- The short answerNVIDIA is the #1-ranked AI stock — but the smarter play is owning the four layers of AI (chips, infrastructure, cloud and software), not a single name.

- How we rankWe grade each stock on AI revenue durability, control of scarce resources (moat) and valuation risk — not hype or last week's price.

- The core sixNVIDIA, Microsoft, Broadcom, TSMC, Alphabet and Amazon are the lower-risk backbone of an AI portfolio.

- Higher risk, higher rewardAMD, Meta, Palantir, Oracle, Arista and Marvell add upside — and sharper drawdowns.

- The one big riskThe whole group runs on hyperscaler AI capex; if that spending slows, the entire supply chain re-rates fast.

- Before you buyA great company can be a poor entry at the wrong price — check the live valuation on each stock's quote page and size for volatility.

The best AI stocks aren't a single lottery ticket — they're a stack of businesses that each control a different scarce resource in the artificial-intelligence buildout. At the base are the chipmakers. Above them sit the infrastructure and foundry companies that physically make and connect the hardware. Above that are the hyperscaler platforms that rent AI capacity to the world, and at the top are the software companies turning models into revenue.

NVIDIA leads this ranking, as it has since the AI trade began. But the more durable lesson is structural: the strongest way to own AI is to own the layers — compute, infrastructure, cloud and software — rather than betting everything on one name. This guide ranks the 12 best AI stocks for 2026, explains how we score them, and shows how to assemble them into a portfolio that can survive a drawdown.

What makes a stock an "AI stock"?

An AI stock is a company whose earnings are materially tied to the development, deployment or infrastructure of artificial intelligence. That is a deliberately strict definition. A company that merely mentions AI on an earnings call is not an AI stock; a company whose chips, cloud capacity, networking or software is being bought specifically to build and run AI is.

By that test, the best AI stocks fall into four groups:

- AI chips — the processors that train and run models (NVIDIA, AMD, Broadcom, Marvell).

- Infrastructure and foundry — the companies that manufacture and connect the hardware (TSMC, Arista Networks).

- Hyperscaler platforms — the clouds that rent AI compute and build AI into software (Microsoft, Alphabet, Amazon, Meta).

- AI software — the application and data layer that turns models into product (Palantir, Oracle).

Owning across these layers is the single most important idea here, because no one yet knows which company captures the largest share of AI's eventual profit pool.

How we rank the best AI stocks

Three filters decide the order.

1. AI revenue durability. A company earns more credit when AI demand already flows through its income statement — through silicon orders, cloud usage, backlog or software renewals — and less credit when AI is mostly a narrative attached to a high multiple. That is why NVIDIA, Microsoft, Broadcom and TSMC sit above flashier names.

2. Control of scarce resources. AI is capital-intensive, and the companies that control the bottlenecks — accelerators, advanced-node manufacturing, networking, cloud distribution, proprietary data and enterprise budgets — deserve a higher ranking than companies simply riding the theme.

3. Valuation risk. A high forward multiple is not automatically wrong if the business compounds through it, but it leaves little room for a slower quarter or a missed contract cycle. That is why a name like Palantir is treated as an important AI stock but not a low-risk core holding.

The ranking reflects business quality and risk, not last week's share price. Prices move daily; moats move slowly.

The 12 best AI stocks for 2026, ranked

1. NVIDIA (NVDA) — the AI compute benchmark

NVIDIA is the anchor of the AI trade because it owns the most direct route from AI spending to revenue. GPUs are only part of the story; the deeper moat is the full-stack system — the CUDA software platform, networking, reference designs, enterprise software and a customer base that buys in clusters rather than single chips. The risks are its own success: expectations are enormous, and hyperscalers are slowly building custom silicon to reduce their dependence. See the NVIDIA quote page, and the company's data-center platform for the full stack.

2. Microsoft (MSFT) — AI distribution at enterprise scale

Microsoft ranks second because it is not waiting for an AI business model to appear. Azure sells AI capacity, GitHub sells developer productivity, Microsoft 365 pushes Copilot into a vast enterprise base, and its OpenAI partnership reinforces the whole platform. The open question is whether AI capex keeps converting into revenue fast enough to justify the spending curve. Track it on the Microsoft quote page.

3. Broadcom (AVGO) — custom silicon and AI networking

Broadcom is the cleanest pick-and-shovel name outside NVIDIA. Its custom AI accelerators and networking silicon matter more as hyperscalers diversify away from a single vendor and tune chips for their own workloads, and the VMware software base gives it a steadier earnings profile than a pure semiconductor cyclical. Details on the Broadcom quote page.

4. TSMC (TSM) — the foundry toll road

TSMC captures AI demand even when the winning chip designer changes. NVIDIA, AMD, Apple, Broadcom and the hyperscalers' in-house silicon all need its advanced-node capacity and packaging. The discount on the stock is geopolitical, not technological — the Taiwan question, not the demand question. Its scale is laid out in TSMC's investor materials and on its quote page.

