- The DateTesla reports Q1 2026 results on Wednesday, April 22, 2026 at 5:30 PM ET (after the bell). Live Q&A webcast with Elon Musk and CFO Vaibhav Taneja.

- Live TapeTSLA closed Friday at $400.62, up ~15% on the week — the best-performing Magnificent Seven name over the five-day run.

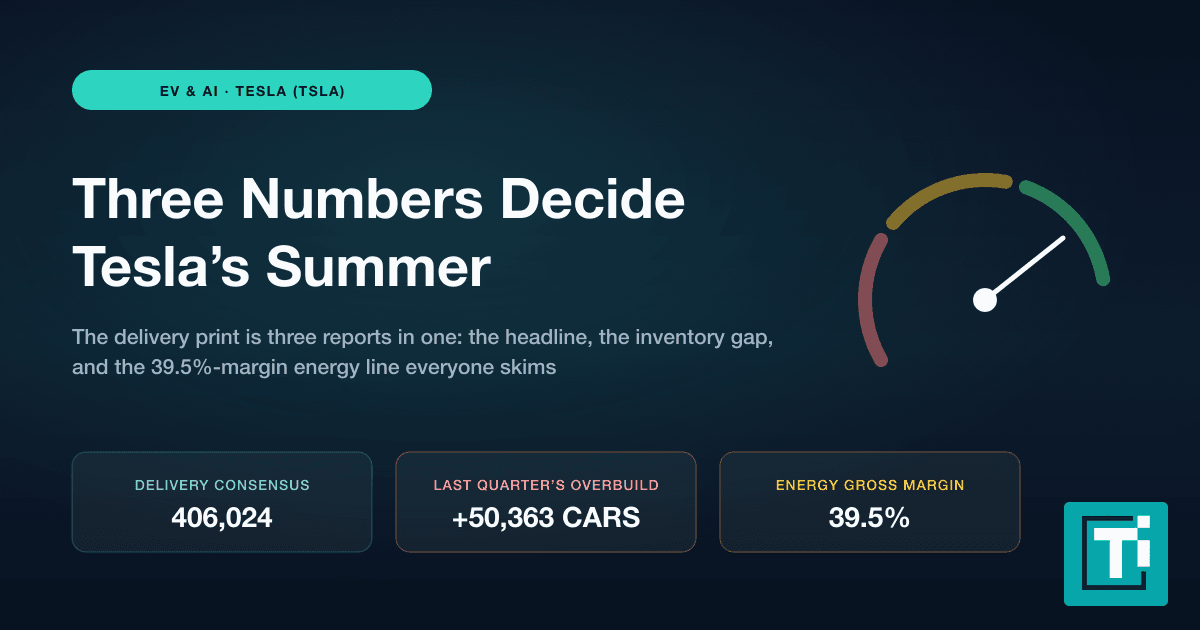

- ConsensusRevenue ~$23.06B (vs $19.34B YoY, +19%), adjusted EPS ~$0.40 (+48% YoY), GAAP EPS ~$0.16. Deliveries already confirmed at 358,023 — 2.1% below the 365,645 consensus.

- The Quiet NumbersProduction of 408,386 left a 50,363-vehicle inventory overhang (mostly Model 3/Y). Energy Storage deployments fell 38% sequentially to 8.8 GWh from 14.2 GWh in Q4 2025.

- The AI StoryRobotaxi is live unsupervised in Austin (31 Model Y, $4.20 fare) and as of mid-April in Dallas and Houston. Cybercab mass production begins this month. Wednesday reframes whether Tesla is a car company with an AI option or an AI-infrastructure company with a car option.

Tesla reports Q1 2026 results on Wednesday, April 22, 2026, at 5:30 PM ET — after the bell, with management hosting the usual live Q&A webcast. TSLA closed Friday at $400.62, up roughly 15% on the week, inside a five-day run that made Tesla the best-performing name in the Magnificent Seven. The setup matters because the last delivery print was a miss (358,023 vehicles against a 365,645 consensus), Energy Storage deployments fell 38% quarter-over-quarter, and the street still has Q1 revenue forecast at $23.06 billion with an adjusted EPS number that implies roughly 48% growth from the same quarter a year ago. Those three data points do not normally coexist. Wednesday night resolves which one is telling the truth.

