AppLovin is a useful stress test for TECHi's AI stock model because it refuses to fit the easy categories. It is not a chipmaker, not a cloud landlord, and not a software company selling seats to CIOs. Its AI shows up in a messier place: ad auctions, bid optimization, app discovery, and the conversion math that decides whether a mobile impression is worth buying.

That is exactly why APP still ranks near the top of TECHi's stock model. The model is not rewarding the phrase "AI advertising" by itself. It is rewarding a business where the AI claim has started to appear in revenue growth, margin structure, and cash generation. The uncomfortable part is that the market has noticed the same thing.

- Model signalAPP ranks high because TECHi's stock model sees rare AI monetization: fast software-platform growth, strong margins, and heavy free-cash-flow conversion.

- Valuation brakeThe stock is not cheap. TECHi's quote page showed APP at $597.08 after the June 2 close, with a $205.96 billion market cap and only 8.5% consensus target upside.

- What matters nextThe ranking stays durable only if AppLovin keeps proving that its ad model can widen beyond mobile gaming while holding unusually high EBITDA and cash-flow margins.

Why TECHi Still Ranks APP So Highly

On TECHi's /markets/stocks/ hub, AppLovin is prominent in the AI applications and software-data cohort. The reason is not a single headline or a one-day price move. The one-year model favors quality trend, forward growth, earnings revision strength, and market sponsorship, then subtracts for valuation pressure. APP scores unusually well on the first three and gets penalized on the last one.

That mix matters. Plenty of AI stocks screen well on narrative and poorly on proof. APP is almost the reverse: the story can sound abstract, but the operating numbers are concrete. The model likes it because AppLovin's software platform has become a high-margin growth engine, not because the stock is trading at a bargain-bin multiple.

The Quality Signal Is Not Subtle

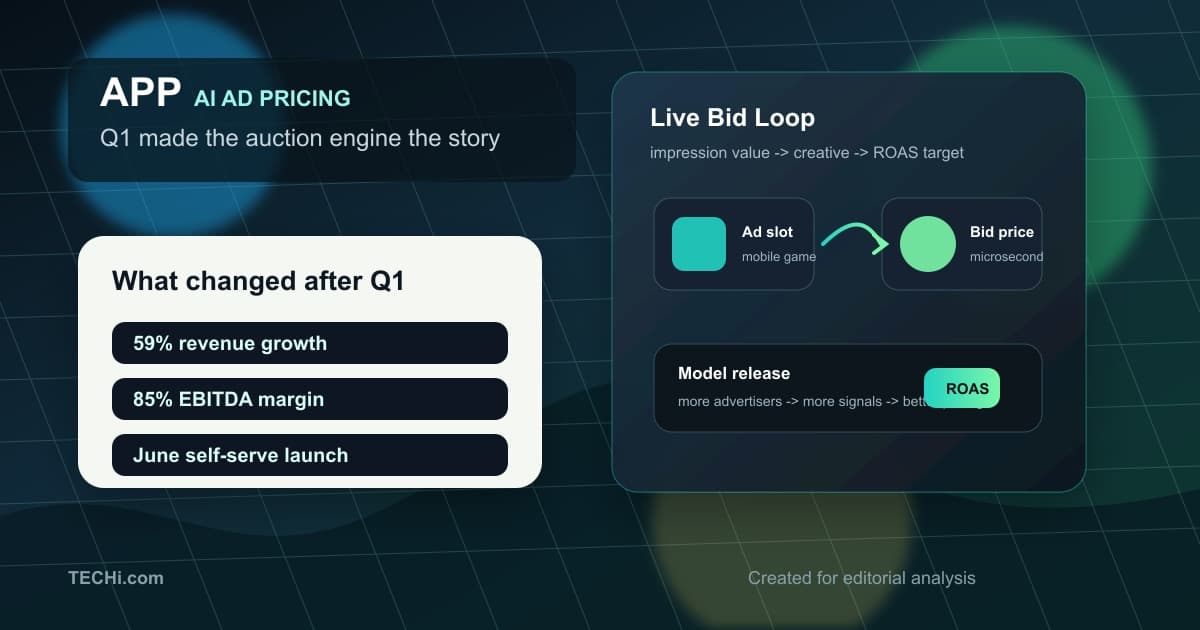

AppLovin reported Q1 2026 results and filed the same release with the SEC for the quarter ended March 31, 2026. The numbers would stand out in almost any software screen: total revenue of $1.48 billion, up 40% from a year earlier; advertising revenue of $1.16 billion, up 71%; net income of $576 million; adjusted EBITDA of $1.03 billion; and free cash flow of $920 million.

The margin line is the tell. A company can grow quickly by buying volume, discounting aggressively, or leaning on a hot market. AppLovin's Q1 adjusted EBITDA margin was 70%, and management guided Q2 adjusted EBITDA of $1.02 billion to $1.04 billion on revenue of $1.26 billion to $1.28 billion. That implies a business model where incremental revenue is falling through at a rate that most AI software companies would like to have.

