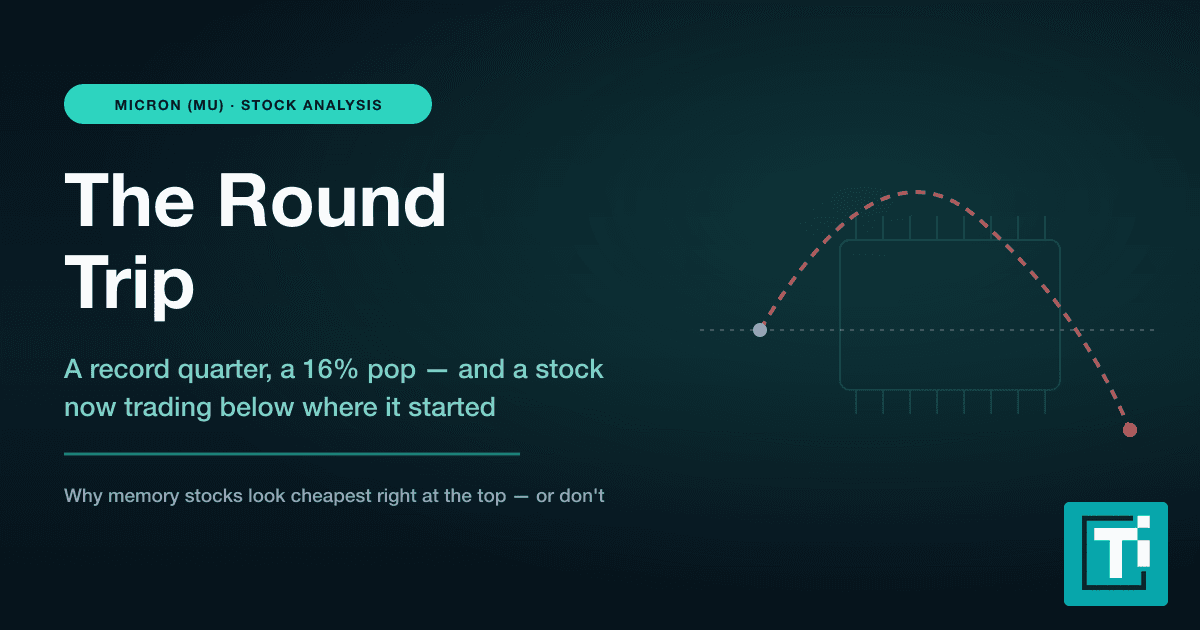

Micron walks into its fiscal third-quarter report on June 24 carrying something unusual for an earnings night: a stock that has already roughly doubled this year, and a Wall Street that spent the week before the print racing to raise price targets rather than waiting to see the numbers. Stifel lifted its target to $1,500 from $550. Wedbush went to $1,300. Half a dozen firms now sit above the $1,134 the shares closed at on June 18. The setup cuts both ways — the analysts are telling you the memory super-cycle is real, and they are also telling you a very good quarter is already in the price.

What makes June 24 a genuine event rather than a victory lap is the gap between what Micron promised and what the Street now expects. The company guided to $33.5 billion in revenue; analysts have crept above it. And the entire case rests on one figure nobody sees until the release — how fast memory prices are actually climbing, and how much higher Micron can guide for the quarter after this one.

- The dateMicron reports fiscal Q3 2026 after the close on June 24, with the call at 4:30 p.m. ET.

- The barCompany guide is $33.5B revenue and ~$19.15 EPS; consensus has moved higher to ~$19.72 EPS on ~$34.5–35.0B.

- The catalystA wave of analysts more than doubled their targets — Stifel $1,500, Wedbush $1,300 — on a triple-digit DRAM price move.

- The real tellIn a super-cycle the next guide matters more than the beat. Fiscal Q4 guidance is what moves the stock.

- The catchMU is up ~70% in 2026 and above its average target; it trades 54x trailing but only ~10x forward — the whole bet is the cycle holding.

The “double upgrade,” decoded

It is worth being precise about the headline that did the rounds, because it overstates the action. There was no "double upgrade" in the literal sense — no firm moved Micron two notches from Sell to Buy. What happened is that several analysts more than doubled their price targets while keeping their existing Buy and Outperform ratings. Stifel went to $1,500 from $550; Wedbush to $1,300; Deutsche Bank and Rosenblatt to the $1,200–$1,500 range; RBC and Citi to $1,200; Susquehanna sits highest at $1,750. The "double" describes the targets, not the ratings — a distinction that matters, because a target raise on a stock that already ran is a weaker signal than a genuine change of conviction.

