AMD set its all-time record close, $580.91, on Tuesday, June 30, 2026. It got to keep the record for exactly one session. On July 1 the stock fell 6.9% to $540.88 — about $65 billion of market value on 1.63 billion shares, a larger dollar loss than NVIDIA took the same day — and the proximate cause was a news story about a company that is not AMD.

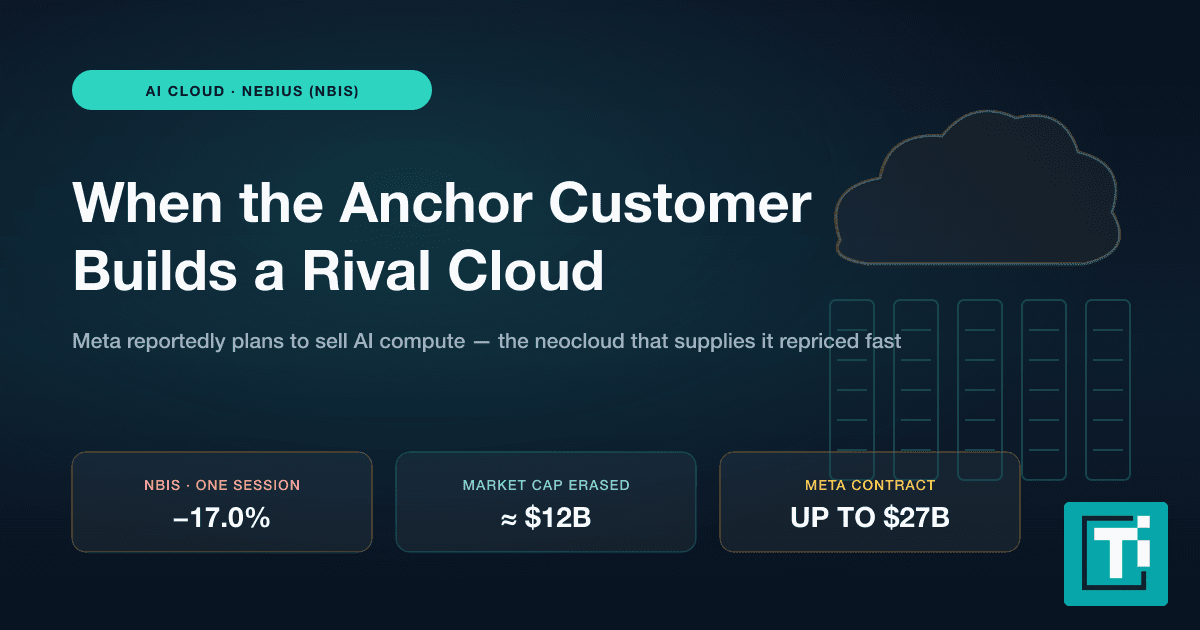

Bloomberg reported that Meta plans to sell its surplus AI computing power. For most chip stocks that was a sector headwind. For AMD it was personal. Meta is the anchor customer of AMD's entire AI acceleration story — committed, since February, to deploying up to 6 gigawatts of AMD Instinct GPUs, holding a warrant for roughly 10% of AMD's shares, and scheduled to take delivery of the first custom MI450 gigawatt in the second half of this year. When your defining customer signals it may have more compute than it needs, the market does not wait for clarification.

The uncomfortable symmetry is this: the Meta agreement is the reason AMD nearly tripled off its March low, and it is the reason July 1 cost $65 billion. The same concentration that re-rated the stock is what makes it fragile. Understanding which parts of the deal are load-bearing — and which parts the market just repriced — is the whole game from here.

- The moveAMD fell 6.9% to $540.88 on July 1 — about $65 billion erased, a bigger dollar loss than NVIDIA took the same day — one session after setting its record close of $580.91.

- The triggerMeta's reported plan to sell surplus AI compute. Meta is AMD's anchor AI customer: up to 6 gigawatts of Instinct GPUs and a warrant for roughly 10% of the company.

- What repricedOnly the first MI450 gigawatt has a shipping schedule; the other five are options that scale with Meta’s purchases. The selloff is a probability discount on the optional tranches — the same structure that hit Nebius.

- The second frontReported GDDR6 prices have roughly tripled and a 10–15% Radeon increase is reported for Q3, while the MI450 ramp needs HBM from a supply pool AMD’s rival has largely pre-booked.

- What settles itAMD's early-August report (MI450 cadence and margin guide), Meta's late-July capex commentary, and warrant-vesting disclosures in the next 10-Q.

