On 15 January 2026, Taiwan Semiconductor manufacturing Co. lightened up the markets with an overwhelming 35% improvement to 505.74 billion (NT, 16 billion) contrasting with its fourth-quarter profits forecasts.

The demand for artificial-intelligence chips was insatiable and led to this growth. Revenues amounted to NT$1.046 trillion, $33.73 billion higher than estimated, and the indicator showed eight consecutive quarters of increase in profits.

Record Breaker

The proportion of fourth-quarter wafer revenue of advanced process nodes of 7nm or below was 77% compared to 74 % of the total year 2025 where the overall revenue increased by 31.6 % to NT$3,809.05 billion as compared to the same period in 2024.

High-performance computing, which incorporated AI and 5G, was the order of the day, as it made sales after the smartphone and computer market demanded slump amidst memory impairments. Gross margin was 62.3%, net profit margin was at 48.3% with a good pricing power.

AI Engine Roars

Competitive strength of TSMC is manifested at its manufacture of state of the art processors on Nvidia and AMD companies where small nanometer technology produces faster more efficient processors.

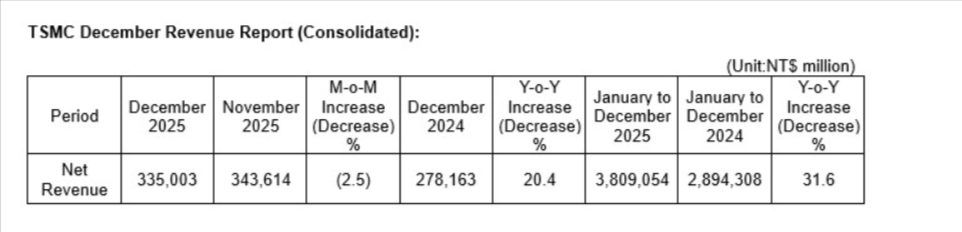

TSMC reported that its consolidated net revenue was NT$335.0 billion in December 2025, down 2.5% from November 2025 but up 20.4% from December 2024. This dominance expands this moat over competitors who fail in the technology of the leader.

Expert Take

The demand for AI remains very strong, driving overall chip demand across the entire server industry.

Counterpoint Research senior analyst Jake Lai told CNBC, predicting that 2026 will be another “breakout year” for AI server demand, Lai said.

With TSMC’s ongoing 2nm capacity expansion and new production contributing to revenue, along with continuous expansion of advanced packaging. TSMC is expected to maintain strong performance in 2026.

2026 Power Surge

IDC projects the revenue of TSMC will grow by 25-30% in USD terms with AI accelerators growing by 78% annually. However, the company is also subject to risks related to the possibility of a slump in consumer electronics.

The capacity expansions and price hikes of elite nodes put TSMC in a position to ride on the AI wave which may reach $300 billion in revenue by the year 2030.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Warisha Rashid writes about the intersection of corporate strategy, venture capital, and macro for TECHi — why certain acquisitions close when the Fed pivots, why a Series C prices at a markdown, and how capital rotation reshapes competitive positioning. She reads PitchBook, CB Insights, and S&P Capital IQ filings alongside the earnings commentary most coverage ignores. Her work focuses on M&A rationale, startup unit economics, and the policy signals that move private markets before they show up in public ones.