Nvidia's blockbuster earnings drop today could make or break the AI hype, as investors demand proof that the chip king's dominance endures amid soaring costs and market doubts.

With the stock up just 3.8% since October amid fears over massive AI bets by giants like Microsoft and Alphabet, all eyes are on whether Nvidia can deliver reassurance.

Market Pressure Mounts

The S&P 500 teeters near its January peak, down under 1%, but AI-sensitive names like Intuit and Workday have plunged over 40% this year, dragging the Magnificent Seven index 4.7% lower in 2026.

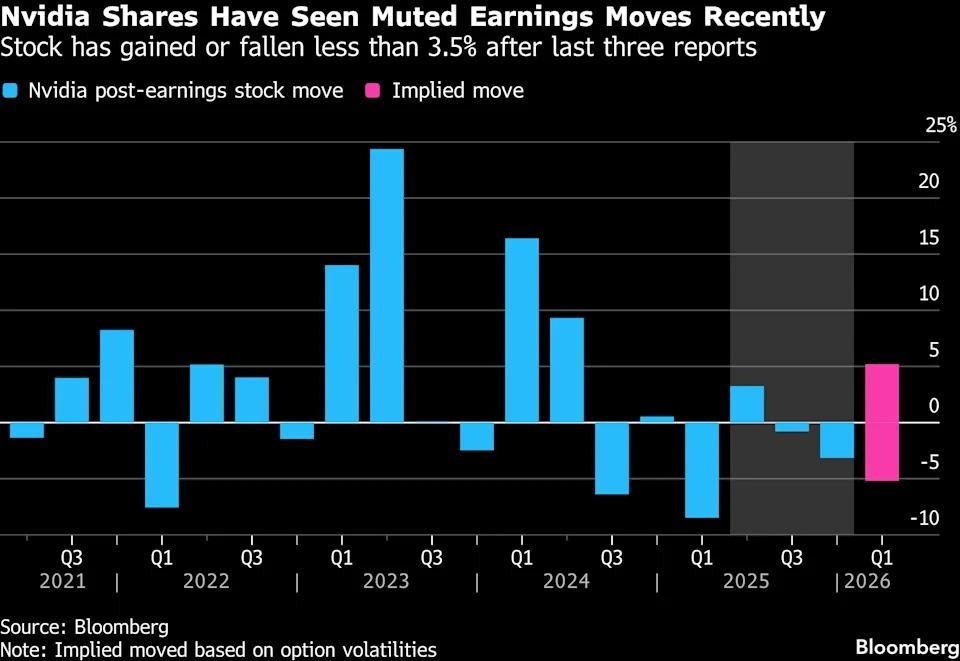

Nvidia, the world's most valuable firm at a $4.8 trillion market cap, held a massive sway as its shares climbed Wednesday, but options traders price in just a 5.6% post-earnings swing, the smallest in three years, signaling caution.

Expectations Tower High

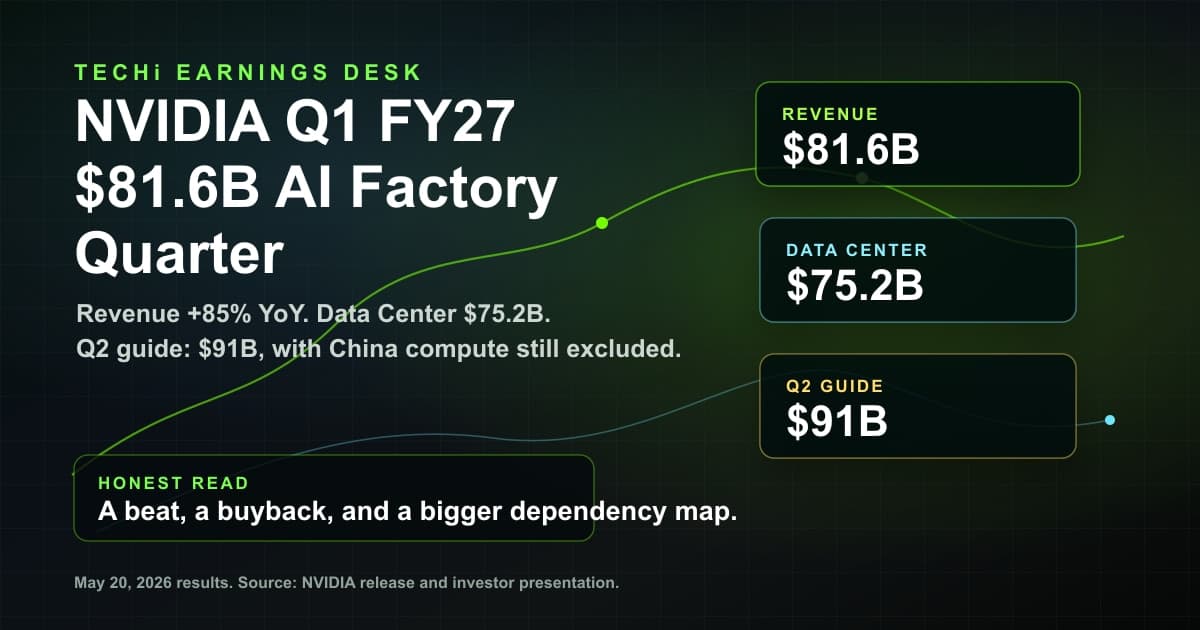

Strong growth is anticipated in Nvidia's Q4 2026 earnings, with adjusted EPS ranging from $1.46 to $1.53 and revenue estimated between $65.0B and $65.8B (67% YoY) due to the Blackwell ramp.

Although there is a risk associated with memory price increases, gross margins are anticipated to rebound to 75.0%. C

Critical Analysis and Outlook

These figures underscore Nvidia's AI stranglehold, with hyperscalers like Meta and Amazon eyeing $700 billion in 2026 capex Nvidia poised to snag 40-50%.

Yet rivals like AMD lurk with cheaper GPUs as supply eases, testing pricing power. Sustained margins would affirm demand resilience; a slip could fuel selloffs in overextended AI plays. Guidance for Q1 FY2027 around $72 billion will spotlight the AI supercycle's stamina.

If Nvidia beats and signals Rubin ramps, expect stock surges toward new highs; misses on margins or China curbs could spark broader tech retreats. Investors crave conviction that AI investments yield returns, not just endless spending.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Warisha Rashid writes about the intersection of corporate strategy, venture capital, and macro for TECHi — why certain acquisitions close when the Fed pivots, why a Series C prices at a markdown, and how capital rotation reshapes competitive positioning. She reads PitchBook, CB Insights, and S&P Capital IQ filings alongside the earnings commentary most coverage ignores. Her work focuses on M&A rationale, startup unit economics, and the policy signals that move private markets before they show up in public ones.