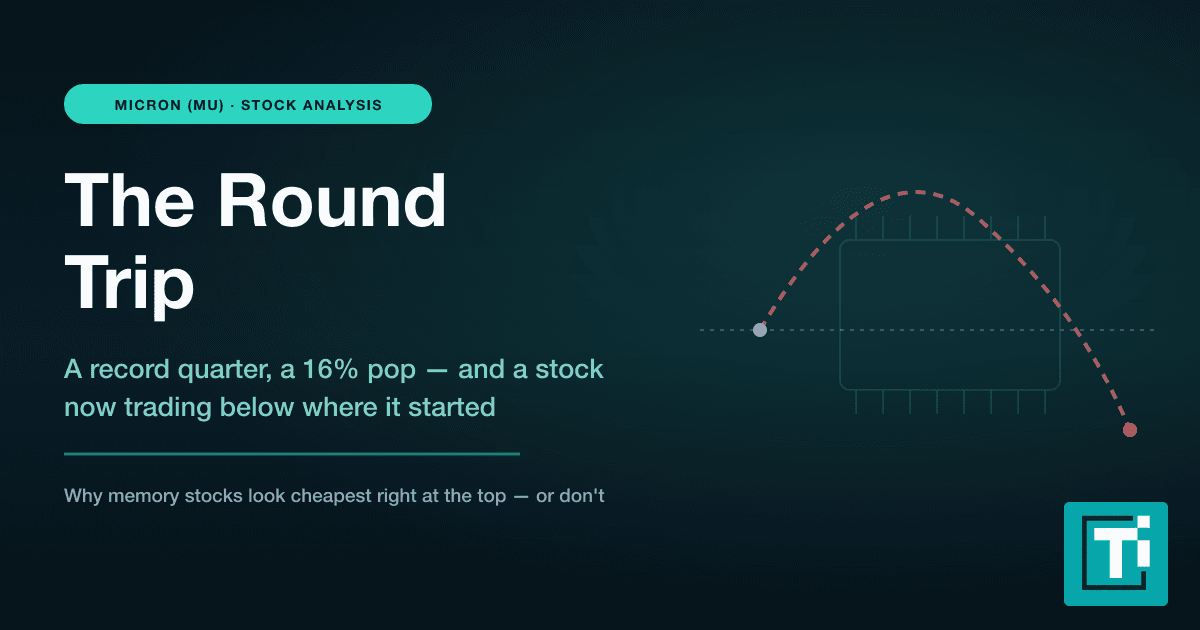

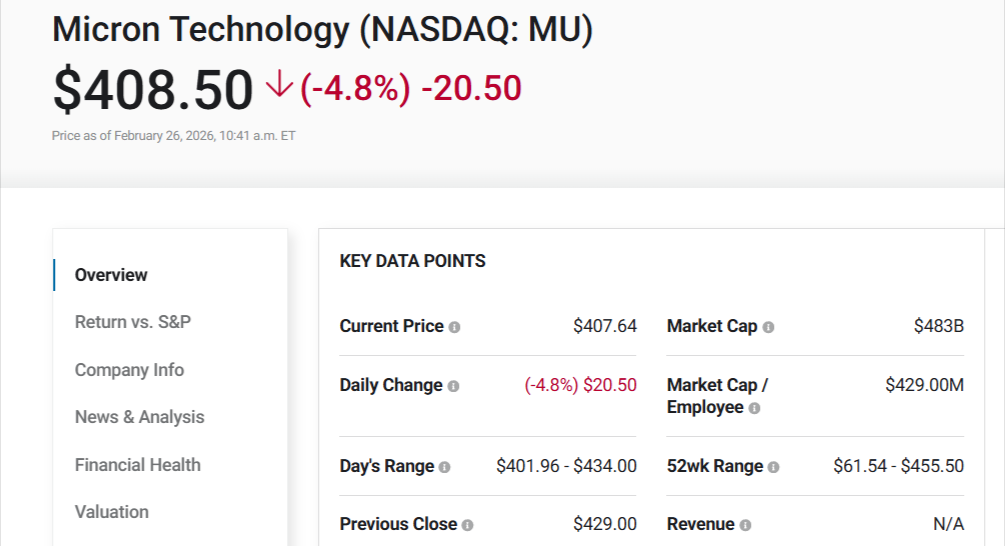

The share of Micron Technology has risen more than 300% over the last fiscal year; it is currently at about $408.50, having dropped to less than $100, thus increasing the capitalization of the company.

This sharp surge can be largely credited to the relentless AI-driven demand to its high-bandwidth memory (HBM) products, which has exceeded supply, and caused the company to achieve historically high profit margins.