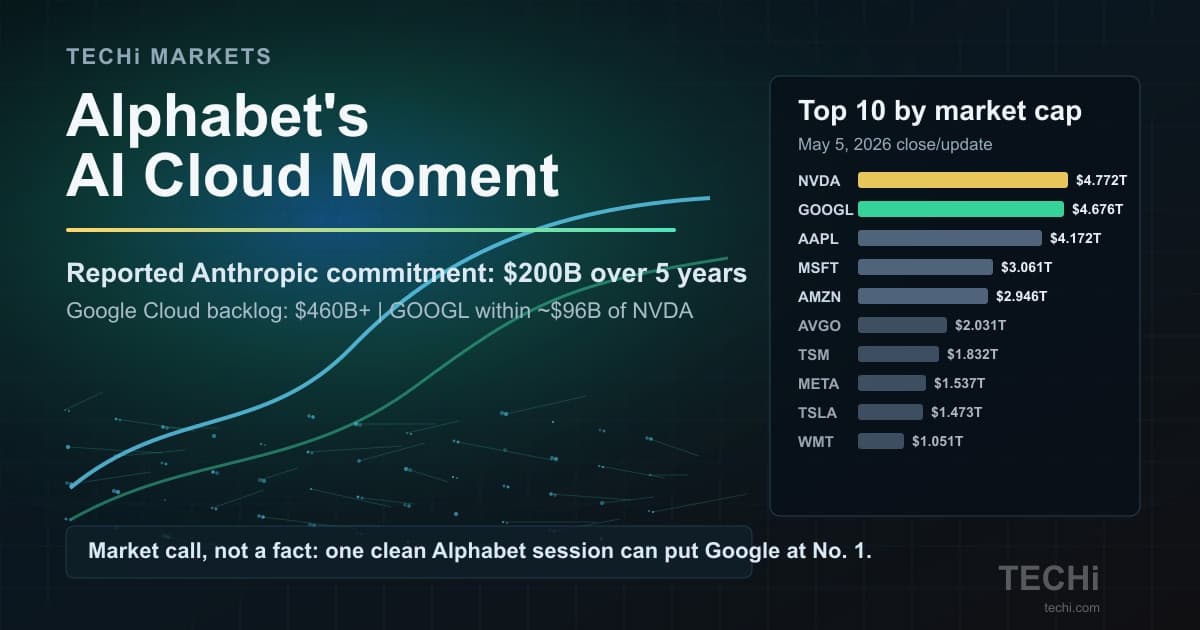

5. Alphabet (GOOGL) — the integrated AI platform

Alphabet pairs the Gemini model family with its own TPUs, Google Cloud and the cash machine of search. That vertical integration — model, chip and cloud under one roof — is rare. The risk is also unique: AI-driven shifts in how people search could pressure the very business that funds everything else. See the Alphabet quote page.

6. Amazon (AMZN) — AWS plus its own silicon

Amazon has AWS (the largest cloud), its Trainium and Inferentia chips, a deep retail-data advantage and a fast-growing, high-margin advertising business that AI improvements monetize quickly. The weight to watch is capex against margins. More on the Amazon quote page.

7. Meta (META) — AI monetized through advertising

Meta runs some of the world's largest recommendation systems, releases open models that pull developers toward its stack, and owns an ad engine that converts AI improvements into revenue almost immediately. The offset is its capital intensity — both AI infrastructure and the Reality Labs burn. See the Meta quote page.

8. AMD (AMD) — the credible compute challenger

AMD is the most direct challenger to NVIDIA in AI accelerators, and its reward depends on proving that hyperscalers want a genuine second source at scale. It carries more execution risk than the names above it, but more upside if its Instinct roadmap keeps landing. The accelerator line is detailed at AMD's investor site and on its quote page.

9. Palantir (PLTR) — the cleanest AI-software story

Palantir is the purest AI-software narrative on this list, with real commercial momentum as enterprises move from pilots to deployments. It is also the most valuation-sensitive name here — the business can compound and the stock can still fall if growth merely slows. A high-conviction, high-volatility holding. See the Palantir quote page.

10. Oracle (ORCL) — booked AI cloud demand

Oracle has turned itself into an AI-capacity story, with large cloud-infrastructure bookings and fast OCI growth. The questions are execution and the balance sheet as it funds that buildout. More on the Oracle quote page.

11. Arista Networks (ANET) — the AI cluster's nervous system

Arista supplies the high-speed networking that ties AI clusters together. As training and inference clusters scale, the networking layer compounds — though Arista's fortunes are tied to a concentrated set of hyperscaler customers. See the Arista quote page.

12. Marvell (MRVL) — custom silicon and interconnects

Marvell builds custom AI silicon and the optical-interconnect components that move data inside and between data centers. It can compound strongly if cluster demand stays high, but it is volatile and dependent on design wins. Details on the Marvell quote page.

