AppLovin is not moving like a normal software stock anymore. At 12:31 p.m. ET on Thursday, May 28, 2026, APP was trading at $599.24, up +5.5% on the day, after already adding roughly 25% in a week. That is the sort of tape that makes traders ask the wrong question first: "Can it explode tomorrow?" The better question is whether Friday, May 29, has enough fresh fuel to keep buyers pressing a stock that is already back above $600.

- Friday setupTECHi's one-day formula points to a directional model price near $605.83, with a breakout attempt likely only if APP holds the $600 area and clears today's $605.05 high with volume.

- One-year mapThe TECHi one-year research signal points to $701.11, while the forecast map has a stress case near $566.79, a base case near $635.58, and a bull case near $711.14.

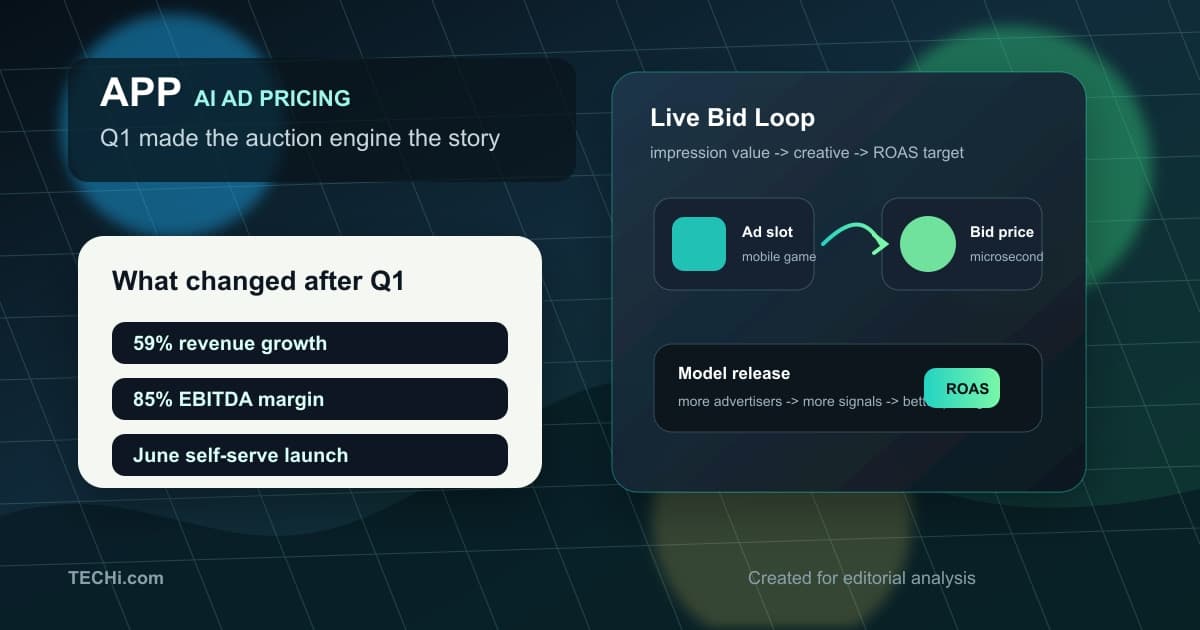

- Fundamental fuelAppLovin reported Q1 revenue of $1.842 billion, net income of $1.206 billion, and adjusted EBITDA of $1.557 billion, then guided Q2 adjusted EBITDA margin to about 84% to 85%.

- Risk lineThis is a high-multiple momentum trade after a violent run. The setup is attractive, but only with defined risk and respect for valuation compression.

The Friday setup is real, but it is not clean

The live APP quote page shows the immediate tension. The stock's May 28 range ran from $560.49 to $605.05, with the latest TECHi quote-stack print at $599.24 as of 2026-05-28T16:55:38.000Z. That puts the tape close enough to the intraday high that a Friday gap or early push through $605 can matter, but not far enough away from the low to pretend risk has disappeared.

