- The reportsGoogle has reportedly committed to building more than 3 million of its TPUs at Intel from 2028, and Nvidia is testing Intel's 18A process for a future GPU.

- Why it mattersThese would be the first hyperscaler-scale external customers to validate Intel Foundry as a real alternative to TSMC.

- Not revenue yetThe volumes are 2028 programs, none of the deals are company-confirmed, and Reuters said it could not verify the reporting.

- The priceINTC closed June 12 at $124.57, up 6.5% and near its 52-week high — yet the average analyst target is $93.12, about a third below the stock.

- Next proof pointIntel Foundry still lost $2.4B last quarter; the July 22 earnings report and 18A yield data are the next checkpoints.

Intel spent three years promising investors its contract-manufacturing arm would eventually win outside customers. Last week, two of the biggest names in computing reportedly started behaving as if that promise is real — and the stock raced past the point most analysts think it is worth.

Google has reportedly committed to manufacturing more than three million of its custom AI chips at Intel, and Nvidia is said to be testing Intel's most advanced process for a future graphics chip. The companies have confirmed none of it, and the volumes that matter arrive in 2028. INTC jumped 6.5% on Friday anyway, closing at $124.57 — roughly a third above the average price target on Wall Street.

What Google and Nvidia actually agreed to

According to reporting from The Information, later picked up by Reuters, Google has decided to have Intel produce more than three million tensor processing units — the in-house chips that run its AI services — starting in 2028. That order is big enough to matter on its own: it is roughly half of Google's expected TPU output for 2027 and 2028 on Morgan Stanley's estimates, and Google reportedly made the call only after months of testing Intel's packaging.

Nvidia's role is earlier-stage and, for now, more telling than material. It is evaluating Intel's 18A process and EMIB packaging to build a GPU that fuses four graphics dies into one package, a design penciled in for around 2028. Nvidia has not placed an order — it is checking whether Intel can do the work.

Two caveats keep this short of a clean win. Intel, Google, and Nvidia have all declined to confirm the reports, and Reuters said it could not independently verify them. And none of it reaches revenue soon: these are 2028 programs, not 2026 bookings.

Why this is the validation Intel's foundry was missing

Intel Foundry's problem was never only technology. It was trust. The unit has spent years making chips mostly for Intel itself, which tells a prospective customer very little about whether they should hand over their own designs. A rumor in May that Apple might use Intel set off a similar pop — one TECHi read at the time as a test of foundry credibility — but a hyperscaler routing millions of its most strategic AI chips is a louder signal than a single consumer part.

Google and Nvidia matter because they are the customers everyone else watches. If the two companies most synonymous with AI compute are willing to move silicon away from TSMC and toward Intel, smaller buyers read that as proof the 18A process works and that a second leading-edge foundry now exists outside Taiwan. INTC has been one of the most violent re-ratings in the AI-stock complex this year, and the reason is exactly this: external validation is the missing piece the whole turnaround was waiting on.

The numbers behind the rally

Intel's first quarter gave the move something to stand on. Revenue was $13.6 billion, about $1.4 billion above the midpoint of its own guidance, and management said AI-related products made up roughly 60% of revenue and grew 40% from a year earlier. Non-GAAP gross margin landed at 41%. For the current quarter, Intel guided to $13.8–$14.8 billion.