The deal that built the breakout

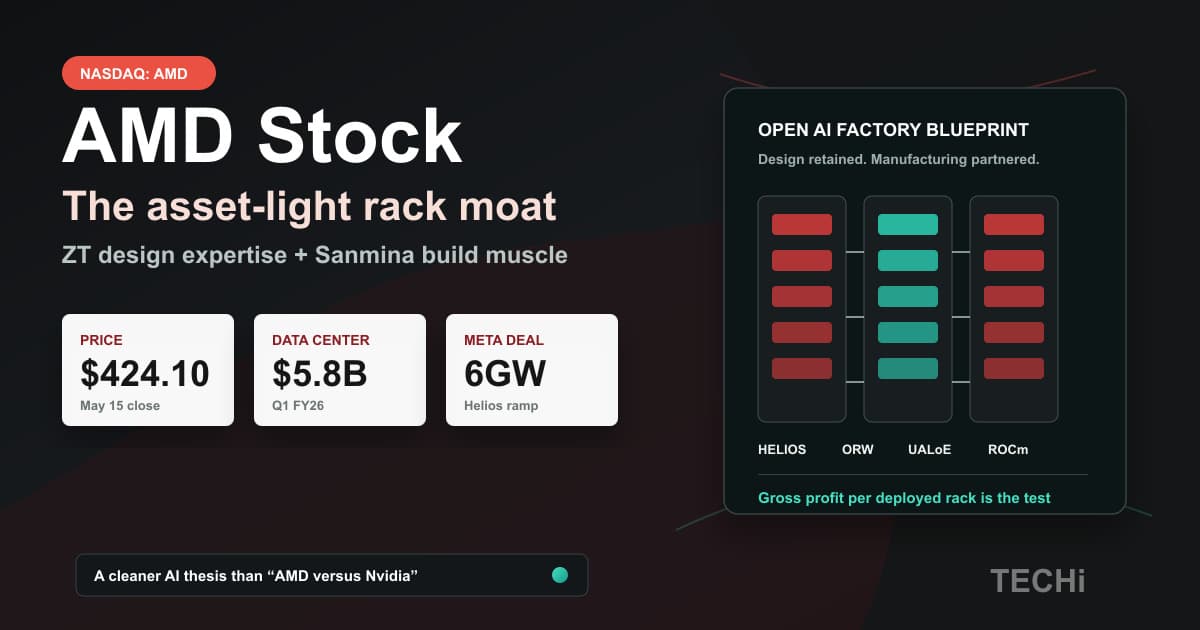

The February 24 agreement, announced by AMD and Meta directly, has three moving parts. Meta may deploy up to 6 gigawatts of Instinct GPUs across its next-generation data centers — a multiyear, multi-generation commitment. The first gigawatt runs on a custom GPU built on the MI450 architecture and optimized for Meta's workloads, with shipments beginning in the second half of 2026. And AMD issued Meta a performance-based warrant for up to 160 million shares — about 10% of the company, in a package Tom's Hardware sized at roughly $100 billion — vesting in tranches as Meta's purchases scale toward the full 6 gigawatts, conditioned on AMD stock-price thresholds and Meta milestones.

TECHi's coverage at the time framed the agreement as the deal that breaks NVIDIA's AI monopoly, and the market eventually agreed — though not immediately. The stock actually drifted to its 2026 low of $190.95 on March 3, a week after the announcement. What ignited the re-rate was evidence: the May earnings report showing Data Center revenue up 57%, the Helios rack-scale systems turning chips into deployable AI factories, and Lisa Su's escalating language about customer forecasts. From that March low to the June 30 record, AMD tripled, adding roughly $630 billion of market value. By late June, the anchor-tenant trade was the stock.

What July 1 actually repriced

Read the deal's structure against Wednesday's Bloomberg report and the selloff stops looking like sentiment and starts looking like arithmetic.

Only the first gigawatt of the Meta agreement has a delivery schedule. The other five scale with Meta's future purchasing decisions — they are options, not orders. That is the identical structure that made Nebius the day's worst casualty, as TECHi detailed in its analysis of the $15 billion backstop Meta just repriced: headline numbers built mostly of optional tranches, valued by the market as if they were backlog. A Meta that expects surplus compute — enough to build a resale business around — is a Meta less likely to exercise gigawatts two through six on anyone's schedule. AMD's $65 billion haircut is the probability discount arriving on five optional gigawatts at once.