What Wall Street Is Actually Expecting

The consensus going into the print: Q1 revenue of roughly $23.06 billion against the $19.34 billion Tesla reported in Q1 2025, adjusted EPS of about $0.40 versus $0.27 a year ago, and GAAP EPS closer to $0.16. Vehicle deliveries are already out at 358,023, published by Tesla at the start of the month. Production ran 408,386, which is the figure that creates the complication.

Tesla produced more than 50,000 vehicles it did not deliver in the quarter, almost all of it inside the Model 3 and Model Y book. That is inventory sitting somewhere, and inventory on a car company's balance sheet is never neutral. It is either a margin compressor (on the way to dealer-style price cuts) or a leading indicator (the fleet is being held back for an FSD- or software-driven release). Wednesday's call has to answer which one it is, and the answer is worth two to three points of gross margin either way.

The Delivery Miss Is Not The Headline Story

Most preview columns will lead with the 7,622-vehicle shortfall against consensus. That reads as cleaner than it is. Year-over-year deliveries still grew about 6%, which is the first positive-growth quarter after two negative-print quarters. The cleaner signal is the production-to-delivery gap: Electrek's detailed breakdown of the Q1 2026 delivery miss puts the excess at 50,363 vehicles, concentrated in Model 3/Y where production of 394,611 outpaced deliveries of 341,893.

A 50K-vehicle overhang walking into Q2 is not a small number. At a blended average selling price near $40,000, that is $2 billion of revenue shifted right on the balance sheet, and somewhere between $400 million and $600 million of gross profit depending on the mix and the pricing action taken in the following quarter. If Tesla discounts the excess to clear it, Q2 gross margin compresses before Cybercab and robotaxi revenue meaningfully contribute. If Tesla holds the line on price, deliveries rise but cash conversion lags. Either path has implications for the valuation framework.

The Margin Line Everyone Should Watch

Revenue growth of 19% year-over-year against EPS growth of 48% on adjusted and a materially lower number on GAAP is a wide spread. That spread is the single most important thing on the Wednesday tape, and here is why: either regulatory-credit revenue is doing the work (which is high-margin but effectively one-time in nature and lumpy), or FSD revenue recognition has finally clicked in with the software-style margin profile the bull case has been pricing for two years, or both. The call commentary has to unpack the two, and the stock moves differently depending on which one is larger.

Bull case split: FSD carries the revenue line, regulatory credits shrink as a share, and Tesla shows operating leverage you can underwrite into 2027. Bear case split: regulatory credits doing most of the heavy lifting, FSD revenue still bumping along, and the margin narrative gets fragile the moment credit pricing normalises. This is the same pattern that decided last year's Q2 print, and the stock moved 12% overnight on the result. Expect similar volatility around Wednesday's 5:30 PM ET release.

Robotaxi — The Part That Isn't Priced In Yet

Tesla's robotaxi service is now operating unsupervised in Austin at a flat $4.20 fare with a 31-vehicle Model Y fleet, and this month the geofence expanded into Dallas and Houston. Videos posted mid-April confirm rides with nobody in the front seats in both new cities. That is the first multi-market commercial robotaxi deployment with no safety monitor aboard by any major US operator, and it is running on Tesla's own Full Self-Driving stack rather than a Waymo-style custom hardware architecture.

Wall Street's models have this revenue line at roughly zero in 2026 and rounding error in 2027. That framing is wrong if the Dallas and Houston expansion holds, because it means Tesla has validated a software-only unit economics profile that can be cloned across geography without capital deployment. The directly comparable work is what TECHi's NVIDIA vs Tesla framework walks through — essentially, whether Tesla is a car company with an AI option or an AI-infrastructure company with a car option. Wednesday's call is the first earnings opportunity to move the needle on that debate with real data.