How to build an AI stock portfolio

There is no single right basket — there are three sensible templates, and the right one depends on the kind of exposure you want.

- Conservative (AI as upside). Lean on the durable platforms and infrastructure: NVIDIA, Microsoft, Broadcom, TSMC, Alphabet and Amazon. These are profitable businesses where AI adds to an already-strong base.

- Aggressive (more beta). Add AMD, Meta and Palantir, accepting sharper drawdowns in exchange for more torque if the buildout accelerates.

- Pure infrastructure. Concentrate on the physical layer — NVIDIA, Broadcom, TSMC, Arista and Marvell — to bet on AI's supply chain rather than its applications.

Whichever you choose, size each position for a real drawdown, treat the basket as a multi-year holding rather than a trade, and rebalance on fundamentals, not headlines. You can screen and compare every name on TECHi's stock screener.

How to buy AI stocks

For most investors the mechanics are simple: open a brokerage account, decide how much of your portfolio belongs in a single volatile theme, and either buy individual leaders or take diversified exposure through an AI or semiconductor ETF. A common structure is a core of megacap leaders plus a small sleeve of higher-beta names. Whatever you buy, check the current price and forward valuation on the stock's quote page first — a great company bought at the wrong price is still a poor investment.

What could break the AI trade?

Four risks matter most.

The first is capex fatigue. The entire group is underwritten by hyperscaler spending on AI infrastructure; if even one major buyer guides that spending down, investors will reprice the whole supply chain within hours.

The second is monetization lag. AI tools are improving fast, but revenue has to grow faster than the depreciation and power costs of the hardware behind them. If it does not, margins compress.

The third is custom silicon. Hyperscalers designing their own chips does not end NVIDIA's role, but it can cap the most aggressive assumptions about its future market share.

The fourth, and most common, is simply price. A great company can be a poor stock if the entry valuation already assumes flawless execution. That is the discipline this ranking is built around: the best AI stocks are not just the most exciting companies — they are the best balance of exposure, control, monetization and valuation.

The bottom line

NVIDIA is still the top-ranked name, but the real takeaway is structure. The strongest AI portfolio is not only chips, only cloud or only software — it spans compute, foundry capacity, networking, cloud distribution, enterprise monetization and a clear discipline around price. Own the layers, respect the valuations, and treat the whole position as a long-term stake in the most important technology shift of the decade.

FAQ

Frequently asked questions

What is the best AI stock to buy right now?

NVIDIA is TECHi's #1-ranked AI stock because it has the most direct line from AI spending to revenue — GPUs plus the CUDA software, networking and systems around them. But “best” depends on your risk tolerance; a balanced basket across chips, cloud and software lowers single-stock risk.

What are the best AI stocks for beginners?

Beginners usually start with the lower-risk backbone: NVIDIA, Microsoft, Alphabet and Amazon. These are profitable megacaps where AI is upside on top of an already-strong business, rather than pre-profit bets that can swing 30-50%.

What are the four types of AI stocks?

AI chipmakers (NVIDIA, AMD, Broadcom, Marvell); infrastructure and foundry (TSMC, Arista); hyperscaler platforms (Microsoft, Alphabet, Amazon, Meta); and AI software (Palantir, Oracle). Owning across the four layers reduces the risk of betting on a single winner.

Is NVIDIA still the best AI stock?

By TECHi's framework, yes — NVIDIA remains #1 because it controls the dominant AI compute stack and converts data-center spending into revenue faster than any peer. The main risks are very high expectations and the gradual rise of custom hyperscaler silicon.

Are AI stocks a bubble?

Parts of the market price in flawless execution, and a pullback is possible if hyperscaler capex slows or AI revenue lags the spending. But the leaders have real, growing AI revenue, so it is better understood as an expensive trade than a pure mania — manage it with valuation discipline and diversification.

What are the best AI stocks under $100?

Several leaders trade at accessible share prices, but share price alone doesn't make a stock cheap — valuation is about price relative to earnings and growth. Use each stock's quote page to check the forward valuation rather than the headline share price.

How do I invest in AI stocks?

You can buy individual leaders through any brokerage, or get diversified exposure through an AI or semiconductor ETF. A common approach is a core of megacap leaders plus a small sleeve of higher-beta names, each sized for volatility.

Which AI stock has the most upside?

The higher-beta names — AMD, Palantir, Marvell and Arista — carry the most upside if the AI buildout keeps accelerating, but also the sharpest drawdowns if it slows. They suit investors who can tolerate volatility rather than those who want stability.

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, tax, or legal advice. Market data, tax rules, and prices can change after the article date. TECHi and its authors may hold positions in securities or digital assets mentioned. Always conduct your own research and consult a licensed financial, tax, or legal professional before making decisions.

About the Author

Fatimah Misbah Hussain is a seasoned financial journalist at TECHi, specializing in stock market analysis, commodities, and tech sector finance. With a strong background in monitoring public markets and tech companies, she breaks down complex stock movements and commodity price trends into actionable insights.