell custom chip over an off-the-shelf Nvidia GPU. The competitive stance is subtle and very modern: Nvidia is converting a competitor into an ecosystem dependency.

The Competitive Map: Broadcom, Marvell, Nvidia, Intel

Four names, four different businesses, one shared tailwind. Nvidia (NASDAQ: NVDA, $201.68 close) still commands the pure AI GPU market. Its competitive moat is software (CUDA) and interconnect (NVLink), and NVLink Fusion is how it keeps that moat intact while hyperscalers experiment with custom silicon. Broadcom (NASDAQ: AVGO, $406.54) leads the custom AI accelerator category by a wide margin. Counterpoint Research projects Broadcom will hold roughly 60% of the custom AI accelerator market by 2027, with Marvell at approximately 25%. Broadcom's AI revenue surged 106% year-over-year to $8.4 billion in its most recent quarter. Marvell is the scrappier, higher-beta custom-silicon play. Intel (NASDAQ: INTC, $68.50) is in a separate competitive lane entirely, still working through foundry transition and manufacturing execution, and not currently a credible threat in the AI ASIC category despite the Gaudi accelerators on paper.

The framing that matters: Broadcom is the market leader, Marvell is the fastest-growing challenger, Nvidia is the platform the market is built on, and Intel is the execution wildcard. If the custom-silicon cycle plays out through 2027, Broadcom captures the dollars while Marvell captures the growth rate. Investors pick the name that fits their framework. TECHi's Apple vs Broadcom dividend and AI analysis walks through Broadcom's own AI thesis in detail, and the NVIDIA stock pillar covers the GPU-side of the same tape.

How Marvell Is Actually Taking Share

The public customer list is the most underrated data point in the Marvell story. As of Marvell's most recent disclosure, the company has 18 cloud-provider design wins for custom silicon. The named relationships include Amazon (Trainium processors), Microsoft (Maia AI accelerator), and Meta (a new data processing unit). Our coverage of Amazon stock and the AWS Trainium roadmap walks through why that one relationship alone is material to Marvell's forward revenue. Adding Google as a fourth named hyperscaler customer, if the talks progress, would give Marvell a clean sweep of the top four US hyperscale cloud providers.

The revenue math is improving fast. Marvell's data center segment revenue grew 46% year-over-year in fiscal 2026 and crossed the $6 billion run-rate threshold. The custom silicon business sits at a $1.5 billion annual run rate and is projected to scale to $9 billion to $11 billion of AI ASIC revenue in 2026 as the design-win pipeline begins converting to production shipments. For context, the custom ASIC market is projected to grow roughly 45% in 2026, well above the 16% growth analysts expect in GPU shipments for the same period. Marvell is riding the faster-growth sub-segment of the fastest-growth end-market in semis.

The 30-Day Analyst Parade

The last thirty days of analyst activity on MRVL tell a story of rapid sell-side catch-up. On March 7, Bank of America's Vivek Arya upgraded the stock from Neutral to Buy and raised his price target from $90 to $110, citing accelerating custom silicon momentum. On April 1, immediately following the Nvidia announcement, Bank of America reiterated its Buy and lifted the target to $125. On April 3, an analyst upgrade pushed MRVL to a fresh twelve-month high. On April 9, Barclays' Tom O'Malley upgraded the stock from Equal Weight to Overweight with the price target moving from $105 to $150. The same day, Citigroup upgraded MRVL to Overweight, flagging data-center and optical growth. On April 10, another analyst action triggered a 7.1% single-session move. Craig-Hallum has separately raised its target to $164, the highest published figure on the tape.

The consensus price target now sits at roughly $120 to $131 depending on source, which is the key framing for any buyer at $147.84. Roughly half the sell-side still has targets beneath spot. The Barclays $150, Citigroup Overweight, and Craig-Hallum $164 are the standouts that justify continued upside. Anyone buying MRVL today is effectively betting that the 30-day upgrade cycle continues into the Q1 earnings print expected in late May, at which point the consensus catches up to the tape.

Is MRVL Still a Buy at $147.84?

The question has three layers. On fundamentals, the answer is yes. Data center revenue compounding at 46% with a custom silicon pipeline that could reach $9 billion to $11 billion in 2026 is a structural growth rate that justifies a premium multiple. The Nvidia NVLink Fusion tie-up and the Google talks both add optionality without adding capital intensity. Twelve-month forward earnings power is still being re-rated higher quarter over quarter.

On valuation, the answer is more nuanced. MRVL at $147.84 trades roughly 13% above the consensus price target. That does not mean the stock is overvalued; it means the sell-side is lagging the tape, which is the expected pattern in a rapidly-revising earnings cycle. Premium customers tend to pay up for the re-rate rather than waiting for targets to catch up. The historical pattern in semis is that stocks that outrun consensus during an upgrade cycle continue to outrun it until the upgrade cycle exhausts, which typically takes two to three quarters. MRVL is roughly one quarter into this cycle. There is likely more runway.

On risk, the answer is be careful. The biggest downside is customer concentration. Marvell's custom silicon revenue is disproportionately AWS-weighted. Any AWS slowdown or TPU design-win shift would pressure the revenue stack faster than any single-customer risk at Broadcom, which has a more distributed customer book. The secondary risk is execution timing on the new chips. Google's memory processing unit is described as reaching final form as early as next year, which means 2027 revenue contribution, not 2026. Anyone buying MRVL on the Google headline needs to underwrite a patience window.

