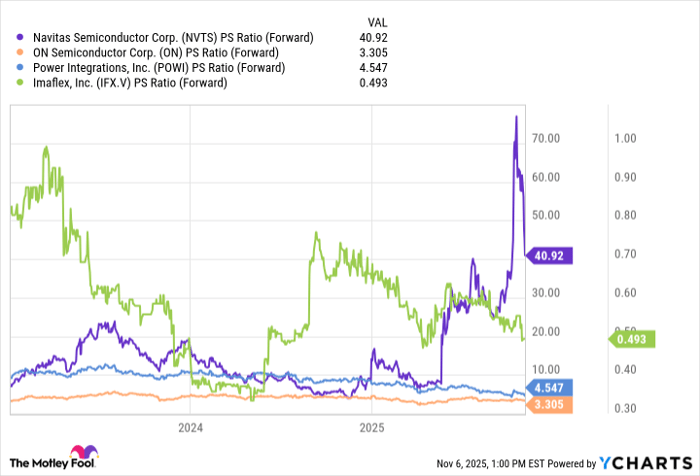

Navitas Semiconductor's shares have nearly tripled over the past year, surging to $8.48 as of February 24, 2026, up 4.43% intraday amid booming AI data center demand. This power chip specialist, trading at a lofty 28 times its trailing $56 million revenue, is betting big on gallium nitride (GaN) tech to fuel energy-hungry servers.

Company Shift

Founded in 2014, Navitas pioneered GaN power ICs for efficient conversion in smartphones and chargers, but consumer sales have waned with 38% trailing revenue drop.

Now pivoting to AI infrastructure, it eyes data centers needing 98% efficient supplies to cut costs on next-gen chips from Nvidia partners. Q3 2025 revenue fell to $10.1 million from $21.7 million year-prior, with a $19 million loss reflecting the transition pains.

Market Potential

Analysts peg Navitas' addressable market exploding 66-87% yearly to $1.4-2.5 billion by 2030, tapping a $2.6 billion 800V data center slice via GaN/SiC combos. "Navitas's integrated power ICs offer scalable solutions for trillion-dollar power shifts in AI and EVs," notes AInvest analysis on its Nvidia tie-up. Yet Q4/full-year 2025 results due post-market today could sway sentiment.

Valuation Risks

Wall Street's mixed: average price target $6.40-$6.74 implies 20-25% downside, with holds dominating despite two buys. Forecasts show 2026 revenue dipping to $36-48 million before rebound, as growth lags until 2027 ramps. At $1.9 billion market cap and -220% margins, the stock prices are in perfection amid beta 3.17 volatility.

Outlook

Navitas holds explosive upside if AI delivers triple density, 30% loss cuts but patience is key. Wait for revenue inflection post-Q4; a miss could trigger pullbacks, while design wins spark rallies toward $13 highs. For risk-tolerant tech bulls, it's a pivotal watch in semiconductors' power race.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Fatimah Misbah Hussain is a seasoned financial journalist at TECHi, specializing in stock market analysis, commodities, and tech sector finance. With a strong background in monitoring public markets and tech companies, she breaks down complex stock movements and commodity price trends into actionable insights.