The public AI economy has added a net +$2.15T of market value since the end of 2025, based on a TECHi basket of 20 companies most directly tied to AI compute, cloud distribution, models, memory, networking, semicap equipment and enterprise AI software. The same basket stood at $28.087T at 2025 year-end and $30.236T on May 6, 2026, using the company-by-company market-cap history pages linked throughout this report.

That number needs one serious caveat: this is AI-economy market-cap change, not a perfect claim that every dollar was caused by AI. Apple, Microsoft, Amazon, Alphabet and Meta move for advertising, devices, cloud, rates, regulation, margins and buybacks too. But AI is now one of the central valuation arguments for the whole basket, and the market is putting a very large number on the companies that supply the compute, software, memory, networking and distribution layer.

The strongest signal is not NVIDIA alone. It is the way value spread across the stack. Alphabet, TSMC, Amazon, Micron, Broadcom, AMD, ASML, Arm and Arista all added market value in different parts of the AI chain, while Microsoft, Meta, Tesla, Salesforce, Adobe, ServiceNow, Oracle and Palantir show the other side of the story: AI exposure does not automatically protect a stock when investors question timing, margins, monetization or valuation.

- Net value addedThe TECHi AI Economy Top 20 moved from $28.087T at 2025 year-end to $30.236T on May 6, 2026, a net increase of +$2.15T.

- Gross winners were biggerPositive contributors added +$3.34T, while valuation drags removed -$1.20T, producing the net +$2.15T increase.

- The stack mattersThe wealth was not created by one category; it spread across chips, foundry, memory, networking, cloud, devices, models and enterprise software.

- AI exposure is not immunityMicrosoft, Meta, Palantir, Tesla, Salesforce, Adobe and ServiceNow remained AI-critical but still lost market cap in this measurement window.

Methodology: What TECHi Counted

TECHi built this report around a public-market basket of 20 companies that sit closest to the AI economy: accelerator compute, hyperscale cloud, model distribution, advanced foundry, semicap equipment, high-bandwidth memory, AI networking, enterprise AI software, operating platforms and GPU cloud.

Market-cap figures come from CompaniesMarketCap, using each company's current market-cap page and its end-of-year historical market-cap series. The report compares the 2025 year-end market cap with the current 2026 market cap shown on the company page at the time of the May 6, 2026 research pull.

This is not a factor model. It does not isolate AI from interest rates, buybacks, product cycles, advertising growth, cloud margins, currency or regulatory risk. It answers a narrower but useful question: how much public-market value has moved inside the companies most responsible for building and distributing the AI economy?

