Friday's tape delivered the useful kind of warning: AI demand can be excellent and the stocks can still be punished.

Broadcom did not hand investors a weak quarter. In its SEC-filed Q2 fiscal 2026 release, the company reported $22.2 billion of revenue, up 48% from a year earlier, and $10.8 billion of AI semiconductor revenue, up 143%. Management also guided for about $29.4 billion of Q3 revenue and said AI semiconductor revenue should reach $16.0 billion in the quarter.

That is not a demand problem. It is a hurdle problem.

As of Friday evening, June 5, 2026, Eastern Time, the market was no longer rewarding every AI infrastructure stock simply for showing up with a bigger number. The next phase is more discriminating: who converts hyperscaler capex into durable free cash flow, who owns a bottleneck, who has enough power or grid access, and whose valuation already assumes a clean buildout. The live TECHi stocks command center is useful here because it separates the AI equity universe by economic role instead of throwing every ticker into one broad theme.

Broadcom raised the numbers, but investors raised the exam

The important part of Broadcom's report is not just the $10.8 billion AI semiconductor line. It is the composition behind it: custom AI accelerators and AI networking. Those are the areas investors have treated as the cleanest alternatives to Nvidia's GPU stack, and they sit at the center of TECHi's Broadcom quote page.

That makes the market reaction more revealing. Broadcom's Q3 AI semiconductor guide of $16.0 billion implies another step-up, yet the stock still absorbed pressure because the question shifted from "is AI demand real?" to "how much evidence is enough for this multiple?"

That shift matters beyond AVGO. It says investors are moving from a story market to an operating market. The companies that win from here will need more than exposure. They will need supply visibility, margin discipline, customer concentration that can be defended, and proof that AI orders are not pulling demand forward from future quarters. It also extends the setup from our recent Broadcom earnings preview into the more important post-print question: what does the tape now demand from every AI infrastructure name?

Nvidia proves the buildout is real, not easy

The cleanest counterargument to any AI-bubble shorthand is Nvidia's latest print. Nvidia reported Q1 fiscal 2027 revenue of $81.6 billion, up 85% from a year earlier, and Data Center revenue of $75.2 billion, up 92%. The same release put Data Center networking revenue at $14.8 billion, up 199%, and guided Q2 revenue to roughly $91.0 billion. TECHi's NVDA quote page keeps the live market layer separate from that company-reported operating data.

Those numbers argue against the easy version of the bear case. The problem is not that AI infrastructure spending disappeared. The problem is that expectations got precise.

A year ago, a stock could rally because it touched AI compute. Now the market is sorting the stack. GPUs, custom ASICs, networking, memory, power equipment, cooling, contract manufacturing, cloud distribution, and data-center real estate all have different margins and different chokepoints. They should not trade as if they are the same business.

TECHi's stocks hub points to the rotation

This is where TECHi's /markets/stocks/ command center is useful. The page is not organized as a generic ticker list. It splits the AI equity universe into core platforms, infrastructure, applications, power and data centers, adjacent compounders, and ETFs.

At the June 5 after-hours snapshot, the hub tracked 129 tickers. Infrastructure was the largest bucket with 61 names, while power and data centers added another 17. The current Horizon Buys list was not a pure chip chase: Alphabet, Celestica, Amphenol, TE Connectivity, and Microsoft were the top five signals, with Vertiv also high on the live table.

That mix says something. The market still wants AI, but it is looking harder at where the bottleneck sits. Alphabet and Microsoft bring distribution, cloud demand, and balance-sheet capacity, which readers can track through the GOOGL quote page and MSFT quote page. Celestica brings the AI server supply chain. Amphenol and TE Connectivity sit closer to connectors and electrification. Vertiv, covered on TECHi's VRT quote page, is tied to power and cooling, where AI factories become physical assets instead of slide-deck TAM.

Broadcom remains essential in custom silicon and networking. But the June 5 setup says the better question is no longer "which single stock is the Nvidia alternative?" It is "which part of the buildout has pricing power without carrying the whole expectation burden?"

Power has moved from footnote to financial line item

The market is also getting more serious about electricity. The International Energy Agency's Energy and AI report estimates that data-center electricity consumption was around 415 TWh in 2024 and is set to more than double to about 945 TWh by 2030. The IEA also says U.S. data centers account for nearly half of electricity-demand growth between now and 2030.

The U.S. Department of Energy's LBNL-backed report puts the domestic issue in sharper terms: data centers consumed about 4.4% of U.S. electricity in 2023 and could consume 6.7% to 12% by 2028. This follows the same physical-capacity thread TECHi covered in Why AI Expansion Is Driving Energy Infrastructure Investment.

That is why the AI trade now includes companies investors used to treat as boring. Cooling gear, electrical systems, switchgear, transformers, grid services, colocated power, and rate structures are no longer side quests. They decide when capacity comes online and what it costs.

For hyperscalers, this is a capex and deployment question. For infrastructure suppliers, it is backlog and margin. For utilities and power-equipment companies, it is a political and regulatory question. For investors, it is the difference between a clean growth story and a trade that can get delayed by permits, interconnection queues, local opposition, and fuel costs.