The trade plan is simple. A constructive Friday needs APP to stay above $600 after the opening auction, then turn $605.05 into support rather than resistance. If that happens, the next magnetic zone is not mysterious: TECHi's one-day model sits at $605.83, and the seven-day model rises to $611.82. A hotter tape can overshoot toward $615 to $620, but below $590 the breakout idea starts looking tired. A clean loss of the mid-$570s would turn the move into a failed chase, not a dip to buy automatically.

Why the $600 move has fundamental backing

The rally is not just a chart line. AppLovin's Q1 2026 results showed revenue up 59% year over year to $1.842 billion, net income up 109% to $1.206 billion, and adjusted EBITDA up 66% to $1.557 billion. The company also guided Q2 revenue to $1.915 billion to $1.945 billion and adjusted EBITDA to $1.615 billion to $1.645 billion. That guidance implies an adjusted EBITDA margin of roughly 84% to 85%, which is why the market keeps treating APP less like a normal ad-tech name and more like an AI pricing engine with operating leverage.

That distinction matters. A stock can run for one day on analyst notes. It does not usually hold a one-year re-rating unless the business model is converting incremental demand into cash flow at a rate investors did not expect. AppLovin's numbers are unusually direct on that point: the revenue base is growing, the margin structure is already elite, and the company is telling investors that the next quarter should preserve the same basic economics.

The market is also paying for a specific product moment. In AppLovin's Q1 earnings presentation, management said the web self-serve version of the platform would open globally in June, described consumer pilot spend as running about 25% above January levels by March, and said April produced a record month for consumer campaign spend. The same presentation framed a path where 100,000 customers spending about $70,000 per year could represent roughly $7 billion of annual ad spend. That is not guidance, but it is the scale argument behind the premium multiple.

What TECHi's formula says now

The TECHi stocks formula is not screaming "buy anything at any price." It is more useful than that. The APP forward model reads Balanced watch with a composite score of 60/100 and low confidence of 49/100 because several analyst, sentiment, and provider fields are not fully populated in the local quote stack. The high-quality business signal is doing most of the work: quality scores 100/100, momentum scores 79/100, track record scores 75/100, and technical tape scores 69/100. Valuation pressure is the brake at 30/100.

That mix is exactly how APP should be read on May 28. The fundamentals and trend are strong enough to keep buyers engaged, but the price is no longer cheap enough for a lazy chase. The APP forecast page points to $605.83 for the one-day model, $611.82 for the seven-day model, $622.01 for the 30-day model, and $701.11 for the one-year model. Those are model levels, not promises. The model's own one-day backtest is noisy, and the article should not pretend a one-session forecast has scientific precision.

Outside analyst targets leave room for the same debate. The StockAnalysis APP forecast page lists an average target near $648, a high target of $860, and a low target of $280, with recent notes including a $700 Needham target and a $720 Morgan Stanley target. TECHi's one-year model around $701.11 is therefore above the average target but not outside the current Street range.

Tomorrow advice: buy strength only if the tape confirms it

For Friday, May 29, the right answer is not "buy because it went up." The right answer is to make the stock prove that Thursday's move was accumulation rather than exhaustion.

Aggressive traders can treat a hold above $600 and a reclaim of $605.05 as the constructive trigger. If APP opens strong, pulls back, and buyers defend the $600 area, the odds improve that momentum accounts press toward the $605.83 to $620 zone. The better version of the trade is a controlled retest and push, not a vertical gap that traps buyers at the top of the first candle.

New money should be stricter. If APP gaps straight into $620 without a pullback, the risk-reward worsens quickly because the obvious stop sits far below the entry. A better setup would be either a $600 hold with volume or a pullback toward $590 that does not break the trend. Below the mid-$570s, the Friday "explosion" thesis should be shelved until the chart rebuilds.

Investors already in the stock have a different job. They do not need to trade every candle. After a 34% one-month move and a 25% one-week move, trimming a small piece into strength is rational if the position has become too large. Holding a core position is also rational if the one-year thesis is June self-serve adoption, ad-spend expansion outside gaming, and sustained EBITDA margins. Those are not one-day variables.