%22%2F%3E%3Crect%20width%3D%221600%22%20height%3D%22900%22%20fill%3D%22url(%23grid)%22%2F%3E%3Crect%20width%3D%221600%22%20height%3D%22900%22%20fill%3D%22url(%23glow)%22%2F%3E%0A%20%20%20%20%3Ctext%20x%3D%2288%22%20y%3D%22104%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2225%22%20font-weight%3D%22900%22%20letter-spacing%3D%223%22%20fill%3D%22%2393fff0%22%3ETECHi%20RESEARCH%20REPORT%3C%2Ftext%3E%0A%20%20%20%20%3Ctext%20x%3D%2288%22%20y%3D%22178%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2262%22%20font-weight%3D%22950%22%20fill%3D%22%23ffffff%22%3EThe%20AI%20Economy%20Market-Cap%20Ledger%3C%2Ftext%3E%0A%20%20%20%20%3Ctext%20x%3D%2288%22%20y%3D%22222%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2225%22%20font-weight%3D%22650%22%20fill%3D%22%23d9fffb%22%3ETop%20positive%20contributors%20since%202025%20year-end%2C%20with%20valuation%20drags%20separated.%3C%2Ftext%3E%0A%20%20%20%20%3Cg%20transform%3D%22translate(88%20704)%22%3E%0A%20%20%20%20%20%20%3Crect%20width%3D%221310%22%20height%3D%22104%22%20rx%3D%2218%22%20fill%3D%22%2308141b%22%20opacity%3D%220.68%22%20stroke%3D%22%23ffffff%22%20stroke-opacity%3D%220.10%22%2F%3E%0A%20%20%20%20%20%20%3Ctext%20x%3D%2234%22%20y%3D%2242%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2224%22%20font-weight%3D%22850%22%20fill%3D%22%23ffffff%22%3EBasket%20moved%20from%20%2428.087T%20to%20%2430.236T%3C%2Ftext%3E%0A%20%20%20%20%20%20%3Ctext%20x%3D%2234%22%20y%3D%2274%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2223%22%20font-weight%3D%22750%22%20fill%3D%22%2399fff0%22%3ENet%20value%20added%3A%20%2B%242.15T%20%E2%80%A2%20Gross%20winners%3A%20%2B%243.34T%20%E2%80%A2%20Drags%3A%20-%241.20T%3C%2Ftext%3E%0A%20%20%20%20%3C%2Fg%3E%0A%20%20%20%20%3Ctext%20x%3D%22170%22%20y%3D%22246%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2218%22%20font-weight%3D%22900%22%20letter-spacing%3D%222%22%20fill%3D%22%2393fff0%22%3ETOP%20POSITIVE%20CONTRIBUTORS%3C%2Ftext%3E%0A%20%20%20%20%3Cg%3E%0A%20%20%20%20%20%20%3Ctext%20x%3D%22170%22%20y%3D%22290%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2223%22%20font-weight%3D%22800%22%20fill%3D%22%23f8fffd%22%3EGOOG%3C%2Ftext%3E%0A%20%20%20%20%20%20%3Crect%20x%3D%22270%22%20y%3D%22268%22%20width%3D%22610.0%22%20height%3D%2230%22%20rx%3D%2215%22%20fill%3D%22url(%23bar)%22%2F%3E%0A%20%20%20%20%20%20%3Ctext%20x%3D%22902%22%20y%3D%22291%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2222%22%20font-weight%3D%22800%22%20fill%3D%22%23f8fffd%22%3E%2B%24853.00B%3C%2Ftext%3E%0A%20%20%20%20%3C%2Fg%3E%3Cg%3E%0A%20%20%20%20%20%20%3Ctext%20x%3D%22170%22%20y%3D%22338%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2223%22%20font-weight%3D%22800%22%20fill%3D%22%23f8fffd%22%3ETSM%3C%2Ftext%3E%0A%20%20%20%20%20%20%3Crect%20x%3D%22270%22%20y%3D%22316%22%20width%3D%22339.7%22%20height%3D%2230%22%20rx%3D%2215%22%20fill%3D%22url(%23bar)%22%2F%3E%0A%20%20%20%20%20%20%3Ctext%20x%3D%22631.68347010551%22%20y%3D%22339%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2222%22%20font-weight%3D%22800%22%20fill%3D%22%23f8fffd%22%3E%2B%24475.00B%3C%2Ftext%3E%0A%20%20%20%20%3C%2Fg%3E%3Cg%3E%0A%20%20%20%20%20%20%3Ctext%20x%3D%22170%22%20y%3D%22386%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2223%22%20font-weight%3D%22800%22%20fill%3D%22%23f8fffd%22%3EAMZN%3C%2Ftext%3E%0A%20%20%20%20%20%20%3Crect%20x%3D%22270%22%20y%3D%