The reason for the stampede is a single, specific read on pricing. Wedbush’s Matthew Bryson wrote that DRAM and NAND contract prices rose by "high double to even triple digits" quarter over quarter, with DRAM possibly up more than 100% because Micron set its contract prices earlier than its Korean rivals — leaving it room for a sharp catch-up. He now models roughly a 65% blended increase in average selling prices for the quarter, up from a prior 40% estimate. That is what the "triple-digit DRAM surge" actually refers to: contract prices, quarter over quarter, in the middle of the broader AI-driven memory super-cycle — not a number conjured for a headline.

The surge is not isolated to one analyst’s spreadsheet, either. Industry trackers describe the tightest memory market in more than a decade, with research-firm estimates pointing to prices up well over 100% across 2026 as AI data centers soak up wafer capacity that used to make consumer chips. Whether every figure holds, the direction is not in dispute: contract prices are resetting higher across both DRAM and NAND at a pace the industry rarely sees, and Micron — which sells into both — is among the most direct beneficiaries in the public market.

What the print has to deliver

Back in March, Micron guided fiscal Q3 to $33.5 billion in revenue, plus or minus $750 million, with a gross margin near 81% and non-GAAP earnings of about $19.15 a share. That guide was itself a leap — the prior quarter brought in $23.86 billion — and it has since been overtaken by the Street, which now models roughly $19.72 in EPS on about $34.5 to $35 billion of revenue. The gap is the whole point: because consensus already sits above the company’s own guide, simply hitting that guide would underwhelm. Micron has to beat the number the analysts moved to, not the one it set itself.

To see why expectations have detached from a normal quarter, follow the trajectory. A year ago Micron was doing roughly $8 billion a quarter; the most recent quarter was $23.9 billion, and the guide for this one is $33.5 billion. That is not a company growing so much as a commodity repricing in real time. Gross margin tells the same story — it has marched from the mid-30s toward a guided 81%, the kind of figure a memory maker only sees at the violent top of a pricing cycle. Every line of the model is running at an extreme, which is exactly what makes the next guide so loaded: extremes, by definition, do not last forever, and the market is trying to work out whether this one has two more quarters in it or two more years.

And even a clean beat is not the real catalyst. In a super-cycle, the market pays for the trajectory, not the quarter that just closed. The figure that will actually move the stock on June 24 is the guide for the following quarter — fiscal Q4. If management extends the pricing gains and guides revenue meaningfully higher, the doubled targets start to look earned. If it guides cautiously, even alongside a strong Q3, the read will be that the cycle is peaking, and a stock priced for acceleration does not handle "deceleration" well.

The HBM question

The piece that ties Micron most directly to the AI boom, rather than to PCs and phones, is high-bandwidth memory — the stacked DRAM that sits beside every AI accelerator. Micron expects to sell out its entire 2026 HBM capacity, has overtaken Samsung to become the number-two supplier behind SK Hynix, and — correcting a misconception that circulated earlier this year — is firmly in Nvidia’s next-generation supply chain. Nvidia certified all three memory makers, including Micron, for its Vera Rubin HBM4, not just its Korean rivals. Any update on HBM revenue, market share, or the HBM4 ramp will be parsed closely, because HBM is the highest-margin, most AI-leveraged slice of the business — the part that makes Micron a toll booth on Nvidia’s GPU boom rather than a commodity chipmaker. The same dynamic is lifting the broader HBM4 supply chain that feeds the AI build-out. By the latest reads, SK Hynix holds roughly 62% of the HBM market, Micron around 21% after passing Samsung, and Samsung near 17% — so any share gain Micron claims on the call lands against rivals the whole market is watching.

Why this cycle looks different

The bulls’ strongest argument is that this is not a normal memory cycle at all. Past booms came from undersupply that the chipmakers eventually fixed by overbuilding, which crashed prices and the stocks with them. This one is demand-led: AI servers need enormous quantities of both high-bandwidth memory and conventional DRAM, the makers have been unusually disciplined about adding capacity, and much of the new output is being absorbed by HBM rather than commodity chips. Meaningful fresh supply is not expected to loosen the market until late 2027. If that framing holds, the down-cycle that normally follows a peak like this is both shallower and further off than the history books suggest.

The bears do not dispute the demand — they dispute the durability and the price. Memory has humiliated investors who extrapolated a peak before, and a stock at a record valuation has no margin for being early. The honest read is that both sides can be right at once: the demand is real and the cycle is real, and the question Micron’s guidance will begin to answer is which of the two the next year actually belongs to.

The valuation paradox

Micron is the rare stock that looks both wildly expensive and oddly cheap, depending on which line you read. At about $1,134 it trades around 54 times trailing earnings — a number that screams late-cycle for a memory company. Yet it trades only about 10 times forward earnings, because analysts expect profits to explode as memory prices roughly double. The entire bull case lives in that gap: it is a bet that the forward number is right, that this cycle stays elevated long enough for trailing earnings to catch up to the multiple rather than the multiple collapsing to meet a normalized earnings base. The bear case is the mirror image — "forward" assumes the cycle holds, and memory cycles have a long history of not holding. It is, in one quarter, the trillion-dollar scarcity test the stock has been pointing toward all year.