The Cybercab Quarter

Separately, Cybercab. The first production unit rolled off the line in mid-February 2026, several weeks ahead of the originally targeted April timeline, with Elon Musk confirming low-volume builds on the dedicated manufacturing line. Mass production is targeted for this month, which means Q2 2026 is the first quarter with meaningful Cybercab revenue — but Wednesday's call will provide unit-level colour on that ramp, plus any indication of pricing, fleet-operator versus consumer split, and geographic rollout.

Cybercab matters because it is the first vehicle Tesla has designed from scratch for autonomous use, with no steering wheel, no pedals, and a per-mile cost structure that analysts estimate at 30 to 40% below Model Y robotaxi economics. If management signals that 2026 production targets are intact or rising, the robotaxi revenue re-rating has a physical product pathway. If management defers the volume timeline, the AI-bet narrative takes a real bruise.

Energy Storage: The Quiet 38% Miss

Q1 Energy Storage deployments came in at 8.8 GWh against 14.2 GWh in Q4 2025, a 38% quarter-over-quarter decline. This is the number most preview columns skip, and it should not be skipped. Tesla's storage business had been the cleanest secular-growth thesis in the company's mix through 2024 and 2025, compounding at rates that made it the second-biggest contributor to gross profit behind auto. A 38% sequential drop signals either a large Megapack order timing gap or a genuine demand deceleration, and the two look very different through the lens of TECHi's $10 trillion energy rewrite analysis.

This is the quarter where Energy Storage either gets reframed as volatile-but-growing or starts to look like the cyclical it was never supposed to be. Wednesday's call commentary on backlog and contract signings is the tell. A Megapack backlog announcement that matches or exceeds $15 billion, pushed into 2026-2027 deployments, restores the secular-growth narrative. Anything below that shifts the framing, and analysts will have to rebuild the storage revenue stack almost immediately.

What Could Make This Print Rip — Or Fail

Three specific disclosures would send TSLA sharply higher from Wednesday's close: (a) a Cybercab 2026 unit target that materially exceeds current sell-side (above 20,000 units annualised on run-rate), (b) robotaxi miles-driven and revenue-per-mile figures that validate the unit economics for the first time on record, and (c) a gross margin ex-credits above 19%, which would put to rest the "credits are carrying it" debate.

Three disclosures would send it sharply lower: (a) price cuts confirmed on the Model 3/Y range to clear the production-delivery gap, (b) Cybercab timeline deferral, and (c) Energy Storage commentary that acknowledges demand-side weakness rather than timing-driven seasonality.

Macro overlay matters too. The tape Wednesday afternoon sits inside an oil spike and Iran-Hormuz headline cycle that has already hit the broader market — TECHi's walk-through of the Hormuz shutdown and its tech-stock playbook covers the three transmission channels oil prices use to reprice equities. Tesla's rate sensitivity is higher than NVIDIA's because its multiple implies more duration in its cash flows, so a hot oil-inflation setup can compound any fundamental miss.

Earnings Week Context

Tesla prints into a dense earnings slate. GE Vernova and Vertiv also report Wednesday, both before the open and both delivering the first read on hyperscaler AI capex commitments this quarter. Alphabet follows later in the week. Intel prints Tuesday. Baker Hughes, Honeywell, American Express, and Comcast fill out the Tuesday slate. That means Wednesday's afternoon tape — which Tesla enters at 5:30 PM ET — already has a full day of AI-infrastructure and industrial-capex signal priced in. If GEV and VRT print strong on Wednesday morning and Tesla prints soft on Wednesday night, the pair trade reads as "own the picks-and-shovels, rent the narrative." If the reverse happens, the AI-infrastructure bid decompresses and Tesla carries the AI leg of the Magnificent Seven into the rest of the quarter.

