A growing number of members of the financial market are currently of the opinion that Taiwan Semiconductor Manufacturing Company can outperform Nvidia in performance in the year 2026. The logic behind it is simple enough: whereas Nvidia stays in control due to being the developer of the high-tech AI processors in the world, its products are being produced by TSMC to a large extent. Thereby, TSMC is advantaged by an omnipresent nature throughout the AI chip supply chain, and therefore gains lots of traction in equity markets. The TSMC equities have shown significantly higher returns compared to Nvidia in the last six months. Unlike the Nvidia, which has had a restricted upward mobility on its share prices, TSMC has enjoyed the benefits of a rising demand of advanced semiconductor devices and strong prospects of further growth.

The Essential Place of TSMC in the AI Boom in the Biosphere

Even though Nvidia is the design holder of the strongest AI processors in the world, it is not involved in their manufacturing. The company thereby uses TSMC to convert its schematics into saleable silicon, making TSMC a key element that cannot be sacrificed in the international AI manufacturing system. Moreover, Nvidia makes only a part of the range of customers that TSMC has. Most of the well-known semiconductor designers such as Broadcom, Advanced Micro Devices, Qualcomm and Apple rely on the fabrication facilities offered by TSMC. Their data-center accelerators, mobile SoCs, and personal computing platforms, which are all made of silicon, are involved in varying applications of artificial intelligence. This large base of clients gives TSMC strategic privileges that Nvidia does not have. Although the income generation of Nvidia largely depends on the level of capital expenditure on AI data-centers infrastructure, TSMC has income streams that are generated in different branches of the technological market. Therefore, with AI embracing various industries, TSMC is not susceptible to market changes that can be explained by the taste of specific chip designers.

Robust Growing Outlook for 2026

TSMC anticipates a growth of close to 30% in its 2026 revenue in U.S. dollars. This trend is driven by increased market demand of the most advanced lithographic nodes of the company that are utilized in producing AI accelerators, high-performance computing units, and new-generation consumer devices. In addition, there can be more upside than the advice that corporate disclosures can provide. The continued increase in production capacity coupled with the expected high price of the state-of-the-art process technologies will put TSMC in a position to realize growth figures much higher than present forecasts provided demand remains as robust as it currently I t makes the future of TSMC relatively more predictable than that of several artificial-intelligence experts that are too narrow-minded.

Assessment Makes TSMC better than Nvidia

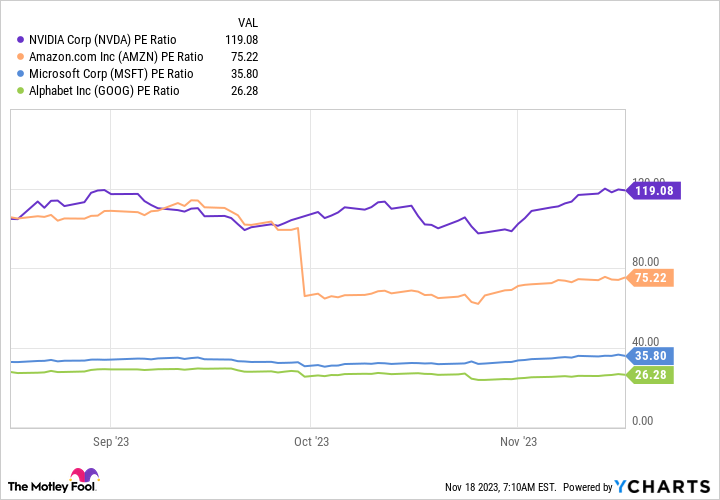

Another factor that would lead to investor interest in TSMC is relative valuation. Nvidia is very expensive with a significant increase in revenue multiple, as compared with TSMC, which indicates market hopes of a strong growth; this magnifies upside margin. Thus, the ability to make unforeseen profits is limited in the case of Nvidia compared to TSMC. However, Nvidia is estimated to be growing at a higher pace in the short-term period. The analysts anticipate significant growth in the revenues and earnings of the incumbent fiscal year, but they are already priced in the market. On the contrary, TSMC is trading at a relatively low multiple, but it has a healthy growth profile. The combination of sound valuation and booming demand makes its equity more attractive to long-term investors.

Conclusion TSMC Could Outperform in 2026

In case TSMC reaches its estimated revenue of about USD -159 billion in 2026 and still maintains similar levels of valuation multiples, its stock value may rise by a substantially large margin compared to current rates. This possible course of action is strengthened by augmentation in capacity, fortified pricing leverage, and long-term AI-related investment. TSMC, as technology analyst Harsh Chauhan of The Motley Fool, has been positioned in the middle of the entire AI chip supply chain. The company does not need to choose between rival chip design companies; instead, it provides most of their manufacturing requirements. TSMC offers a unique offer in the sphere of AI to those investors who are less concerned with current market trends and more focused on long-term investment. It provides a significant exposure to the AI revolution, provides a consistent growth, and has a way more balanced risk profile. In this regard, TSMC has a more reasonable chance of producing higher equity returns by 2026 compared to Nvidia.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Dr Layloma Rashid brings a clinical lens to healthcare investing. She translates FDA filings, Phase 3 readouts, and PDUFA calendar dates into analysis readers can act on — covering large-cap pharma, medical-device makers, and the oncology and GLP-1 pipelines reshaping the sector. Her coverage weighs ClinicalTrials.gov data against management guidance and flags where sell-side models diverge from what trial design actually supports. She writes about drug development with the skepticism Phase 2 success rates deserve.