The AI Chip Demand Backdrop

Step back from MRVL specifically and the demand picture across AI semiconductors remains one of the strongest in modern market history. Counterpoint Research projects AI server compute ASIC shipments will triple by 2027, with the custom ASIC market projected to reach $118 billion by 2033. Hyperscaler capex for 2026 is now pegged at roughly $527 billion, up from $465 billion at the start of the Q3 2025 earnings season. TECHi's GE Vernova and Vertiv analysis walks through why the power and cooling side of that capex is compounding alongside the silicon side.

Inside the custom silicon bucket, Broadcom is winning the dollars and Marvell is winning the growth rate. Both can coexist for the rest of this decade. The pie is getting large enough that 25% of it is a $29 billion revenue opportunity for Marvell alone by 2033 on the Counterpoint trajectory, before assigning any valuation multiple. Long-duration buyers who already own the NVIDIA infrastructure thesis should view MRVL as a complementary second-layer position rather than a replacement trade.

The $10,000 Question

An investor with $10,000 and a three-year horizon has three defensible ways to express the AI semiconductor trade. Option A: own Nvidia directly at $201.68. Option B: own Broadcom at $406.54. Option C: own Marvell at $147.84. All three have compelling fundamentals, but they express different views. Nvidia is the platform bet. Broadcom is the market-leader custom-silicon bet with the cleaner customer diversification profile. Marvell is the higher-beta challenger bet that captures disproportionate growth-rate upside if the design-win pipeline converts cleanly.

A split position — roughly 40% Nvidia, 35% Broadcom, 25% Marvell — captures most of the AI infrastructure upside while diversifying against single-name earnings risk. A more aggressive take would tilt the Marvell weighting higher to 35%, accepting the concentration and execution risk in exchange for the steeper revenue-growth trajectory. Risk-averse buyers should anchor more heavily on Broadcom, where the customer diversification and market-share lead reduce the single-quarter execution risk that defines Marvell's near-term setup.

The honest answer on Marvell at $147.84: it is still a buy for investors who can hold through a two-to-three-quarter patience window and who understand that the Google deal is a 2027 revenue story, not a Q2 2026 revenue story. The rally has been fast, but the design-win pipeline has not meaningfully contributed to the reported numbers yet. Most of the upside still lives in the quarters ahead.

For broader context, see TECHi's Apple at $3.97 Trillion valuation breakdown and the live Bitcoin price page.

FAQ

Frequently asked questions

What is the Marvell-Google AI chip deal?

Google is in talks with Marvell Technology (NASDAQ: MRVL) to co-develop two AI chips: a memory processing unit that would pair with Google's TPU accelerators to speed up data movement during AI workloads, and a next-generation TPU optimised for AI inference. If the talks progress, Marvell would become Google's third named custom-silicon partner alongside Broadcom and MediaTek. Reports indicate the memory-chip design could reach final form as early as 2027.

Why did MRVL stock jump on April 20, 2026?

Marvell shares opened roughly 6% higher in pre-market trading on April 20 after reports that Google was exploring an AI chip co-development partnership with Marvell. The move added to an already-strong rally driven by Nvidia's $2 billion strategic investment on March 31 and a cluster of analyst upgrades including Barclays (Overweight, price target $150) and Citigroup (Overweight) on April 9.

How much is Marvell stock up year-to-date in 2026?

MRVL closed Monday April 20, 2026 at $147.84, up 5.8% from Friday on the Google AI chip talks. Year-to-date return of roughly 84% from the $80.46 year-end 2025 close, and up approximately 170% on a trailing twelve-month basis. Rally driven by the custom silicon business ramping with 18 named hyperscaler design wins, 46% year-over-year data center revenue growth, and back-to-back validation events from Nvidia and Google.

Is Marvell still a buy after the 84% rally?

Most sell-side analysts still rate MRVL a Buy or Strong Buy, with the consensus price target in the $120-$131 range and the most bullish targets at $150 (Barclays) and $164 (Craig-Hallum). The stock trades modestly above consensus, which is the expected pattern during a rapid upgrade cycle. Fundamentals remain strong with projected 2026 AI ASIC revenue of $9-11 billion. Key risks are customer concentration (AWS-heavy) and execution timing on new design wins. Consult a licensed financial advisor before making portfolio decisions.

How does Marvell compare to Broadcom and Nvidia?

Counterpoint Research projects Broadcom will hold roughly 60% of the custom AI accelerator market by 2027, with Marvell at about 25%. Broadcom's AI revenue surged 106% year-over-year to $8.4 billion in its most recent quarter. Nvidia still dominates the pure AI GPU market with its CUDA software moat and NVLink interconnect standard. Marvell is the fastest-growing challenger in the custom ASIC category, while Nvidia and Broadcom compete in adjacent but overlapping segments.

What is NVLink Fusion and why does it matter?

NVLink Fusion is Nvidia's interconnect standard for AI chips. The March 31, 2026 Nvidia-Marvell partnership gives Marvell's custom silicon customers a compatibility path to Nvidia's scale-up networking (Spectrum-X switches, ConnectX NICs, Bluefield DPUs). Strategically, NVLink Fusion allows Nvidia to remain essential to hyperscaler infrastructure even when customers buy custom chips from Marvell instead of Nvidia GPUs — converting a competitor into an ecosystem dependency.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Fatimah Misbah Hussain is a seasoned financial journalist at TECHi, specializing in stock market analysis, commodities, and tech sector finance. With a strong background in monitoring public markets and tech companies, she breaks down complex stock movements and commodity price trends into actionable insights.