The $10,000 Question

The $10,000-over-three-years question for TSLA at $400 is unusual, because Tesla is the rare mega-cap whose 2029 fair value sits in a wider range than most analysts will publicly admit. A conservative sum-of-parts on the auto business alone supports a $240 to $280 stock. A base-case model that gives 2% of per-mile US ride-hail market share to Tesla robotaxi supports $450 to $520. An upside case with Cybercab fleet economics clicking and FSD licensing at scale gets to $700-plus. The difference between those three cases is almost entirely decided by what management discloses on Wednesday and over the next four earnings calls.

The honest framing is that TSLA at $400 is priced for a middle case with more optionality than any other name in the Magnificent Seven. A reader who cannot stomach the volatility should own the stock small and pair it with an AI-infrastructure position (such as the GEV and VRT pair trade covered earlier this week) to hedge the downside. A reader who can stomach the volatility and believes management's robotaxi disclosures Wednesday night should treat any 5%+ single-day drop as a buying opportunity, consistent with how TSLA has historically absorbed earnings-driven drawdowns over the 2023-2025 cycle.

The binary is Wednesday night. Three catalysts, two tail outcomes, one conference call. The rest of the Magnificent Seven will reprice around whichever way it breaks.

For broader context, see TECHi's Apple $4 trillion valuation breakdown and the NVIDIA stock analysis pillar.

FAQ

Frequently asked questions

When does Tesla report Q1 2026 earnings?

Tesla reports Q1 2026 results on Wednesday, April 22, 2026, at 5:30 PM ET (after the US market close). The live question-and-answer webcast is hosted by Elon Musk and CFO Vaibhav Taneja and runs about 60 to 90 minutes.

What are analysts expecting for Tesla Q1 2026?

Consensus: revenue of approximately $23.06 billion (up from $19.34 billion in Q1 2025), adjusted EPS of roughly $0.40 (up 48% year-over-year from $0.27), and GAAP EPS near $0.16. Deliveries are already confirmed at 358,023 vehicles, slightly below the pre-print consensus of 365,645.

Did Tesla miss Q1 2026 deliveries?

Tesla delivered 358,023 vehicles against an analyst consensus of 365,645, a 7,622-unit miss or roughly 2.1%. Year-over-year deliveries still grew about 6%, the first positive quarter after two negative-growth quarters. Production ran at 408,386, meaning Tesla built roughly 50,363 more vehicles than it delivered, almost all in the Model 3/Y category.

What is the Cybercab timeline?

First production Cybercab rolled off the line in mid-February 2026, several weeks ahead of the originally targeted April start. Low-volume builds are underway on a dedicated manufacturing line. Mass production is targeted for April 2026, which means Q2 is the first quarter with meaningful Cybercab revenue. Wednesday's call should provide unit-level guidance on the ramp.

Is Tesla's robotaxi service operating unsupervised?

Yes, in Austin. Tesla runs a 31-vehicle Model Y fleet at a flat $4.20 fare with no safety monitor in the vehicle. Mid-April 2026, Tesla expanded unsupervised service into Dallas and Houston, with videos confirming no occupant in any front seat. This is the first multi-market commercial robotaxi deployment without safety monitors by any US operator.

What happened to Tesla Energy Storage deployments?

Q1 2026 Energy Storage deployed 8.8 GWh, a 38% sequential drop from Q4 2025's 14.2 GWh. The number is the quiet miss in the Q1 print and is the single line item that will determine how analysts frame the energy business going forward. Call commentary on Megapack backlog and contract signings is the tell.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Omer Sheikh covers Elon Musk-led and Musk-adjacent companies for TECHi, with a focus on Tesla, xAI, SpaceX, X, Neuralink, The Boring Company, and the public-market read-throughs from their product cycles, capital needs, AI infrastructure plans, supply chains, and regulatory risk. He also follows MicroStrategy/Strategy and its Bitcoin treasury strategy, using his finance background to connect balance-sheet decisions, capital markets, valuation, catalysts, and downside risk. His work is built for readers who want the investment case behind the headline: what changed, what it means for cash flow or market value, and what would prove the thesis wrong.