22364%22%20width%3D%22326.8%22%20height%3D%2230%22%20rx%3D%2215%22%20fill%3D%22url(%23bar)%22%2F%3E%0A%20%20%20%20%20%20%3Ctext%20x%3D%22618.8112543962486%22%20y%3D%22387%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2222%22%20font-weight%3D%22800%22%20fill%3D%22%23f8fffd%22%3E%2B%24457.00B%3C%2Ftext%3E%0A%20%20%20%20%3C%2Fg%3E%3Cg%3E%0A%20%20%20%20%20%20%3Ctext%20x%3D%22170%22%20y%3D%22434%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2223%22%20font-weight%3D%22800%22%20fill%3D%22%23f8fffd%22%3EMU%3C%2Ftext%3E%0A%20%20%20%20%20%20%3Crect%20x%3D%22270%22%20y%3D%22412%22%20width%3D%22287.1%22%20height%3D%2230%22%20rx%3D%2215%22%20fill%3D%22url(%23bar)%22%2F%3E%0A%20%20%20%20%20%20%3Ctext%20x%3D%22579.0790152403283%22%20y%3D%22435%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2222%22%20font-weight%3D%22800%22%20fill%3D%22%23f8fffd%22%3E%2B%24401.44B%3C%2Ftext%3E%0A%20%20%20%20%3C%2Fg%3E%3Cg%3E%0A%20%20%20%20%20%20%3Ctext%20x%3D%22170%22%20y%3D%22482%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2223%22%20font-weight%3D%22800%22%20fill%3D%22%23f8fffd%22%3EAVGO%3C%2Ftext%3E%0A%20%20%20%20%20%20%3Crect%20x%3D%22270%22%20y%3D%22460%22%20width%3D%22253.2%22%20height%3D%2230%22%20rx%3D%2215%22%20fill%3D%22url(%23bar)%22%2F%3E%0A%20%20%20%20%20%20%3Ctext%20x%3D%22545.1535756154749%22%20y%3D%22483%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2222%22%20font-weight%3D%22800%22%20fill%3D%22%23f8fffd%22%3E%2B%24354.00B%3C%2Ftext%3E%0A%20%20%20%20%3C%2Fg%3E%3Cg%3E%0A%20%20%20%20%20%20%3Ctext%20x%3D%22170%22%20y%3D%22530%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2223%22%20font-weight%3D%22800%22%20fill%3D%22%23f8fffd%22%3EAMD%3C%2Ftext%3E%0A%20%20%20%20%20%20%3Crect%20x%3D%22270%22%20y%3D%22508%22%20width%3D%22163.9%22%20height%3D%2230%22%20rx%3D%2215%22%20fill%3D%22url(%23bar)%22%2F%3E%0A%20%20%20%20%20%20%3Ctext%20x%3D%22455.9062133645956%22%20y%3D%22531%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2222%22%20font-weight%3D%22800%22%20fill%3D%22%23f8fffd%22%3E%2B%24229.20B%3C%2Ftext%3E%0A%20%20%20%20%3C%2Fg%3E%3Cg%3E%0A%20%20%20%20%20%20%3Ctext%20x%3D%22170%22%20y%3D%22578%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2223%22%20font-weight%3D%22800%22%20fill%3D%22%23f8fffd%22%3EASML%3C%2Ftext%3E%0A%20%20%20%20%20%20%3Crect%20x%3D%22270%22%20y%3D%22556%22%20width%3D%2299.9%22%20height%3D%2230%22%20rx%3D%2215%22%20fill%3D%22url(%23bar)%22%2F%3E%0A%20%20%20%20%20%20%3Ctext%20x%3D%22391.93130128956625%22%20y%3D%22579%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2222%22%20font-weight%3D%22800%22%20fill%3D%22%23f8fffd%22%3E%2B%24139.74B%3C%2Ftext%3E%0A%20%20%20%20%3C%2Fg%3E%3Cg%3E%0A%20%20%20%20%20%20%3Ctext%20x%3D%22170%22%20y%3D%22626%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2223%22%20font-weight%3D%22800%22%20fill%3D%22%23f8fffd%22%3ENVDA%3C%2Ftext%3E%0A%20%20%20%20%20%20%3Crect%20x%3D%22270%22%20y%3D%22604%22%20width%3D%2298.0%22%20height%3D%2230%22%20rx%3D%2215%22%20fill%3D%22url(%23bar)%22%2F%3E%0A%20%20%20%20%20%20%3Ctext%20x%3D%22389.9718640093787%22%20y%3D%22627%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2222%22%20font-weight%3D%22800%22%20fill%3D%22%23f8fffd%22%3E%2B%24137.00B%3C%2Ftext%3E%0A%20%20%20%20%3C%2Fg%3E%0A%20%20%20%20%3Cg%20transform%3D%22translate(960%20252)%22%3E%0A%20%20%20%20%20%20%3Crect%20x%3D%220%22%20y%3D%220