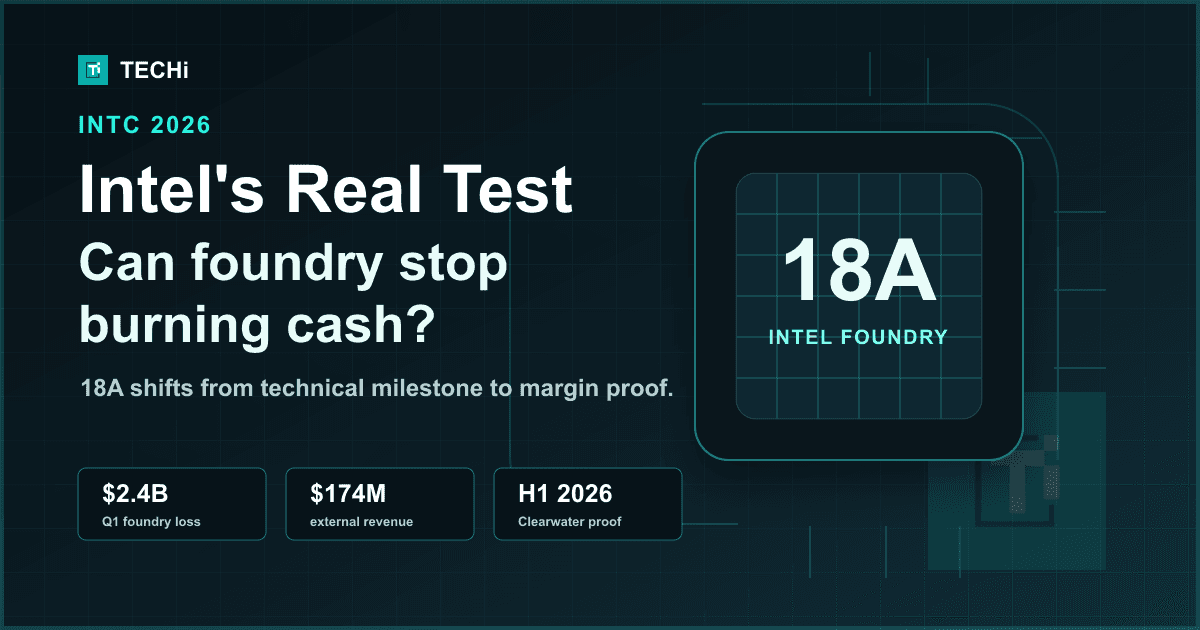

The foundry itself is still the hard part — the open question of whether it can stop burning cash has not gone away:

- Intel Foundry: $5.4B revenue, $2.4B operating loss — narrower than the prior quarter, but a long way from breakeven.

- Data Center & AI: $5.1B revenue, up 22% year over year — with $1.5B in operating income, the segment is carrying the company's profit.

- 18A yields running ahead of internal targets — the technical precondition for any Google or Nvidia work to happen at all.

What the stock is actually pricing in

Here is the part that complicates the rally. At Friday's $124.57 close, INTC sat near the top of a 52-week range that runs from $18.96 to $132.75 — and well above where most analysts say it belongs. TECHi's INTC quote page shows a consensus 12-month target of $93.12, implying about 26% downside, with 48 analysts collectively rating it a Hold. The stock trades near 147 times forward earnings while its trailing net margin is still negative.

Said plainly: the market has already paid for a foundry turnaround that the sell-side, on its published numbers, has not. That gap is the opportunity and the risk in one sentence. Confirmed contracts from Google and a real order from Nvidia would make today's price look early. Reports that quietly fade, or 18A traction that stalls, would make it look like a squeeze.

Three ways the next year plays out

- Bull — Google's order is confirmed, Nvidia turns its 18A trial into a booking, and yields hold. Intel re-rates as a credible second source to TSMC, and 2028 external revenue becomes something analysts can model.

- Base — the Google order is real but stays a 2028 event, Nvidia keeps testing without committing, and foundry losses keep narrowing slowly. The stock holds its gains but struggles to grow into a ~147x multiple without more signed names.

- Bear — the reports stay unconfirmed or slip, external 18A demand disappoints, and the AI build-out cools. The gap between $124.57 and the $93.12 target closes the hard way.

The next hard checkpoint is July 22, when Intel reports again. Until then, the foundry story leans on reports the companies will not confirm and yield curves only Intel can see. The stock is treating both as settled.

FAQ

Frequently asked questions

Did Google actually order chips from Intel?

According to reporting from The Information, Google has committed to having Intel manufacture more than three million of its TPUs starting in 2028. Intel, Google, and Nvidia have not publicly confirmed the arrangement, and Reuters said it could not independently verify it.

Is Nvidia using Intel's foundry?

Not yet. Nvidia is reportedly evaluating Intel's 18A process and EMIB packaging for a future GPU that combines four dies in one package, targeted around 2028, but it has not placed an order.

What is Intel 18A?

18A is Intel's most advanced manufacturing process and the centerpiece of its bid to win outside foundry customers. On its first-quarter 2026 call, Intel said 18A yields were running ahead of internal targets.

Why did Intel (INTC) stock jump?

Shares rose on reports that Google and Nvidia are turning to Intel's foundry. INTC closed June 12, 2026 at $124.57, up about 6.5% on the day.

Is INTC trading above analyst price targets?

Yes. At $124.57, INTC trades roughly a third above the $93.12 consensus 12-month target, which implies about 26% downside; the average rating across 48 analysts is Hold.

When does Intel report earnings next?

Intel's next quarterly results are scheduled for July 22, 2026.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Umair Aslam is an ACCA-qualified finance executive based in Al Khobar, Saudi Arabia. His CV lists INSEAD Executive Education's Management Acceleration Leadership Program in 2025, so his TECHi profile treats INSEAD as completed executive education rather than current enrollment. His work sits at the intersection of corporate finance, operating discipline, financial reporting, and executive decision-making across growth markets. On TECHi, Umair focuses on finance, markets, fintech, AI adoption, and boardroom-level strategy: the practical questions executives, investors, and operators ask when numbers, policy, technology, and execution all meet. His profile is built around transparent credentials, public social links, and a clear professional beat so readers can evaluate his perspective before following his analysis.