The equity valuation of Dell Technologies has grown by 62% in the past twelve months, thereby gaining much attention in a market that has developed a major interest in AI leaders.

What was the triggering point of this sharp rise? A paradigm shift to AI infrastructure, which will be accelerated by an increase in the load on high-performance server solutions.

AI Boom Fuels the Fire

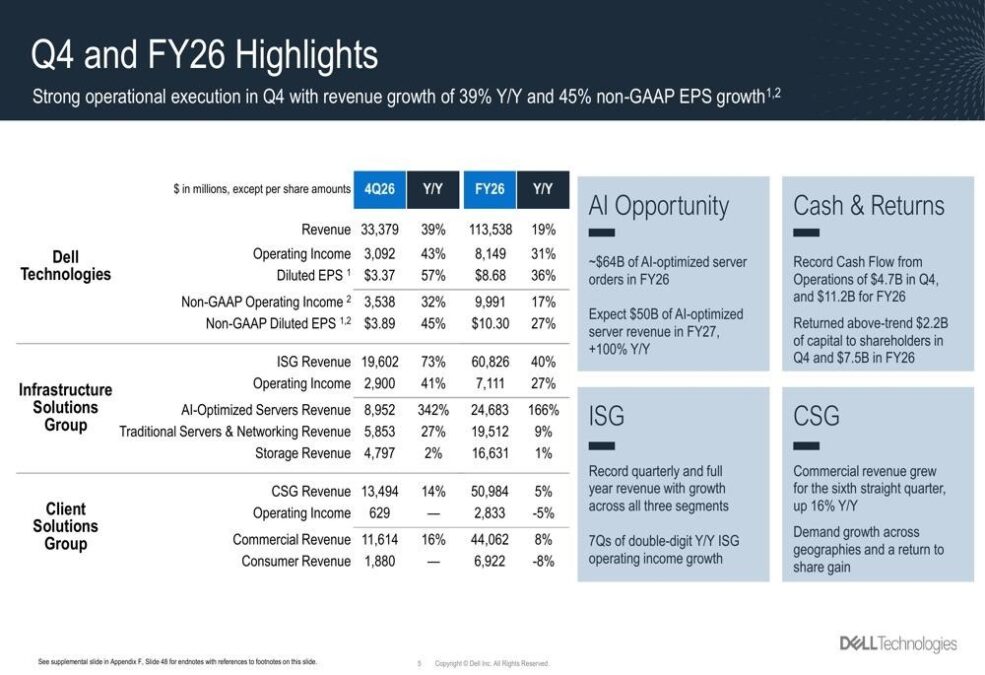

Following the announcement, the company's stock increased 1.34% in aftermarket trading to $125.14 as investors reacted favorably to both the fiscal 2027 guidance and the impressive quarterly results. Revenue of $33.4 billion exceeded projections of $31.41 billion by 6.34%, and Dell reported non-GAAP diluted earnings per share of $3.89, exceeding consensus estimates of $3.52 by 10.51%.

The best result was a backlog of AI servers worth $43 billion as of Q4, which could signal significant purchases of AI servers by businesses that seek to establish AI production plants.

David Kennedy, CFO, Dell Technologies

Yeah, sure. I think, look, I guess from a top-down perspective for guidance, let’s start with revenue, right? As we did our results, we talked about our $43 billion backlog from an AI perspective. That’s a great anchor tenant from a revenue perspective as we get into the year and look at the growth that’s potential that’s out there. You look at our Q4 results, record in terms of revenue and EPS, both on an accelerating curve as we went through the year and backended through that. You come into the year ahead and you think you’re pretty bullish then from a revenue and an AI perspective. When we look at the core business, as we’ve guided Q1, it’s more near term

DELL's FY27 and Q1 Guidance

Revenues for the first quarter of fiscal 2027 are predicted to range from $34.7 billion to $35.7 billion, with a midpoint of $35.2 billion indicating a 51% increase from the previous year.

Dell Technologies projects that the combined ISG and CSG will grow by 53% Y-O-Y at the halfway point, with ISG expected to grow by over 100%, thanks to $13 billion in revenue from AI servers and CSG which is expected to grow by about 2%.

At the halfway point, non-GAAP earnings are predicted to be $2.90 per share (+/- 10 cents), representing an 87% increase over the previous year.

Road Ahead

In the future, AI-led efforts at Dell ought to overcome the issue of the margin as the supply chains reach maturity, and the operational leverage comes into action.

Major threats exist in case the cost of the components goes awry or in case the AI euphoria dies, the consistent backlog, as well as the simultaneous stream of data centers and personal computers, points to the ongoing momentum. Any investor that goes with efficient implementation will be paid off in this high-stakes AI race despite the volatility.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Warisha Rashid writes about the intersection of corporate strategy, venture capital, and macro for TECHi — why certain acquisitions close when the Fed pivots, why a Series C prices at a markdown, and how capital rotation reshapes competitive positioning. She reads PitchBook, CB Insights, and S&P Capital IQ filings alongside the earnings commentary most coverage ignores. Her work focuses on M&A rationale, startup unit economics, and the policy signals that move private markets before they show up in public ones.