The warrant sharpens the story in both directions. Meta's 160 million shares vest as it buys — an alignment mechanism that pays Meta to stay committed, which is genuine downside protection the neoclouds never had. But it also means AMD's largest AI customer is a future 10% shareholder whose cost basis improves as AMD's stock falls, and — if the cloud-resale plan becomes real — a company that could sell access to those very MI450 clusters in competition with AMD's other prospective buyers. There is even a quiet bull case buried in that scenario: Meta reselling MI450 capacity would put AMD silicon and the ROCm software stack in front of thousands of third-party developers who would never have provisioned it directly. Distribution is distribution, whoever operates the data center.

What the market could not do on Wednesday is distinguish between those futures. So it did what markets do with new uncertainty about old concentration: it charged for it.

The second-source premium, quantified

It is worth being precise about what the market is paying for, because it is not current revenue. AMD’s data-center business did $5.8 billion last quarter; NVIDIA’s did $75.2 billion — roughly thirteen times more. Yet at its June 30 record, AMD was valued near $947 billion, about a fifth of NVIDIA. On a per-dollar-of-data-center-revenue basis, the market was paying AMD more than double what it pays the leader.

That premium is not an accounting error; it is a thesis. It prices AMD as the industry’s designated second source at hyperscale — the vendor every buyer of AI compute wants to exist, funds deliberately, and rewards with contracts structured like the Meta agreement precisely so that a real alternative to the incumbent survives. Second-source premiums are rational while the conversion story is intact. They are also the first thing a market re-examines when the flagship conversion — six gigawatts, of which five are optional — acquires a question mark. Wednesday’s 6.9% was not the thesis breaking. It was the thesis being marked to a world where the anchor customer talks about surplus.

The memory bill arrives at the same time

The second front gets less attention because the numbers are smaller, but it presses on the same income statement. Industry supply-chain reports describe a 10–15% Radeon price increase coming as early as this quarter, driven by GDDR6 memory costs that have roughly tripled since late 2025 — from about $2.50 to $7.50 per gigabyte — as DRAM makers shift wafer capacity toward HBM for AI processors. AMD has not confirmed the pricing action, and gaming is now a small line: $720 million of Q1 revenue against $5.8 billion for Data Center.

The reason to care is not Radeon. It is that the same physics govern the MI450 ramp. High-bandwidth memory is the binding constraint on every AI accelerator program in the world, and — as TECHi examined when NVIDIA locked up SK hynix's HBM4 supply — AMD's chief rival has pre-booked a commanding share of exactly the component AMD now needs in unprecedented volume for the Meta gigawatt and everything behind it. AMD is scaling its largest GPU program ever into the tightest memory market ever, where the queue is partly owned by its competitor. First-quarter gross margin of 53% was already down a point from the fourth quarter. The margin trajectory through the MI450 ramp — not the delivery date — is where the memory market will show up in AMD's numbers.

The business under the swing is not the problem

None of this reflects operating weakness, which is what makes the setup a valuation argument rather than a distress story. AMD's first-quarter results, reported May 5, were the strongest in its history: revenue of $10.25 billion, up 38% year over year; Data Center revenue of $5.8 billion, up 57%, now — in Su's words — "the primary driver of our revenue and earnings growth"; GAAP earnings per share up 91%; record quarterly free cash flow; and second-quarter guidance of roughly $11.2 billion, implying about 46% growth. Client revenue grew 26% on Ryzen share gains. The engine is real and accelerating.

The valuation carries the argument instead. At the June 30 record, AMD was worth about $947 billion — approaching NVIDIA's league on roughly one-eighth the revenue, at something near 21 times this year's implied sales. Even after July 1, at $882 billion, the stock trades at a multiple that assumes the optional Meta gigawatts convert, the memory bill stays manageable, and a second and third anchor tenant eventually arrive to dilute the first. Those are plausible assumptions. They are also, as of Wednesday, assumptions the market has started charging for — which is the correct response to a customer that just told the world it might have spare capacity. Live pricing and fundamentals sit on TECHi's AMD quote page.

The CPU business is the quiet ballast

One reason AMD fell 7% on Wednesday rather than 17% — the fate of the pure-play suppliers — is that a large share of its income statement has nothing to do with the optional gigawatts. Client revenue grew 26% last quarter on Ryzen share gains, and the data-center line is driven by EPYC server processors alongside the Instinct ramp. Wall Street has noticed: the most recent high-profile target increase on the stock was explicitly about the CPU franchise, not GPUs, built around a dramatic expansion of the server-CPU opportunity as AI clusters multiply.