%22%20width%3D%22440%22%20height%3D%22360%22%20rx%3D%2222%22%20fill%3D%22%2308141b%22%20opacity%3D%220.58%22%20stroke%3D%22%23ffffff%22%20stroke-opacity%3D%220.10%22%2F%3E%0A%20%20%20%20%20%20%3Ctext%20x%3D%2250%22%20y%3D%2254%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2220%22%20font-weight%3D%22900%22%20letter-spacing%3D%222%22%20fill%3D%22%23ffb4b4%22%3EVALUATION%20DRAGS%3C%2Ftext%3E%0A%20%20%20%20%20%20%3Cg%3E%0A%20%20%20%20%20%20%3Ctext%20x%3D%2250%22%20y%3D%22118%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2223%22%20font-weight%3D%22800%22%20fill%3D%22%23f8fffd%22%3EMSFT%3C%2Ftext%3E%0A%20%20%20%20%20%20%3Ctext%20x%3D%22168%22%20y%3D%22118%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2223%22%20font-weight%3D%22800%22%20fill%3D%22%23ffb4b4%22%3E-%24570.00B%3C%2Ftext%3E%0A%20%20%20%20%3C%2Fg%3E%3Cg%3E%0A%20%20%20%20%20%20%3Ctext%20x%3D%2250%22%20y%3D%22166%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2223%22%20font-weight%3D%22800%22%20fill%3D%22%23f8fffd%22%3EMETA%3C%2Ftext%3E%0A%20%20%20%20%20%20%3Ctext%20x%3D%22168%22%20y%3D%22166%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2223%22%20font-weight%3D%22800%22%20fill%3D%22%23ffb4b4%22%3E-%24136.00B%3C%2Ftext%3E%0A%20%20%20%20%3C%2Fg%3E%3Cg%3E%0A%20%20%20%20%20%20%3Ctext%20x%3D%2250%22%20y%3D%22214%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2223%22%20font-weight%3D%22800%22%20fill%3D%22%23f8fffd%22%3EPLTR%3C%2Ftext%3E%0A%20%20%20%20%20%20%3Ctext%20x%3D%22168%22%20y%3D%22214%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2223%22%20font-weight%3D%22800%22%20fill%3D%22%23ffb4b4%22%3E-%24123.96B%3C%2Ftext%3E%0A%20%20%20%20%3C%2Fg%3E%3Cg%3E%0A%20%20%20%20%20%20%3Ctext%20x%3D%2250%22%20y%3D%22262%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2223%22%20font-weight%3D%22800%22%20fill%3D%22%23f8fffd%22%3ETSLA%3C%2Ftext%3E%0A%20%20%20%20%20%20%3Ctext%20x%3D%22168%22%20y%3D%22262%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2223%22%20font-weight%3D%22800%22%20fill%3D%22%23ffb4b4%22%3E-%24118.00B%3C%2Ftext%3E%0A%20%20%20%20%3C%2Fg%3E%3Cg%3E%0A%20%20%20%20%20%20%3Ctext%20x%3D%2250%22%20y%3D%22310%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2223%22%20font-weight%3D%22800%22%20fill%3D%22%23f8fffd%22%3ECRM%3C%2Ftext%3E%0A%20%20%20%20%20%20%3Ctext%20x%3D%22168%22%20y%3D%22310%22%20font-family%3D%22Inter%2C%20Arial%22%20font-size%3D%2223%22%20font-weight%3D%22800%22%20fill%3D%22%23ffb4b4%22%3E-%24100.34B%3C%2Ftext%3E%0A%20%20%20%20%3C%2Fg%3E%0A%20%20%20%20%3C%2Fg%3E%0A%20%20%20%20%3Cimage%20href%3D%22data%3Aimage%2Fpng%3Bbase64%2CiVBORw0KGgoAAAANSUhEUgAAALgAAAAsCAYAAADWxHKSAAAACXBIWXMAAAPoAAAD6AG1e1JrAAAKj0lEQVR4nO2de2wcVxWHT%2BLYhPBQy6MVQqIIFRqgDQHxEqIgECCgggYo4h%2BkIgJpGpVSEhA0JHH6UiAkEgghZOdR2gJV7bn3ztpZrx07sfMuJSAQaUtJS6kKhCS0TRMSO17v%2FaE7e8a%2BHs%2Fuzu7OrnfdOdLxrndm7vPbs2fOfQwB2AFgCECmDroLwH4At5IvKfUtUuJRcsUBcsVhT5U4SK78EylnuXdOe%2Fv8yfMTSaQcAXAcedGovWTNn1wu1zlZgJTaSiN7QCmVpR4XrBM0OAByZTsXMgE8kcoEwBMMX44hr6WOM%2BAdkwVQYivtGQQpkSVXgnWCBjIg6SSAJ1KdAPgrA%2F6s1vqjAN4D4P0A3lcDfa%2FW%2BoMA3jzpdrhySwJ4IvUA%2FG8AXsWfzaNaS1dXS9yAA1hQR51WJtNmdcq3ZN%2BYsgFoiTHPliJ5tZRzflQpkO78ojwNDy%2BYpuYzC%2FAnAVzCiXuF7Dh6tLX92LG2uHXF0aOt1NXVNgm48beVGPPAzutFyqTNZ%2Bu5tokFjyAMdu2NUzOJBfjxulpw8w0zkklvoocPgwYy457VzusEHdgH2tVzZynA%2FbICeC2Adq31hmIKYD2AjQA6AWxj7eRo0lYA6yJcf7dxuThfrx4AFgO4H0BHIM1NpdKMoqZuANYCuCysj