One-year advice: hold the thesis, not the hype

The one-year case for AppLovin is compelling because it has a clean business mechanism: better AI ad matching can raise advertiser returns, which can pull more spend into the platform, which can then show up as revenue and EBITDA without a matching increase in cost. That is the bull case in one sentence. It is also why the stock has become dangerous for anyone who looks only at the chart.

At $599.24, APP already discounts a lot of execution. The trailing P/E from TECHi's quote stack is roughly 51.5x, and the stock remains below but not far from its 52-week high of $745.61. The valuation does not need bad news to pull back. It can compress simply because investors decide the next dollar of growth deserves a smaller multiple.

For a one-year investor, the clean plan is this: hold or build only if the June self-serve launch shows real demand outside the initial pilot base, Q2 and Q3 margins stay near the guided range, and the company continues to show that e-commerce advertisers can scale without breaking return on ad spend. If those pieces hold, the $701.11 model price is defensible, with a $700 to $750 zone in reach over the next year. If growth decelerates or the ad market turns, the $635.58 base case and $566.79 stress case are better anchors than any upside target.

The risks that should keep this forecast honest

The easiest way to ruin an APP article is to treat the stock like a guaranteed AI winner. AppLovin still operates in a competitive digital advertising market, depends on advertiser budgets, relies on mobile platform rules and data access, and faces privacy, measurement, and model-performance risks that can change quickly. The company's 2025 10-K lays out risk factors around competition, privacy regulation, platform dependence, and advertiser demand. Those risks matter more after a stock has already run.

The near-term risk is simpler. If Friday opens with excitement and then loses $600, the buyers who chased Thursday's move will have little patience. If it loses $590, the market may treat the stock as overextended. If it loses the mid-$570s, the setup changes from "momentum continuation" to "failed breakout." None of that invalidates the one-year business thesis. It only says the stock price can get ahead of the thesis.

This article is market commentary and scenario analysis, not personalized financial advice. APP is a volatile equity, and one-day forecasts can fail quickly. Use position sizing and independent research before trading.

Bottom line

APP can break higher tomorrow, but the clean answer is conditional. The Friday model says $605.83, the breakout tape says $615 to $620 is possible if $600 holds, and the one-year research model says $701.11 if AppLovin's AI advertising engine keeps converting growth into extreme EBITDA margins. That is an attractive setup, not a free pass.

The stock's job on Friday is to prove the move has sponsorship above $600. The company's job over the next year is harder: prove that the June self-serve expansion can turn a great margin story into a broader advertising platform. If both happen, APP does not need hype to keep working. If either fails, the stock is expensive enough to punish late buyers.

FAQ

Frequently asked questions

What is TECHi's APP stock forecast for tomorrow?

TECHi's one-day APP model pointed to about $609 as of May 28, 2026. A stronger Friday tape could test $615 to $620 if APP holds $600 and clears the May 28 intraday high, but a break below the mid-$570s would invalidate the short-term breakout setup.

What is TECHi's one-year AppLovin stock forecast?

TECHi's one-year model pointed to about $714 as of May 28, 2026, with a stress case near $571 and a bull case near $717. The one-year thesis depends on self-serve advertiser adoption, sustained margins, and valuation discipline.

Why is AppLovin stock moving?

APP is moving because investors are repricing AppLovin's AI advertising platform, Q1 2026 profit margins, Q2 guidance, and the June self-serve expansion catalyst.

Is APP stock a buy after the rally?

APP may still work for investors who can tolerate volatility and size positions carefully, but chasing a vertical move above $600 without a pullback carries high risk. The setup is more attractive when the stock confirms support or gives a disciplined entry.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Umair Aslam is an ACCA-qualified finance executive based in Al Khobar, Saudi Arabia. His CV lists INSEAD Executive Education's Management Acceleration Leadership Program in 2025, so his TECHi profile treats INSEAD as completed executive education rather than current enrollment. His work sits at the intersection of corporate finance, operating discipline, financial reporting, and executive decision-making across growth markets. On TECHi, Umair focuses on finance, markets, fintech, AI adoption, and boardroom-level strategy: the practical questions executives, investors, and operators ask when numbers, policy, technology, and execution all meet. His profile is built around transparent credentials, public social links, and a clear professional beat so readers can evaluate his perspective before following his analysis.