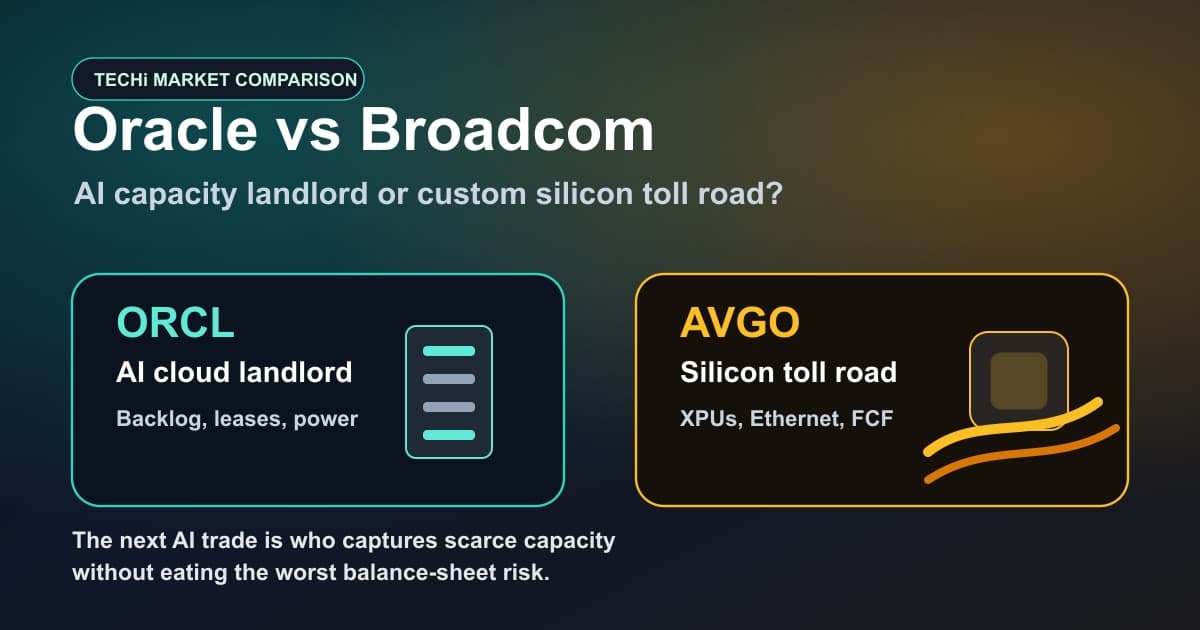

Oracle shows how large the commitments have become

Oracle is another reminder that AI infrastructure is becoming balance-sheet infrastructure. In its Q3 fiscal 2026 release, Oracle said remaining performance obligations reached $553 billion, up 325% year over year, with most of the increase related to large-scale AI contracts. Cloud Infrastructure revenue rose 84% to $4.9 billion.

That kind of backlog changes the conversation. AI is no longer only a chip-cycle story. It is an infrastructure-financing story: who prepays, who buys GPUs, who owns capacity risk, who funds power, and who earns enough margin to justify the capital intensity. That was also the central issue in TECHi's Oracle vs Broadcom comparison.

The companies that look safest in a spreadsheet may still disappoint if the buildout slows. The companies that look expensive may keep compounding if their bottleneck becomes harder to replace. That is why the stock-level work matters now.

What matters now

Investors should read the June 5 reset as a standards change, not a funeral for the AI trade.

AI revenue quality matters more than AI revenue size. A dollar of high-margin software, a dollar of custom silicon, a dollar of connector revenue, and a dollar of utility load are not equal.

Networking is no longer a supporting actor. Nvidia's 199% Data Center networking growth and Broadcom's custom AI networking exposure both point to the same issue: clusters get bigger, and the fabric between accelerators becomes a bottleneck.

Power access is part of valuation. Data centers that cannot get electricity are not capacity. Suppliers that help solve power, cooling, or grid complexity deserve a different lens from companies that merely benefit from AI sentiment.

Cash conversion is the filter. Broadcom's free cash flow was 46% of Q2 revenue. That is why the stock can remain a serious compounder even when the tape gets harsher. But the market will increasingly ask every AI infrastructure company to prove that orders become cash, not just backlog.

The right watchlist is wider than chips. Nvidia and Broadcom are still central. But the live TECHi signal is pushing readers toward the broader physical layer: Alphabet and Microsoft for platform scale, Celestica for buildout execution, Amphenol and TE Connectivity for interconnects, Vertiv for power and cooling, and the energy names that can support load growth.

The AI trade did not stop mattering. It became less forgiving. That is healthier than it feels in the moment, because a stricter market eventually separates durable infrastructure companies from ticker symbols wearing an AI label.

FAQ

Frequently asked questions

Why did Broadcom stock fall even though AI revenue was strong?

Broadcom reported $10.8 billion of Q2 fiscal 2026 AI semiconductor revenue, up 143% year over year, but the market reaction showed that investor expectations had already moved higher. The issue was not weak demand; it was whether the next guidance step was enough for the valuation.

Which AI infrastructure stocks stood out on TECHi's stocks hub?

As of TECHi's June 5, 2026 after-hours snapshot, the Horizon Buys list was led by Alphabet, Celestica, Amphenol, TE Connectivity, and Microsoft, with Vertiv also high on the live table.

Is Nvidia still the center of the AI infrastructure trade?

Nvidia remains central. Its Q1 fiscal 2027 release showed $81.6 billion of revenue and $75.2 billion of Data Center revenue, but the broader trade now includes custom silicon, networking, server manufacturing, connectors, power, cooling, and cloud capacity.

Why does electricity matter for AI stocks?

Electricity determines when AI capacity can come online and what it costs. The IEA estimates data-center electricity consumption will more than double to about 945 TWh by 2030, while the DOE says U.S. data centers could consume 6.7% to 12% of domestic electricity by 2028.

Is this article investment advice?

No. TECHi market coverage is educational and informational. It is not a recommendation to buy, sell, or hold any security.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Muhammad Zeshan Sarwar covers mobile technology, consumer electronics, and the intersection of crypto with mainstream products. He reviews phones and wearables against their shipping firmware rather than launch-day marketing, and tracks the crypto-in-app integrations Apple and Google actually allow on their platforms. His reporting spans hardware launches, iOS and Android ecosystem shifts, and the wallet and payments layer bridging both.