The risk into the print

The caution list is real even if the demand is. The stock is up around 70% in 2026 and trades above its average analyst target — momentum has run ahead of the published numbers, which is exactly when an in-line print can still trigger a sell-off. There has been insider selling, too: CEO Sanjay Mehrotra sold roughly $38 million of stock in early June, though under a pre-arranged trading plan that predates the run, which makes it routine rather than a signal. And underneath it all sits the oldest fact about this industry: memory is the most cyclical business in technology. Buying a binary earnings event at a record valuation is the textbook way to get hurt if the guide disappoints, and with a beta above two, whatever Micron does on June 24, the move will not be gentle.

There is a read-through well beyond Micron itself, too. As the first major memory maker to report into this pricing surge, its results — and especially its forward guidance — will set the tone for the entire group: Sandisk, the Korean giants that dominate DRAM and HBM, and the equipment and materials suppliers that feed them. A blowout guide would ripple through the whole memory and semicap complex; a cautious one would pull air out of every name that has run on the same thesis. That makes June 24 a sector event, not merely a single-stock one. It is also why the reaction can overshoot in either direction — traders will be repricing the entire memory trade off one company’s outlook, and the first hard data point in a cycle this hot carries more weight than the arithmetic alone would justify.

What to watch on the call

Skip the reflex of grading the headline beat against consensus. In a name priced like this one, these are the lines that will actually decide the reaction:

- The fiscal Q4 guide. The single most important number — whether management extends the pricing surge into another quarter or signals it is cresting.

- DRAM versus NAND. Pricing and bit-shipment commentary on each, and whether the triple-digit contract move analysts flagged actually showed up in the results.

- HBM specifics. Revenue, market share, the HBM4 ramp with Nvidia, and any change to the "sold out for 2026" framing or its capacity run-rate.

- Gross margin. Whether margin pushes beyond the guided ~81% — and how management talks about its durability.

- Capex and supply. How much Micron is spending to chase demand, and what that says about how long it expects prices to stay this high.

The price targets say the super-cycle is real. The share price says a great deal of it is already paid for. June 24 is where those two statements get reconciled, and the resolution will come less from the quarter Micron just finished than from the one it guides next. A beat with a bold outlook validates the doubled targets and likely drags the whole memory complex up with it; a beat with a careful outlook reminds everyone that memory has always been a cycle dressed up, for a while, as a growth story — and that the safest time to own one is rarely the week the targets all double. For the live price and the latest analyst targets as the report approaches, Micron’s quote page carries the current numbers.

FAQ

Frequently asked questions

When does Micron report earnings?

Micron Technology reports fiscal third-quarter 2026 results on June 24, 2026, after the US market closes, with a conference call scheduled for 4:30 p.m. Eastern.

What is Micron expected to report?

Micron guided to $33.5 billion in revenue and about $19.15 in non-GAAP EPS for the quarter. Wall Street consensus is slightly higher, near $19.72 EPS on roughly $34.5 to $35.0 billion in revenue, as analysts model the surge in memory prices.

Why did analysts raise their Micron price targets?

Several firms more than doubled their targets in June 2026 — Stifel to $1,500, Wedbush to $1,300, and RBC and others to $1,200 — citing sharply rising DRAM and NAND contract prices. Wedbush's analyst estimated DRAM contract prices could be up triple digits quarter over quarter. These were target raises on maintained ratings, not formal rating upgrades.

Did Nvidia choose Micron for HBM4?

Yes. Nvidia certified all three major memory makers — SK Hynix, Samsung and Micron — for its Vera Rubin HBM4 platform in 2026, with Micron supplying a share behind SK Hynix and Samsung. Micron also expects to sell out its 2026 high-bandwidth memory capacity.

Is Micron stock too expensive before earnings?

Micron has roughly doubled in 2026 and trades around 54 times trailing earnings — but only about 10 times forward earnings, because analysts expect profits to surge with memory prices. The risk is that it is a binary earnings print at a record valuation in a historically cyclical industry.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Dr Layloma Rashid brings a clinical lens to healthcare investing. She translates FDA filings, Phase 3 readouts, and PDUFA calendar dates into analysis readers can act on — covering large-cap pharma, medical-device makers, and the oncology and GLP-1 pipelines reshaping the sector. Her coverage weighs ClinicalTrials.gov data against management guidance and flags where sell-side models diverge from what trial design actually supports. She writes about drug development with the skepticism Phase 2 success rates deserve.