The mechanism is the attach rate TECHi examined before the May report: every rack of accelerators — anyone’s accelerators — ships with head-node CPUs, and AMD is winning a growing share of those sockets whether the GPUs beside them are its own or its rival’s. That is real ballast. If Meta’s optional tranches stretch out, the CPU and client franchises put a floor under estimates that Nebius and CoreWeave simply do not have. It is the difference between a company with a concentrated customer and a company that is only a concentrated customer.

What would settle it

Three disclosures decide whether July 1 was a discount or a warning. The first is the MI450 shipping cadence: AMD's second-quarter report in early August is the last one before first-gigawatt deliveries begin, and any change in the "second half of 2026" language moves the stock more than the revenue print will. The second is Meta's own late-July earnings call — capex guidance and any comment that turns the reported cloud business into a plan with dates. The third is the warrant table in AMD's next 10-Q: vesting activity is the cleanest public record of whether Meta's purchases are actually scaling toward tranche two.

And one number nobody should skim: gross margin guidance. If AMD can hold the mid-50s through the most memory-constrained ramp in its history, the two-front squeeze becomes a footnote. If it cannot, the market will re-run Wednesday's arithmetic with a colder eye — because a customer with surplus capacity negotiates future tranches very differently than a customer standing in line.

The near-triple off the March low was the market paying in advance for a future in which Meta buys all six gigawatts and others follow. July 1 was the first invoice disputing part of that bill. The evidence that resolves it starts arriving in about four weeks.

Not investment advice. This article is for information only. Multi-gigawatt commitments describe potential future deployments, not booked revenue; memory-pricing and Radeon-price reports are unconfirmed by AMD. Figures reflect trading on July 1, 2026 and filings and announcements available at publication. Do your own research before making investment decisions.

FAQ

Frequently asked questions

Why did AMD stock drop 7% on July 1, 2026?

AMD closed at $540.88, down 6.9% from the record $580.91 it set the day before — roughly $65 billion of market value. The trigger was Bloomberg's report that Meta plans to sell surplus AI compute: Meta is AMD's anchor AI customer, committed to up to 6 gigawatts of Instinct GPUs, so a Meta with excess capacity raises questions about the optional tranches of that deal. Profit-taking after the stock's near-triple off its March low amplified the move.

What is the AMD–Meta 6 gigawatt deal?

Announced February 24, 2026, it is a multiyear, multi-generation agreement under which Meta may deploy up to 6 gigawatts of AMD Instinct GPUs. The first gigawatt — a custom MI450-based GPU optimized for Meta's workloads — begins shipping in the second half of 2026. AMD also issued Meta a performance-based warrant for up to 160 million shares, about 10% of the company, vesting in tranches as capacity ships and subject to stock-price and milestone conditions.

Is the whole 6 gigawatts guaranteed?

No. Only the first 1-gigawatt tranche has a shipping schedule. The remaining capacity scales with Meta's future purchases — which is exactly why a report that Meta may have surplus compute to resell repriced AMD: the optional five gigawatts are the part of the deal the market had been valuing most aggressively.

How is the memory shortage affecting AMD?

Two ways. Industry reports put GDDR6 spot prices at roughly triple their late-2025 level — about $7.50 per gigabyte — and describe a 10–15% Radeon price increase coming in Q3, which AMD has not confirmed. Meanwhile the MI450 data-center ramp requires HBM, a supply pool a rival has largely pre-booked. Q1 gross margin of 53% was already down a point from Q4.

Is AMD's business still growing?

Strongly. Q1 2026 revenue was $10.25 billion, up 38% year over year, with Data Center revenue up 57% to $5.8 billion, EPS up 91%, record quarterly free cash flow, and a Q2 revenue guide of about $11.2 billion. CEO Lisa Su said customer forecasts for the MI450 series and Helios racks are exceeding AMD's initial expectations.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Umair Aslam is an ACCA-qualified finance executive based in Al Khobar, Saudi Arabia. His CV lists INSEAD Executive Education's Management Acceleration Leadership Program in 2025, so his TECHi profile treats INSEAD as completed executive education rather than current enrollment. His work sits at the intersection of corporate finance, operating discipline, financial reporting, and executive decision-making across growth markets. On TECHi, Umair focuses on finance, markets, fintech, AI adoption, and boardroom-level strategy: the practical questions executives, investors, and operators ask when numbers, policy, technology, and execution all meet. His profile is built around transparent credentials, public social links, and a clear professional beat so readers can evaluate his perspective before following his analysis.