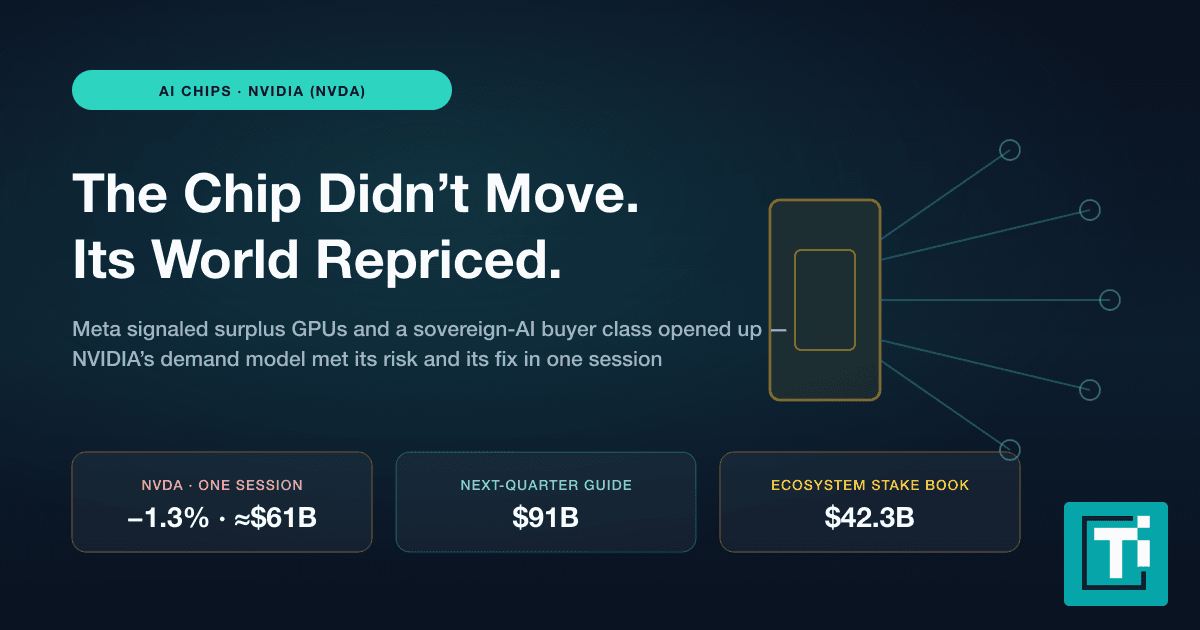

The share price of Nvidia dropped by approximately 5 % in 2026, but the company still has an operating high capacity business, and so it is up to the investors to decide whether the present decline in the share price is an opportunity of buying it or a red flag.

Strong Earnings Powered by AI Demand

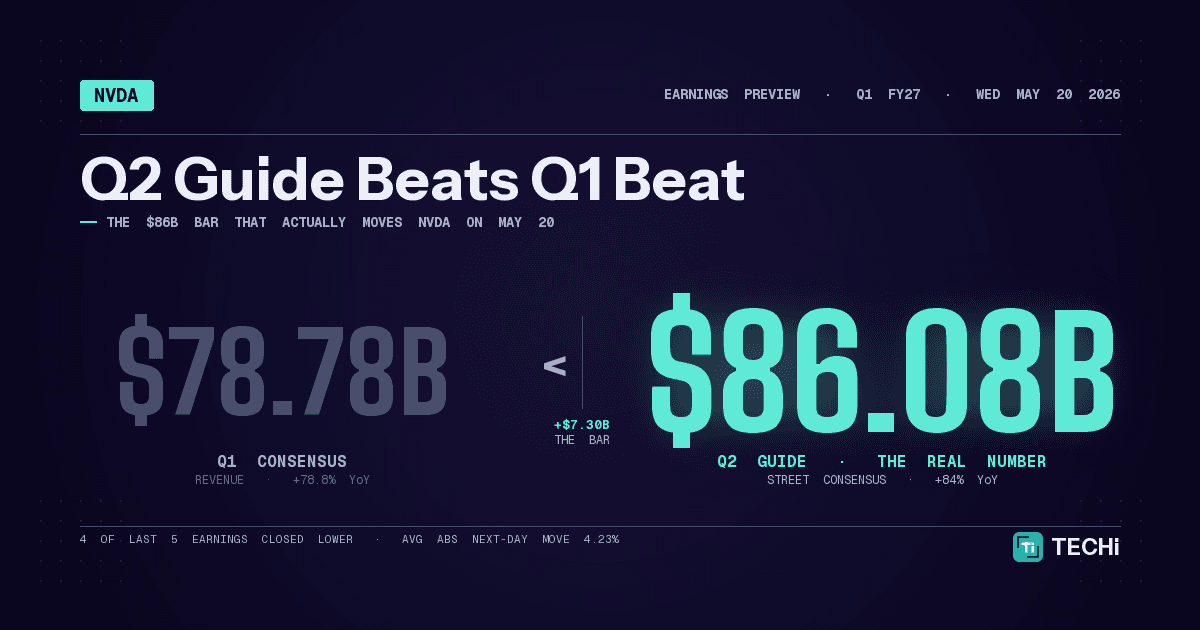

In the fourth quarter of fiscal 2026, Nvidia achieved the highest overall revenue in its history with a record of $68.1 billion and that is 73%, compared to 20% above Wall Street expectations.

CEO Jensen Huang noted in the company's earnings release

"Computing demand is growing exponentially, the agentic AI inflection point has arrived,"

The sale of data-centers motivated by the need to buy AI GPUs increased by 75% to reach $62.3 billion. The net income increased by nearly two years in a row with the diluted earnings per share increasing by 98% to about $1.76 billion.

Revenue increased to $215.9 billion in the entire fiscal year, 65% growth continues to indicate how central Nvidia is in AI infrastructure spend.

Valuation confronts the increasing competition

The valuation of Nvidia is still strong, with a price-to-earnings ratio of some 36.29 and a market capitalization valuation of $4.32 trillion as of March 7, 2026, with little discretionary space available to revise downwards.

At the same time, hyperscale clients like Amazon, Alphabet and Microsoft are hastening their investment in in-house chips e.g. Trainium and Tensor Processing Units to decrease reliance on Nvidia and to decrease the expenses of AI compute.

The actual benefit of the pullback

Nvidia projects first-quarter fiscal 2027 income of a little more than $78 billion, meaning that even following the previous year’s burst it will keep growing exponentially.

A lot of information about the company's most recent quarter (and entire year) of operations can be found in NVIDIA's most recent earnings report. NVIDIA spent $40 billion on share buybacks during that time, which is one of the more intriguing facts from the annual report.

However, the concentration in a small number of hyperscalers, and the risk of price pressure, and a high-priced valuation multiple all indicate a stock that is priced to have long-term dominance over the traditional growth story. To investors with volatility tolerance and still convinced of Nvidia's ability to protect its AI lead against the custom silicon.

Those with a more conservative outlook will have to wait for a final assessment of the dominance's resilience, but the current decline can be viewed as an opportunity to establish a modest, measured holding.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Warisha Rashid writes about the intersection of corporate strategy, venture capital, and macro for TECHi — why certain acquisitions close when the Fed pivots, why a Series C prices at a markdown, and how capital rotation reshapes competitive positioning. She reads PitchBook, CB Insights, and S&P Capital IQ filings alongside the earnings commentary most coverage ignores. Her work focuses on M&A rationale, startup unit economics, and the policy signals that move private markets before they show up in public ones.