3y4Wa8BsMLky%2Fn%2FqEI11%2F4EwHeDVtlq9%2BUA7uJ2MfndA%2BCrYWUs03qvstJdz%2Ble79fVOjmfh3I%2BR0psIleuI1duICU2klK3FQc85SwnV2yhlLiLXOeemqix0il5OymxdlKlY%2F7fSFJ%2BeFolwhvDqyyAq%2BoQBdJa6wl%2Bc5vJV2v9Ms7%2FU%2Fz5RC3y5ddRAEuCnWzB9g4Ox8YVEdPeH62fBrAwkJf%2F%2Bkc%2BN2fVfcg%2FpxzIrTQXAng8JN0H%2BXjeOOb%2FybdDpnc7HToAyqSzlElrzyvoSZ0sDvhg%2FwgdPgga3D1BQ7sRqw7uztKRQ8YNWevl1dHRGrUhCgD%2BNh%2FAKMohyxka4ZqL3F6rAoB%2Fgj8fi5pemWU18j8AVwfq7b1euHDhCgBP%2BVD4YOjq8vWiXgAeA9BWAPDDfM641TYD1QBu2hTAsZB07%2BXzWmYArkQn7e7Pu7rmfi7l3cv9ozjg0hmivl1TF8WrY3k%2F21nj5TU8vHDGTUKEAZ4A4JOdG0ELWayC1wQ6PQj4JwtY8KJpRlErzfOFAAfwKz7nYsCC6yry9r9YT1j1DAL%2BsNXu%2FvmDMQAeZsHvKwi4qzo8wF05Sq4cp5Qy758uDrgrhj2fOH%2Fjh5jVH8xZzYBP%2FeyUISGA18VFAXBLRMBjyddyUa7x621BdpnW%2BrnAuTbclYqf1j8BvLyhAc%2Bkd3gewUAmSwMZ7UXmelOn5gzgo6OjVwI4C%2BBMBH2xgJ86qrV%2BodB15pgBiX%2FCv8n5t9kuSgjg54ulGUX5elO3%2Fxg%2F2wLc62gAn7bqEwTcyFmt9cly1eSntX7e%2BNkNbMHz6QvxcVJqDSm1iqS8hYS4lZT6WinAhzw3woTtpkJ4Qc2RK3UBzRW57iIN9E0BfuxYm%2FdtnK6RG6erq6uNrXgxNTeib%2BFBJ%2FNz70Pgd8zPjTXkm7Vi6Sy2Qqo%2BZB%2FxEpvqDD%2FNmwFcrrV%2Be4TyldK3%2BqAFIjg3WnXx1cj58fHx2wGYL%2F%2Frq9DXhERtGgPwCIkWBjyza4T2j4D6%2Byaovw%2BhuqvHzCOZqcZKp3vDr8lr1gsFKvH9am4yyxGrU0yHneN6T04hMGEuPh7518QC%2FFovsanO8NP0Q1sV%2FUKVyNsHfIUFme1G%2FdguY8x5zwHAXXknKZkhKRxSUs5QVzoknUdJiedJiVOkxGnWU%2BSKF0g5R0jJbnKFmnm9EKRErxcSlPIzJOUXSallnkp5PbnuDeQ4i7mQkRqJf7aLaYsVMw8D%2FA4%2B3lYqrTIAXxY1zShaAPCbbMCt99f651kx8oq04QHPj1y2TVMzoFjxQM9UgH2nZ5FtN8ZESPIhm29MG5YPFshISm2mfcNmBmGWelNgzYclTSw8xpHMCBZ8Y5Na8DDALwJ4Jx%2BPfSS4YQD3I21mPEXJ46TkI6TEUVJmurXoKw64eS2sHJ4R93N4ZupG1IQBh7wbyJWTMAev9wGXYgvDPE5KaNYsf2k2cDkSwMPzTgAH1y3ds91zedO9WUr3ai84knJPxGDB5X3hgO8Gye6VBS14DSZbRW3ABPDGBpzducfKAjwlOjkql%2FckzLoCJZ9JAK894L4PfgeAvWZVk9a6rxzllVB7zPyQJgF8Dx%2F7gJk6wHVIl1Hffrt%2Fog30yG3sCZhBRO25uko%2BmwBee8C%2FwMf7qxgI8gdrDjQJ4Hv52DKrDhXPj0kAbw7AUz54VcwJGWoywK%2BzXIyy5uUkgFcgCeDxSQJ4AnjioiBxUV5KgG8G8HsAI7x1Rjk6orV%2BBMDPmuwm80PmS8l12FdGfQ%2FaUykSwJsjTLiQw1%2FV6IImCxO2cEw7Uv343FbDocVlxOmyCeCzDXgSB69lHDwBfNYBb612PkjIjL5GB3x%2BYK1oKZ1fYslaEwKeDNVXU59GB3xe%2FVb0NLIF3ztkrsta020nvDTnlgWfTcDn1SDvBPBIgJul%2Fmbdp3TOkhIXWM%2Fl5xJ0r51DQ%2FX1dlGyZicxv4xzdrpswwJO5C81egN1d7%2B7NdW9ZJFSS422dncvoa6upZRKXU4xyhy24CsDgHtxc631D%2B0yxpx3AngJwOsudQbc7%2Byv8PFLALwyBrUXW3jlNOtDA4B7VjyXy704MTHxbQBv0lq%2Fuoo8FxVpywTwooDnJ6zPe%2BbMmUtPjo5eafTg6dOmHFNzzpsD8OCiY3%2FTnOd4Y9N%2FVaq8qv0EgL%2Bb9aCcn71CqdCIoeaBErNo%2Bd8V5nuaB2sK7YuSAF4McKuTVpoV3AzEdTMq0viAz%2Ba2EVfkcrkzNdw24qkGXlVfY8BdcW%2F4krWMyeymMgD%2FntWwX66F3zpLgNd64x%2B%2FTg6fM16DjX8ef%2Bla8HTvA95SoYy18t7sD3dwv1lbeXMZgK%2B2OuVLNQb8Uv7Z9uDWWl9gODdU66IEt26LSX1ozxXa2WpsbOyqXC53Iuat27Kc3pNFLLiZN%2BKHJU3djfTHAPhfQtLdabc5X%2BQvnezwBgeVGPXGVFwBckWJna2KlyZ%2FjnRWkxTDJJxekiLN2kNS7CPH%2Bax3TpEt2CxA1tQR8NdZnYeYLHg9Nt80Hf0uzs%2B%2B2fRhX8Irf2LNV%2Bc3AVoUBrjW%2Bs812nwzbC7KQzP6x2%2BHgcwO%2Bt0R0OBAlgYHNA3vMVua%2FLdywGOSWQL8FQB%2BYSwCgO285fFDAD5vlylimj5cVwMQWusHAPyG9bdmw0jeTnl7FbqNy%2FpLAG%2B06xJSDuObL%2BXQ4bqYtk%2F%2BQchEL78t1%2FK20f6W0abea6rhiLe5uNtOV2v9awBft%2Bs63dB230gp50FSTiel5DZKyZ2kxOaiG%2BDXSdtCfPCaAD7XJdkAv5EeYTKVv2cttdbfqSfgUR5LUgFcrSGaPMKkAik73bBHmOS3K6nrQ6hmqHkoFe%2Fb99PEgicSu7Dl9pz5Ao%2F%2Bq6f6MdsbuGwJ4Ik01YNgS0kCeCLxiokemPV%2BWutD%2FDiK2VQTU%2F0DgI9x2RpiDksi1LTyf5QDcD9JDYqgAAAAAElFTkSuQmCC%22%20x%3D%221268%22%20y%3D%22802%22%20width%3D%22244%22%20height%3D%2258%22%20preserveAspectRatio%3D%22xMidYMid%20meet%22%20opacity%3D%220.96%22%2F%3E%0A%20%20%3C%2Fsvg%3E)