Boom Fueled by AI Hunger

Micron, the largest vendor of DRAM and NAND flash memory chips, recorded a fiscal Q1 2026 revenue of $13.64 bn, which was up by 57% compared to the year-on-year increase of 5.7, and greatly exceeded the forecasts.

In fiscal Q2 2026, the management projected the issuance of sales of $18.7 bn, which is a growth rate of 130 % and exceeds the total revenue of an entire fiscal year 2023. Besides, the earnings per share are expected to be $8.42 with gross margins projected to be 68.

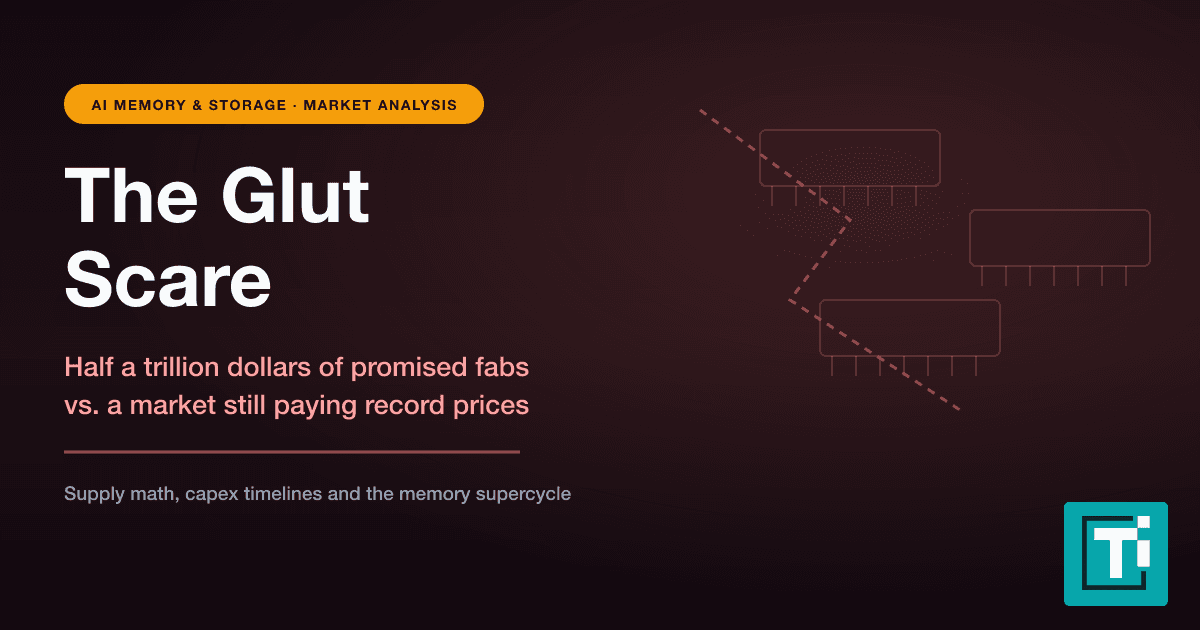

According to Micron, it can meet roughly 60% of its 2026 demand, indicating that supply will also have trouble meeting demand in 2027. According to the more negative projections, the high demand for data centers will cause supply shortages to persist until 2028.

Micron's revenue is expected to increase by about 100% in 2026 over the previous year. The business will probably perform better than anticipated.

Sanjay Mehrotra, CEO, President & Chairman, reported

"an outstanding start to fiscal 2026, delivering fiscal Q1 revenue, gross margin and EPS well above the high end of our guidance." Mehrotra stated that Micron has "completed agreements on price and volume for our entire calendar 2026 HBM supply including Micron's industry-leading HBM4," and forecasted an HBM total addressable market (TAM) CAGR of approximately 40% through calendar 2028 from $35 billion in 2025 to around $100 billion in 2028.

Prognosis: High Stakes, High Reward.

The demand on the Micron solutions based on memory is still dependent on the projected spending on AI hyperscalers in 2026, but the success of the company depends on the long-term investment in infrastructure.

In case these macro-economic forces remain in place, Micron may outpace the S&P 500 mark within a period of five years but, on the contrary, a downturn in demand could be a big drawback.

Micron is an interesting investment target to risk-taking investors who are willing to take the long-term prospect of AI applications.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Warisha Rashid writes about the intersection of corporate strategy, venture capital, and macro for TECHi — why certain acquisitions close when the Fed pivots, why a Series C prices at a markdown, and how capital rotation reshapes competitive positioning. She reads PitchBook, CB Insights, and S&P Capital IQ filings alongside the earnings commentary most coverage ignores. Her work focuses on M&A rationale, startup unit economics, and the policy signals that move private markets before they show up in public ones.