That is the TECHi-native reason APP sits so high. The model is looking for AI companies where the product loop is already financial. In AppLovin's case, better ad matching should raise return on ad spend, which should attract more advertiser demand, which gives the model more auction data, which can improve targeting again. When that loop works, the income statement notices.

The Valuation Brake Is Real Too

This is where the quote page becomes more cautious than the stock hub. TECHi captured APP at $597.08 after the June 2, 2026 close, down 1.43% on the day, with a $205.96 billion market cap. The same APP quote page showed a consensus target of $647.85 across 34 analysts, or about 8.5% upside from that price.

That is not the setup of a forgotten compounder. The quote page's Decision Lens reads Neutral watch, with a 58/100 score, while the forward model is Positive but selective. That split is not a contradiction. It is the product doing what it should do: the stock hub highlights APP as one of the cleaner AI quality stories, while the quote page reminds readers that high quality and good entry price are different questions. That same selectivity shows up on TECHi's APP forecast page, where quality and growth leads are high but valuation pressure keeps the setup from reading like a simple green light.

The free-cash-flow yield sharpens the point. TECHi quote data showed trailing free cash flow of $2.33 billion and an FCF yield of 1.3%. That is the market saying investors are paying for persistence: sustained software-platform growth, durable pricing power, and a margin profile that does not fade as AppLovin pushes into broader advertiser categories.

What Could Break the Ranking

The cleanest risk is that AppLovin's AI advantage proves narrower than the current growth rate suggests. If advertisers see weaker returns, if non-gaming expansion comes in slower, or if larger ad platforms squeeze the same performance gap, the quality score can fall quickly. This is still an advertising business, and advertising businesses can look strongest near the top of a cycle.

Platform and policy risk also deserve a line. AppLovin depends on mobile ecosystems, signal quality, and advertiser confidence. Changes in privacy rules, app-store economics, or auction transparency can move the economics even when the model itself keeps improving. A high stock-model rank should not make those risks disappear; it should make them more specific.

What Would Make the Ranking More Durable

For APP to keep its place near the top, the next few quarters need to show that Q1 was not just a great print against an easy comparison. Watch advertising revenue growth, adjusted EBITDA margin, free cash flow conversion, and evidence that AppLovin's software platform is scaling outside the categories that built the company.

The most constructive version of the story is not simply that AppLovin has AI. It is that AppLovin's AI system can keep raising advertiser outcomes without requiring an equal rise in operating cost. If that remains true, the premium multiple has a defense. If growth slows while the valuation stays stretched, the stock can still be a strong business and a difficult trade.

How TECHi Reads APP Now

APP deserves its high TECHi model rank because it has one of the cleaner financial translations of AI in public markets: rapid software-platform growth, unusually high margins, and cash generation that already looks mature. It also deserves the quote page's caution because the market is pricing in a long runway.

That is the right way to read the ranking. APP is not near the top because it is an easy buy. It is near the top because the business quality is hard to ignore. From here, the burden shifts to execution: every quarter has to defend the premium the model is flagging.

FAQ

Frequently asked questions

Why does AppLovin rank near the top of TECHi's AI stock model?

APP ranks high because TECHi's model gives strong credit to quality, growth, revision strength, and cash-flow conversion. AppLovin's Q1 2026 advertising revenue rose 71% year over year, and the company produced $920 million of free cash flow.

Is the TECHi AI stock model a buy recommendation?

No. The model is a research screen, not personalized investment advice. A high rank means the stock scores well on TECHi factors; investors still need to assess valuation, risk, position sizing, and timing.

What AppLovin metric matters most now?

Advertising revenue growth and adjusted EBITDA conversion matter most. They show whether AppLovin can keep turning AI-driven ad matching into revenue and cash flow rather than just headline growth.

Why is valuation a risk for APP stock?

TECHi quote data after the June 2, 2026 close showed APP at $597.08, a $205.96 billion market cap, and only 8.5% consensus target upside. At that level, the market is already pricing in durable growth and high margins.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Umair Aslam is an ACCA-qualified finance executive based in Al Khobar, Saudi Arabia. His CV lists INSEAD Executive Education's Management Acceleration Leadership Program in 2025, so his TECHi profile treats INSEAD as completed executive education rather than current enrollment. His work sits at the intersection of corporate finance, operating discipline, financial reporting, and executive decision-making across growth markets. On TECHi, Umair focuses on finance, markets, fintech, AI adoption, and boardroom-level strategy: the practical questions executives, investors, and operators ask when numbers, policy, technology, and execution all meet. His profile is built around transparent credentials, public social links, and a clear professional beat so readers can evaluate his perspective before following his analysis.