The Answer: A Net +$2.15T Added

The 20-company basket increased from $28.087T at 2025 year-end to $30.236T on May 6, 2026. The net increase was +$2.15T, or 7.7%.

The positive side was larger than the headline number. Winners in the basket added +$3.34T of market value, led by Alphabet, TSMC, Amazon, Micron, Broadcom and AMD. Drags subtracted -$1.20T, led by Microsoft, Meta, Palantir, Tesla and Salesforce.

The Top 20 AI Economy Market-Cap Ledger

1. NVIDIA (NVDA)

- Market-cap ledger: 2025 year-end market cap $4.638T, current market cap $4.775T, change +$137.00B.

- AI company type: AI accelerator and full-stack compute platform.

- How the AI contribution happened: NVIDIA remains the cleanest public-market proxy for AI compute because GPUs, networking, CUDA software and rack-scale systems sit directly under model training and inference demand. Source.

- Main internal players: Jensen Huang, Colette Kress, Ian Buck.

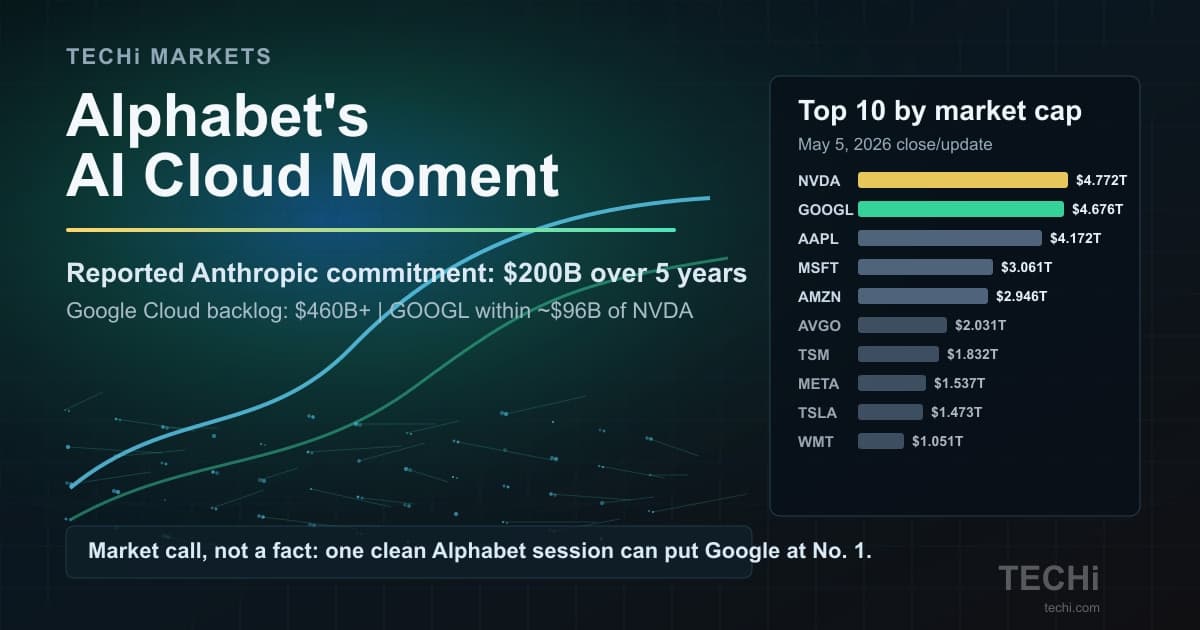

2. Alphabet (GOOG)

- Market-cap ledger: 2025 year-end market cap $3.802T, current market cap $4.655T, change +$853.00B.

- AI company type: Model lab, search distributor and cloud AI platform.

- How the AI contribution happened: Alphabet captures AI value through Gemini, Google Search distribution, YouTube/ads data, TPUs and Google Cloud. Source.

- Main internal players: Sundar Pichai, Demis Hassabis, Thomas Kurian.

3. Apple (AAPL)

- Market-cap ledger: 2025 year-end market cap $4.057T, current market cap $4.173T, change +$116.00B.

- AI company type: Device distribution and on-device AI platform.

- How the AI contribution happened: Apple is not valued like an AI infrastructure vendor, but Apple Intelligence gives it a distribution layer for private, on-device and personal AI across iPhone, iPad and Mac. Source.

- Main internal players: Tim Cook, Craig Federighi, John Giannandrea.

4. Microsoft (MSFT)

- Market-cap ledger: 2025 year-end market cap $3.625T, current market cap $3.055T, change -$570.00B.

- AI company type: AI cloud, productivity software and OpenAI distribution partner.

- How the AI contribution happened: Microsoft is the enterprise distribution layer for AI through Azure, Copilot, GitHub and its OpenAI relationship, even though its 2026 market cap has lagged this basket so far. Source.

- Main internal players: Satya Nadella, Amy Hood, Kevin Scott.

5. Amazon (AMZN)

- Market-cap ledger: 2025 year-end market cap $2.485T, current market cap $2.942T, change +$457.00B.

- AI company type: Hyperscale cloud and AI infrastructure provider.

- How the AI contribution happened: Amazon captures AI value through AWS infrastructure, Bedrock, Trainium/Inferentia chips and the retail/logistics data layer that can absorb AI automation. Source.

- Main internal players: Andy Jassy, Matt Garman, Rohit Prasad.

6. TSMC (TSM)

- Market-cap ledger: 2025 year-end market cap $1.570T, current market cap $2.045T, change +$475.00B.

- AI company type: Advanced semiconductor foundry.

- How the AI contribution happened: TSMC is the manufacturing toll road behind the AI chip cycle because advanced nodes and packaging capacity turn GPU and ASIC demand into silicon supply. Source.

- Main internal players: C.C. Wei, Wendell Huang, Kevin Zhang.

7. Broadcom (AVGO)

- Market-cap ledger: 2025 year-end market cap $1.669T, current market cap $2.023T, change +$354.00B.

- AI company type: Custom AI silicon and networking infrastructure.

- How the AI contribution happened: Broadcom benefits from hyperscaler custom accelerators, networking silicon and VMware-driven enterprise infrastructure scale. Source.

- Main internal players: Hock Tan, Charlie Kawwas, Kirsten Spears.

8. Meta Platforms (META)

- Market-cap ledger: 2025 year-end market cap $1.671T, current market cap $1.535T, change -$136.00B.

- AI company type: Consumer AI, open models and AI-powered advertising.

- How the AI contribution happened: Meta turns AI into value through ranking, recommendations, ad efficiency, Llama/open models and AI assistants across Facebook, Instagram, WhatsApp and Quest. Source.

- Main internal players: Mark Zuckerberg, Susan Li, Yann LeCun.

9. Tesla (TSLA)

- Market-cap ledger: 2025 year-end market cap $1.580T, current market cap $1.462T, change -$118.00B.

- AI company type: Autonomy, robotics and AI-enabled vehicles.

- How the AI contribution happened: Tesla is in the basket because much of its premium depends on autonomy, robotaxi and robotics optionality rather than only vehicle deliveries. Source.

- Main internal players: Elon Musk, Ashok Elluswamy, Lars Moravy.

10. Oracle (ORCL)

- Market-cap ledger: 2025 year-end market cap $568.85B, current market cap $533.07B, change -$35.78B.

- AI company type: AI cloud infrastructure and enterprise database layer.

- How the AI contribution happened: Oracle is an AI infrastructure trade through cloud capacity, database workloads and partnerships that put model training and enterprise data closer together. Source.

- Main internal players: Safra Catz, Larry Ellison, Clay Magouyrk.

11. ASML (ASML)

- Market-cap ledger: 2025 year-end market cap $416.38B, current market cap $556.12B, change +$139.74B.

- AI company type: EUV lithography and semiconductor equipment.

- How the AI contribution happened: ASML is the upstream bottleneck because EUV lithography is essential for the leading-edge chips that power AI accelerators and advanced CPUs. Source.

- Main internal players: Christophe Fouquet, Roger Dassen, Jim Koonmen.

12. AMD (AMD)

- Market-cap ledger: 2025 year-end market cap $350.01B, current market cap $579.21B, change +$229.20B.

- AI company type: AI accelerators, CPUs and adaptive compute.

- How the AI contribution happened: AMD is the challenger compute supplier, with AI GPU, CPU and data-center products giving cloud customers leverage beyond one supplier. Source.

- Main internal players: Lisa Su, Jean Hu, Forrest Norrod.

13. Salesforce (CRM)

- Market-cap ledger: 2025 year-end market cap $253.30B, current market cap $152.96B, change -$100.34B.

- AI company type: Enterprise AI agents and customer workflow software.

- How the AI contribution happened: Salesforce is the customer-data and enterprise-agent layer, but the stock shows that software AI narratives still have to prove monetization. Source.

- Main internal players: Marc Benioff, Brian Millham, Clara Shih.

14. Adobe (ADBE)

- Market-cap ledger: 2025 year-end market cap $150.08B, current market cap $103.32B, change -$46.76B.

- AI company type: Creative generative AI and digital experience software.

- How the AI contribution happened: Adobe owns a core creative workflow surface through Firefly, Creative Cloud and Experience Cloud, but investors remain cautious about pricing, cannibalization and competition. Source.

- Main internal players: Shantanu Narayen, David Wadhwani, Anil Chakravarthy.

15. ServiceNow (NOW)

- Market-cap ledger: 2025 year-end market cap $159.79B, current market cap $94.89B, change -$64.90B.

- AI company type: Enterprise workflow automation and AI agents.

- How the AI contribution happened: ServiceNow is a workflow-AI compounder because agents are most valuable when they can execute inside enterprise processes, tickets and approvals. Source.

- Main internal players: Bill McDermott, Amit Zavery, Jon Sigler.

16. Palantir (PLTR)

- Market-cap ledger: 2025 year-end market cap $449.77B, current market cap $325.81B, change -$123.96B.

- AI company type: Operational AI platform and decision software.

- How the AI contribution happened: Palantir is the operational AI layer: its value case rests on AIP turning models into controlled workflows for governments and enterprises. Source.

- Main internal players: Alex Karp, Shyam Sankar, Ryan Taylor.

17. Arm Holdings (ARM)

- Market-cap ledger: 2025 year-end market cap $116.99B, current market cap $221.78B, change +$104.79B.

- AI company type: CPU IP and edge-AI architecture.

- How the AI contribution happened: Arm captures AI value through power-efficient CPU IP that reaches cloud servers, phones, PCs, automotive systems and edge devices. Source.

- Main internal players: Rene Haas, Jason Child, Dipti Vachani.

18. Micron Technology (MU)

- Market-cap ledger: 2025 year-end market cap $320.53B, current market cap $721.97B, change +$401.44B.

- AI company type: AI memory and HBM supplier.

- How the AI contribution happened: Micron is a direct AI infrastructure beneficiary because high-bandwidth memory is now one of the scarcest ingredients in accelerator systems. Source.

- Main internal players: Sanjay Mehrotra, Mark Murphy, Sumit Sadana.

19. Arista Networks (ANET)

- Market-cap ledger: 2025 year-end market cap $166.02B, current market cap $214.33B, change +$48.31B.

- AI company type: AI data-center networking.

- How the AI contribution happened: Arista benefits from AI clusters that require high-speed, low-latency Ethernet networking between accelerators, storage and compute nodes. Source.

- Main internal players: Jayshree Ullal, Andy Bechtolsheim, Anshul Sadana.

20. CoreWeave (CRWV)

- Market-cap ledger: 2025 year-end market cap $38.08B, current market cap $67.55B, change +$29.47B.

- AI company type: GPU cloud and AI compute utility.

- How the AI contribution happened: CoreWeave is the purest public GPU-cloud utility in the basket, giving model builders leased access to scarce accelerator capacity. Source.

- Main internal players: Michael Intrator, Brian Venturo, Brannin McBee.

What The Market Is Actually Paying For

The AI value pool is not one business model. It is a stack.

At the bottom sits the hard infrastructure layer. NVIDIA supplies accelerators, systems, software and networking. TSMC manufactures the leading-edge silicon. ASML supplies the lithography chokepoint. Micron supplies high-bandwidth memory. Arista supplies AI data-center networking. CoreWeave rents accelerator capacity as a cloud utility.

Above that sits the hyperscaler and platform layer. Amazon Bedrock, Microsoft AI, Google Gemini and Oracle AI all represent attempts to make models, data, cloud infrastructure and enterprise deployment easier to buy.

Then comes the application and workflow layer. Salesforce Agentforce, Adobe Firefly, ServiceNow AI Agents and Palantir AIP are all trying to turn AI from a demo into work that gets executed inside customer systems.

The Standout Story Is Not Just Chips

NVIDIA added +$137.00B in this window, but Alphabet added +$853.00B, TSMC added +$475.00B, Amazon added +$457.00B, and Micron added +$401.44B. That tells us investors are not only buying the GPU story; they are buying the whole AI supply chain.

The flip side matters too. Microsoft, Meta, Tesla, Palantir, Salesforce, Adobe and ServiceNow all remain AI-critical companies, yet each posted a negative market-cap change in this measurement window. That does not mean their AI strategies failed. It means AI exposure is no longer enough by itself. Investors are now asking whether AI turns into revenue, margin, defensible product advantage or real customer adoption quickly enough to justify valuation.

Why This Wealth Was Created

The first reason is scarcity. The AI economy is constrained by accelerators, advanced packaging, HBM memory, networking and data-center power. When a scarce input becomes central to the next platform shift, public markets capitalize the bottleneck.

The second reason is distribution. Alphabet, Microsoft, Amazon, Apple and Meta already own huge customer surfaces. If AI becomes a daily interface, the companies with the largest distribution layers can monetize it through cloud consumption, ads, subscriptions, devices and enterprise software.

The third reason is workflow control. Salesforce, Adobe, ServiceNow and Palantir matter because enterprises do not pay for models in the abstract; they pay when models enter sales, service, creative, document, operations, defense and compliance workflows.

The fourth reason is optionality. Tesla, Apple and Meta carry AI optionality that is harder to measure in quarterly revenue but deeply embedded in the valuation conversation: autonomy, on-device agents, consumer AI, robotics, smart glasses and new interfaces.

What Would Change The Number Next

The next leg of wealth creation depends on whether AI moves from capex promise to cash-flow proof.

For infrastructure companies, the test is supply durability: can NVIDIA, TSMC, Micron, Broadcom, ASML, AMD and Arista keep converting AI demand into high-margin revenue without a supply glut? For hyperscalers, the test is utilization: can Amazon, Alphabet, Microsoft and Oracle earn attractive returns on the AI data centers they are building? For software companies, the test is monetization: can agents and copilots produce visible seat expansion, usage pricing, retention or margin leverage?

That is why this report should not be read as a victory lap. It is a ledger. The market has already created trillions of dollars of AI-linked value. The next phase has to justify it.

FAQ

Frequently asked questions

How much market value did the TECHi AI Economy Top 20 add since 2025 year-end?

The basket increased from $28.087T at 2025 year-end to $30.236T on May 6, 2026, a net increase of +$2.15T. The figure uses CompaniesMarketCap current and historical market-cap pages for each company.

Does this mean AI caused every dollar of the market-cap change?

No. This is an AI-economy basket measurement, not a factor model. Market caps also move because of rates, margins, regulation, non-AI products, buybacks, currency and investor sentiment.

Which company added the most market value in the basket?

Alphabet added the most in this measurement window at +$853.00B, followed by TSMC, Amazon, Micron and Broadcom.

Why are non-model companies like TSMC, ASML and Micron included?

They are included because AI value depends on the physical supply chain: advanced foundry capacity, EUV lithography, high-bandwidth memory and networking. Model labs cannot scale without that infrastructure.

Why did some AI companies lose market cap?

AI exposure does not guarantee stock performance. Microsoft, Meta, Tesla, Palantir, Salesforce, Adobe, ServiceNow and Oracle were drags in this window because investors also price growth expectations, margins, valuation, execution risk and non-AI business performance.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

CEO of TECHi. Building the operating system for serious tech investors. Previously led engineering at scale. Focus: AI capex thesis, semiconductor supply chain, and the equity tape.